Functional Analysis in TP Reports

The introduction of UAE Corporate Tax (Federal Decree-Law No. 47 of 2022) has placed significant emphasis on Transfer Pricing (TP) compliance. For businesses engaged in related-party transactions, one of the most critical elements of TP documentation is the Functional Analysis (FAR).

A well-prepared FAR analysis not only ensures compliance with the Arm’s Length Principle but also provides clarity on how value is created and shared within a multinational group.

________________________________________

1. What is a Functional Analysis (FAR)?

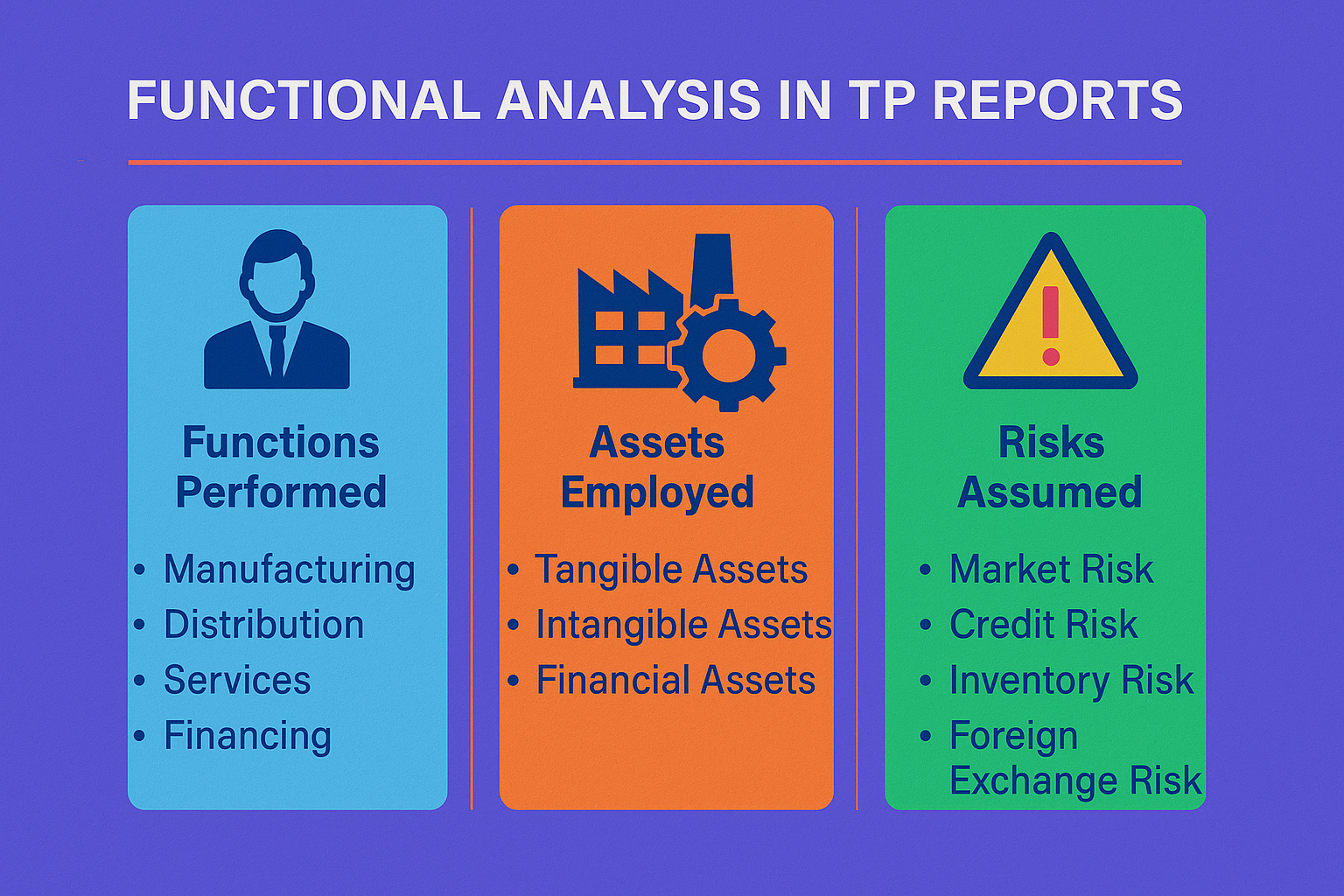

Functional Analysis is the process of identifying and evaluating:

• Functions performed – what each entity does,

• Assets employed – resources (tangible and intangible) used in transactions, and

• Risks assumed – commercial, operational, and financial risks borne by each party.

