Exemption for Free Zone Qualifying Income

The introduction of the UAE Corporate Tax regime through Federal Decree-Law No. 47 of 2022 has brought important considerations for businesses operating in Free Zones. While all juridical persons in the UAE are subject to corporate tax, the law offers a special relief mechanism for Qualifying Free Zone Persons (QFZPs)—specifically on Qualifying Income.

Sheikh Anwar Accounting & Auditing LLC explains the conditions, categories of income, and the legal framework for 0% corporate tax exemption on qualifying income earned by Free Zone entities.

________________________________________

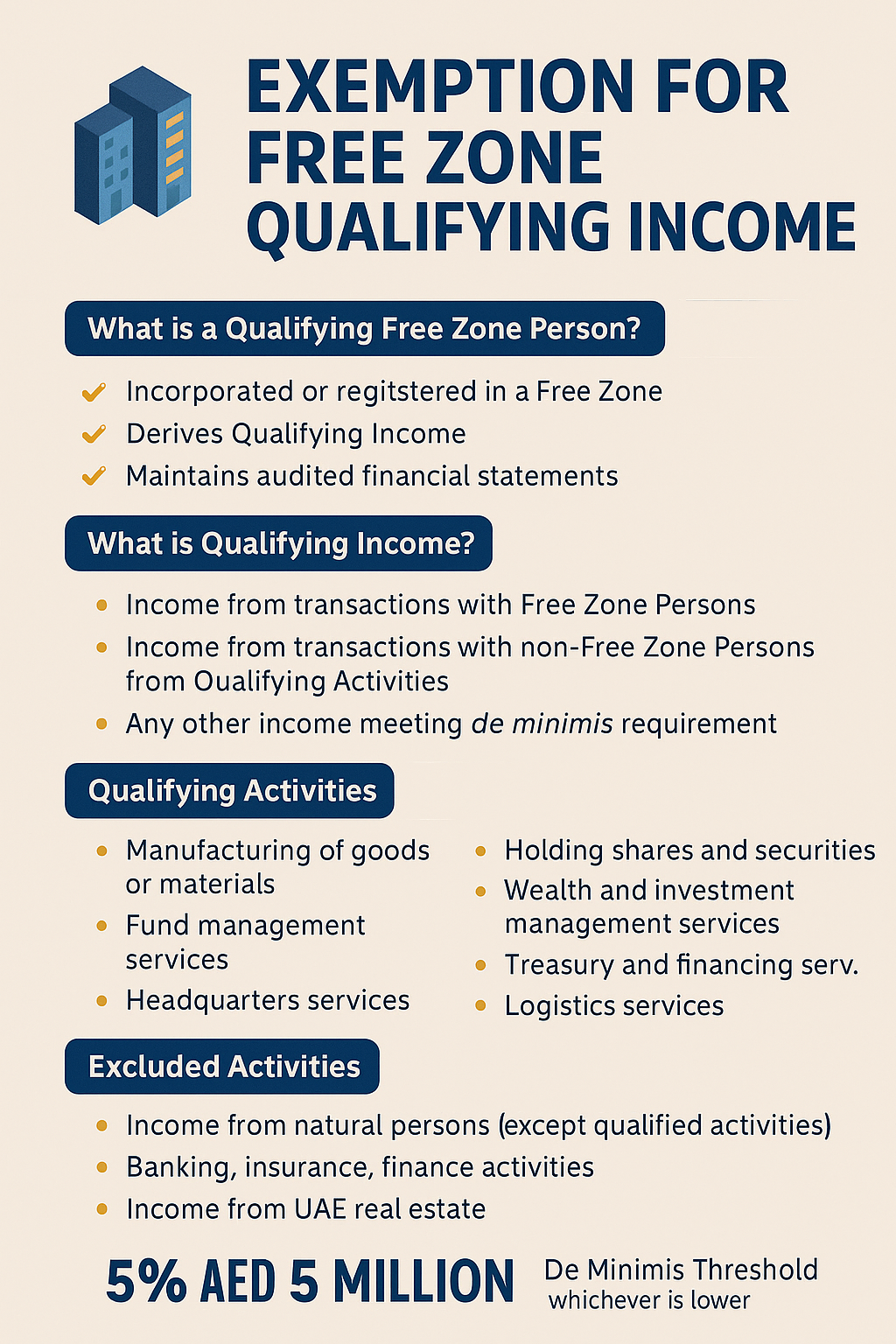

🔍 What is a Qualifying Free Zone Person?

