Free Zone Leasing Activities and Tax

Free Zones in the UAE are well-known for offering attractive business incentives, including 100% foreign ownership, ease of setup, and, under the UAE Corporate Tax Law, a 0% tax rate for Qualifying Free Zone Persons (QFZPs) on certain income.

However, when it comes to leasing activities—such as renting out commercial property or equipment—the tax treatment becomes complex and must be carefully analysed under the law.

Here, we explain how leasing income is treated under the UAE Corporate Tax Law, how it affects QFZP status, and what Free Zone businesses engaged in leasing should do to remain compliant.

________________________________________

📘 Legal Framework

Key references:

• Federal Decree-Law No. 47 of 2022 – UAE Corporate Tax

• Cabinet Decision No. 55 of 2023 – QFZP conditions

• Ministerial Decision No. 139 of 2023 – Qualifying & Excluded income

• Ministerial Decision No. 265 of 2023 – Transfer Pricing

• FTA Public Clarifications on QFZP eligibility and income classification

________________________________________

🏢 What Are Leasing Activities?

Leasing activities in Free Zones may include:

• Renting out commercial office space or warehouses

• Leasing industrial land plots or retail units

• Subleasing units to other Free Zone entities

• Leasing machinery, vehicles, or equipment

• Real estate developers leasing built properties to tenants

These activities are not automatically considered qualifying under the Corporate Tax Law.