This three-dimensional approach ensures that profits are aligned with economic substance, not just legal ownership.

________________________________________

2. Why is FAR Essential in TP Reports?

• Demonstrates that intra-group transactions comply with the Arm’s Length Principle.

• Determines the tested party for benchmarking analysis.

• Guides the selection of the most appropriate TP method.

• Provides strong evidence in case of FTA audit or inspection.

• Protects businesses from penalties, adjustments, and double taxation.

________________________________________

3. The FAR Framework Explained

A) Functions Performed

Functions vary depending on the business model. Common examples include:

• Manufacturing: procurement, production, R&D, quality control.

• Distribution: warehousing, marketing, logistics, after-sales service.

• Services: IT, HR, management, consultancy.

• Financing: cash pooling, loans, treasury functions.

👉 Entities performing high-value functions (e.g., R&D, marketing intangibles) are expected to earn greater returns.

________________________________________

B) Assets Employed

Assets directly influence the value created in a transaction.

• Tangible assets: property, plant, equipment, warehouses.

• Intangible assets: patents, brands, know-how, customer lists.

• Financial assets: working capital, intercompany loans, guarantees.

👉 Ownership of unique intangibles (like trademarks or technology) typically commands premium profits.

________________________________________

C) Risks Assumed

Risk allocation is central to determining profitability. Examples include:

• Market Risk – demand fluctuations, competition.

• Credit Risk – customer defaults.

• Inventory Risk – obsolescence, storage losses.

• Operational Risk – production delays, supply chain disruptions.

• Foreign Exchange Risk – volatility in cross-border transactions.

👉 Higher risks should correspond to higher expected returns.

________________________________________

4. Role of FAR in TP Method Selection

The findings of FAR directly impact:

• Which TP method applies (CUP, Resale Price, Cost Plus, TNMM, Profit Split).

• Whether the entity is a limited-risk service provider/distributor or a full-risk entrepreneur.

• What profit margin or pricing policy is justified under benchmarking studies.

________________________________________

5. FAR in UAE Context

• Free Zone Companies: FAR is crucial for proving substance and retaining Qualifying Income status.

• Gold & Jewellery Sector: FAR distinguishes between a trader assuming inventory risk and a limited-risk reseller.

• Family Businesses: FAR clarifies roles and ensures tax-efficient allocation across group entities.

• Cross-Border Transactions: FAR supports double tax treaty positions and dispute prevention.

________________________________________

6. Example of FAR in Practice

Scenario: A UAE subsidiary imports branded apparel from its parent and sells locally.

• Functions: Sales, limited marketing, distribution.

• Assets: Warehousing facilities, no unique IP.

• Risks: Bears inventory and credit risk; brand risk stays with parent.

Conclusion: The UAE entity is a limited-risk distributor. Under TNMM, its return should be benchmarked against independent distributors, typically earning a modest margin (e.g., 3–6%).

________________________________________

7. Best Practices for FAR Analysis

• Conduct management interviews and process walkthroughs.

• Validate functions/risks using contracts and actual conduct.

• Ensure consistency across FAR, benchmarking, and financials.

• Refresh FAR annually to reflect business changes.

• Integrate FAR into Local File and Master File for UAE compliance.

________________________________________

✅ How Sheikh Anwar Accounting & Auditing LLC Can Help

At Sheikh Anwar Accounting & Auditing LLC, we prepare comprehensive Transfer Pricing documentation, with FAR analysis tailored to UAE business models and FTA expectations.

Our Expertise Includes:

• FAR interviews & documentation.

• Preparation of Local File & Master File.

• Benchmarking studies and arm’s length range analysis.

• Advisory on TP method and tested party selection.

• Support during FTA Transfer Pricing audits.

📌 Contact Us Today

🌐 www.sa-auditors.com

✉️ info@sa-auditors.com | 📱 +971-XX-XXXXXXX