A Qualifying Free Zone Person (QFZP) is a Free Zone business that:

1. Is incorporated or registered in a Free Zone, including Financial Free Zones.

2. Maintains adequate substance in the UAE.

3. Derives Qualifying Income, as defined by the Cabinet and Ministerial Decisions.

4. Complies with transfer pricing rules and documentation requirements.

5. Has not elected to be subject to regular corporate tax.

6. Prepares audited financial statements.

📜 Legal Reference:

• Article 18 of UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022)

• Cabinet Decision No. 55 of 2023

• Ministerial Decision No. 139 of 2023

________________________________________

✅ What is Qualifying Income?

Qualifying Income includes income that is eligible for the 0% corporate tax rate. According to Ministerial Decision No. 139 of 2023, it includes:

1. Income from transactions with other Free Zone Persons, excluding income from Excluded Activities.

2. Income from transactions with non-Free Zone persons, but only in respect of Qualifying Activities.

3. Any other income that meets the de minimis threshold.

________________________________________

🛠️ What are Qualifying Activities?

As per Ministerial Decision No. 139 of 2023, Qualifying Activities include:

• Manufacturing of goods or materials

• Holding of shares and securities

• Ownership, management, and operation of ships

• Reinsurance and fund management services

• Wealth and investment management services

• Headquarter services

• Treasury and financing services

• Financing and leasing of aircraft

• Logistics services

• Distribution of goods in or from a designated Free Zone (meeting customs conditions)

📌 Note: Qualifying income must be derived from one of these core activities and not constitute Excluded Activities.

________________________________________

🚫 What are Excluded Activities?

The following are not eligible for 0% tax, and income derived from these is fully taxable at 9%:

• Income from transactions with natural persons (except for Qualifying Activities like warehousing or logistics)

• Regulated banking, insurance, finance activities

• Income from real estate located in the UAE (except Free Zone commercial property to Free Zone Persons)

• Ownership or exploitation of intellectual property

• Any activities that do not meet the substance or reporting requirements

________________________________________

📊 De Minimis Threshold

A QFZP can still maintain its 0% status even if it earns non-qualifying income, provided the non-qualifying revenue does not exceed:

• 5% of total revenue, or

• AED 5 million,

whichever is lower.

If the threshold is exceeded in any tax period, the entity loses its QFZP status for that period and the next four years.

________________________________________

📑 Reporting and Compliance Requirements

To maintain 0% Corporate Tax on Qualifying Income, a QFZP must:

• Maintain audited financial statements

• Submit Corporate Tax return annually

• Segregate books for qualifying vs. non-qualifying income

• Maintain transfer pricing documentation (Master File, Local File)

• Demonstrate adequate economic substance in the UAE

________________________________________

📌 Summary Table

Category Requirement

Qualifying Income Income from Free Zone Persons and Qualifying Activities

Tax Rate 0% on Qualifying Income, 9% on Non-Qualifying

De Minimis Limit 5% of total revenue or AED 5M

Audited Financials Mandatory

Opt-in for Taxation Not permitted for 0% treatment

Key Laws Article 18, Cabinet Decision 55, Ministerial Decision 139

________________________________________

🧠 Expert Insight by Sheikh Anwar Accounting & Auditing LLC

Many businesses mistakenly believe that simply operating in a Free Zone automatically qualifies them for 0% corporate tax. This is not true. Only businesses that meet all conditions and generate qualifying income are eligible.

At Sheikh Anwar Accounting & Auditing LLC, we help clients:

✅ Assess their eligibility as a QFZP

✅ Structure business activities to optimize tax benefits

✅ Prepare and audit financials

✅ Maintain required documentation for FTA review

✅ File Corporate Tax returns accurately and on time

________________________________________

📞 Contact Us for Free Zone Tax Advisory

Need help determining if your Free Zone business qualifies for 0% corporate tax?

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 Website: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📞 Phone: +971-XX-XXX-XXXX