________________________________________

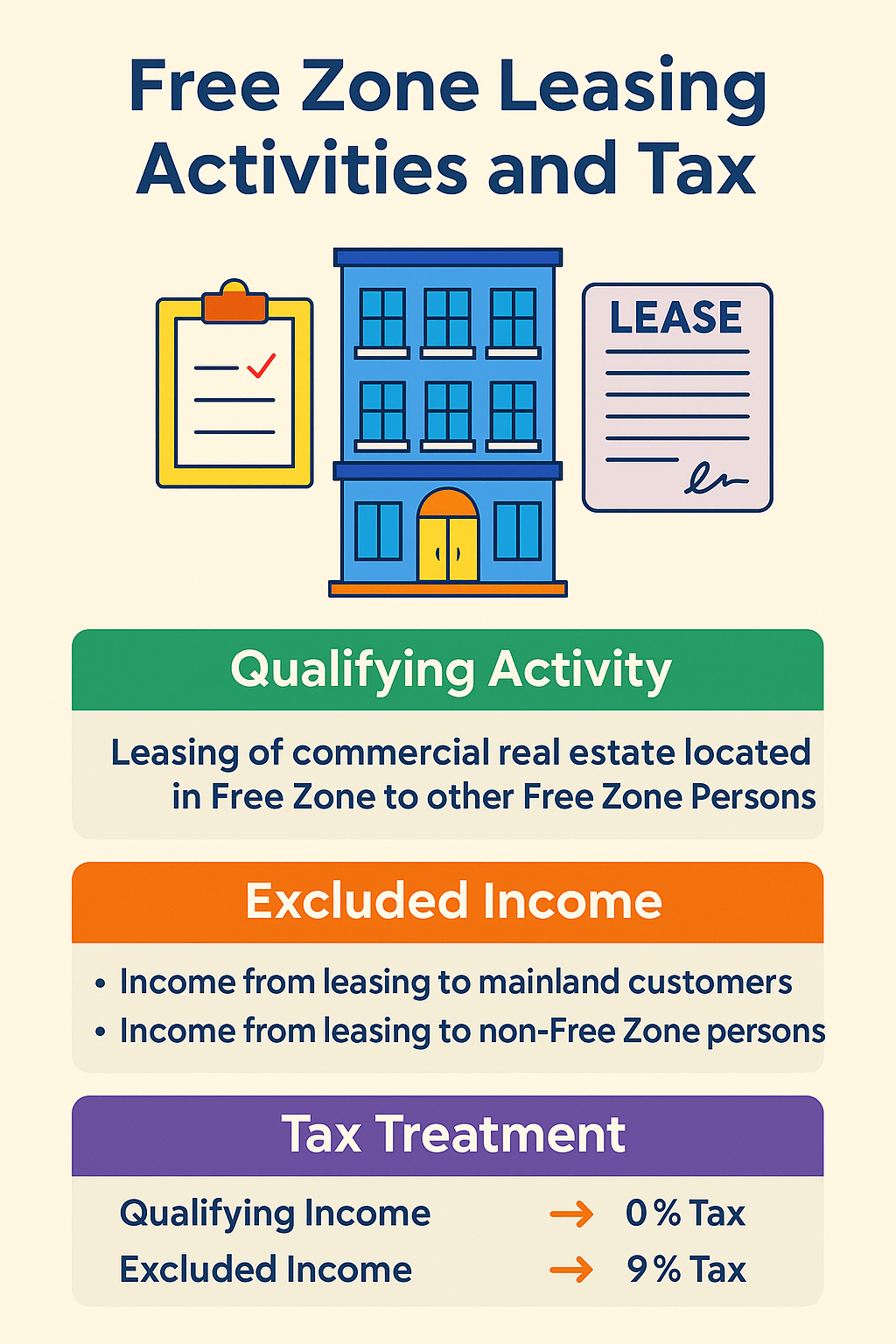

❗ Is Leasing a Qualifying Activity?

According to Ministerial Decision No. 139 of 2023, the following applies:

✅ Qualifying Activity:

• Leasing of commercial real estate located in a Free Zone to other Free Zone Persons is considered a qualifying activity.

❌ Excluded Income:

• Income from leasing immovable property to UAE mainland persons (even if the property is in a Free Zone) is excluded income and not eligible for the 0% rate.

• Income from leasing Free Zone property to non-Free Zone entities (including individuals and mainland companies) is also excluded.

________________________________________

📌 Tax Treatment of Leasing Activities

Scenario Qualifying for 0% Tax? Notes

Leasing office space to Free Zone company ✅ Yes Qualifying income

Leasing warehouse to mainland UAE company ❌ No Excluded income (taxed at 9%)

Leasing to individual (not business) ❌ No Not qualifying income

Subleasing within Free Zone (to FZP) ✅ Yes If conditions are met

Equipment leasing to Free Zone companies ✅/❌ Case-by-case, depends on nature and counterparty

Commercial real estate leased to foreign company ✅ Yes Qualifying income if property in Free Zone and lessee is non-resident

________________________________________

🧾 Impact on QFZP Status

If a Free Zone entity derives excluded income, such as from mainland leasing:

• It does not automatically lose QFZP status, provided it:

o Continues to meet all other QFZP conditions

o Properly segregates qualifying and non-qualifying income

o Pays 9% tax on non-qualifying income

However:

• If income from excluded activities becomes dominant, the FTA may scrutinize the QFZP status.

• Improper recordkeeping or misclassification can lead to disqualification.

________________________________________

📑 Key Compliance Requirements for Leasing Activities

Requirement Description

Income Segregation Maintain separate ledgers for qualifying and excluded income

Contracts Clearly identify lessee type (Free Zone, mainland, individual)

Substance Have operations (staff, systems) in the Free Zone

Transfer Pricing Apply arm’s length pricing if leasing to related parties

Annual Declaration Confirm continued QFZP eligibility with accurate disclosures

Audited Financials Mandatory if revenue > AED 50 million

________________________________________

⚠️ Risk Areas to Watch

• Leasing to mainland persons without declaring income as excluded

• Using dual licensing to lease outside Free Zone under QFZP entity

• Booking entire leasing revenue as qualifying

• Failing to provide supporting documentation for tenant classification

• Violating GAAR (anti-abuse rules) through artificial leasing structures

________________________________________

✅ Best Practices

• Use clear leasing agreements that define tenant status

• Implement automated income tagging in your ERP or accounting system

• Conduct annual QFZP review with your tax advisor

• Train finance teams on income classification rules

• Document lease allocation logic for multi-tenant properties

• Submit timely CT return and declarations with accurate segregation

________________________________________

🧑💼 How We Can Help

At Sheikh Anwar Accounting and Auditing LLC, we support Free Zone leasing entities with:

• ✅ Income classification review for QFZP eligibility

• ✅ Corporate Tax filing with proper disclosures

• ✅ Segregated accounting setup

• ✅ Transfer Pricing documentation

• ✅ FTA audit preparation for leasing portfolios

📧 Email: info@sa-auditors.com