Free Zone Corporate Tax Misconceptions

Introduction

Since the introduction of UAE Corporate Tax through Federal Decree-Law No. 47 of 2022, many Free Zone companies have operated under assumptions that could lead to non-compliance, penalties, or loss of benefits.

It clears up the most common misconceptions related to Free Zone Corporate Tax and provides factual clarifications to help businesses stay compliant.

________________________________________

🔍 Background: Free Zones and the 0% Corporate Tax

Free Zones were designed to attract foreign investment with business-friendly regulations. Under the UAE Corporate Tax regime, Qualifying Free Zone Persons (QFZPs) can benefit from 0% corporate tax on qualifying income, provided they meet strict conditions outlined in:

• Article 18 of the Corporate Tax Law

• Cabinet Decision No. 55 of 2023

• Ministerial Decision No. 139 of 2023

• FTA Public Clarifications

But misunderstanding these provisions can put your tax status at risk.

________________________________________

🚫 Common Misconceptions About Free Zone Corporate Tax

________________________________________

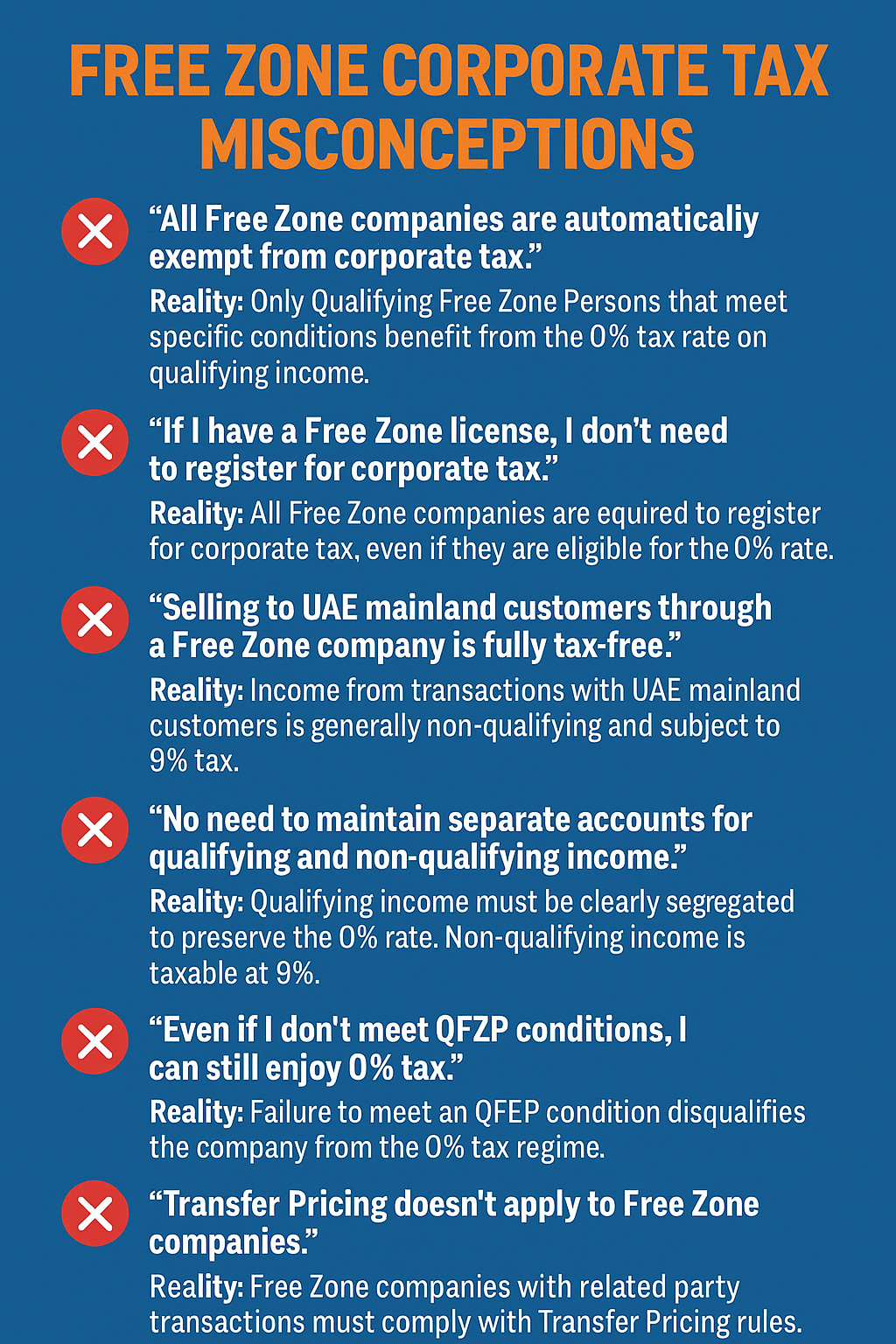

❌ 1. “All Free Zone companies are automatically exempt from corporate tax.”

✅ Reality:

Only companies that meet all QFZP conditions get the 0% rate on qualifying income. These include:

• Being a Free Zone Person

• Maintaining adequate economic substance

• Not electing to be taxed at 9%

• Deriving qualifying income only

• Complying with transfer pricing and documentation requirements

Non-qualifying income is taxed at 9%, even for Free Zone entities.

________________________________________

❌ 2. “If I have a Free Zone license, I don’t need to register for corporate tax.”

✅ Reality:

All UAE businesses, including Free Zone companies, must register for Corporate Tax — even if they expect to pay 0% tax.

FTA has made registration mandatory for all juridical persons, with specific deadlines based on license issuance date.

Failure to register can lead to a AED 10,000 penalty.

________________________________________

❌ 3. “Selling to UAE mainland customers through a Free Zone company is fully tax-free.”

✅ Reality:

Income from transactions with mainland UAE customers is considered non-qualifying unless:

• It relates to passive income (e.g., interest, royalties), or

• The Free Zone company is a designated zone trading in goods with customs control

Otherwise, income from mainland sales is subject to 9% Corporate Tax.

________________________________________

❌ 4. “No need to maintain separate accounts for qualifying and non-qualifying income.”

✅ Reality:

QFZPs must segregate qualifying vs. non-qualifying income in their accounting systems and financials. Failure to do so may result in:

• Loss of QFZP status

• 9% tax on entire income

• Penalties and audit risks

An accounting system that enables clear income classification is essential.

________________________________________

❌ 5. “Even if I don’t meet QFZP conditions, I can still enjoy 0% tax.”

✅ Reality:

FTA will revoke QFZP status if you fail to meet any one of the conditions, and the company will be subject to 9% tax on all taxable income from that tax period onward.

Common reasons for disqualification:

• Inadequate economic substance

• Engaging in excluded activities

• Missing annual QFZP declaration

• Improper related-party pricing

________________________________________

❌ 6. “Transfer Pricing doesn’t apply to Free Zone companies.”

✅ Reality:

Transfer Pricing (TP) rules apply to all entities, including Free Zone companies.

If you have related party or connected person transactions, you must:

• Apply the arm’s length principle

• Submit a Disclosure Form with your return

• Prepare a Master File and Local File if thresholds are met

FTA is empowered to recharacterize income if TP rules are violated.

________________________________________

❌ 7. “Free Zone companies don’t need audited financials.”

✅ Reality:

Audited financial statements are mandatory for Free Zone entities claiming QFZP status if their revenue exceeds AED 50 million in a tax year.

These statements must be retained and submitted within 9 months after the tax period ends.

________________________________________

📌 Final Thoughts

Free Zone companies have the opportunity to enjoy corporate tax incentives, but only if they:

• Understand and meet all QFZP conditions

• Avoid structuring arrangements that violate anti-abuse rules

• Maintain full documentation and transparency

________________________________________

✅ How We Can Help

At Sheikh Anwar Accounting and Auditing LLC, we assist Free Zone companies with:

• QFZP status assessments and reviews

• Corporate tax registration and filings

• Transfer pricing documentation

• Segregated accounting systems setup

• Audit-ready financials and advisory

📧 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com