Example Case Studies of Free Zone Companies

Introduction

The UAE’s free zones offer businesses significant advantages — from 100% foreign ownership and simplified customs processes to competitive tax incentives.

Under the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022), free zone entities can still enjoy a 0% corporate tax rate on qualifying income if they meet the Qualifying Free Zone Person (QFZP) criteria.

Sheikh Anwar Accounting and Auditing LLC explores practical case studies showing how different free zone companies are taxed under the new regime.

________________________________________

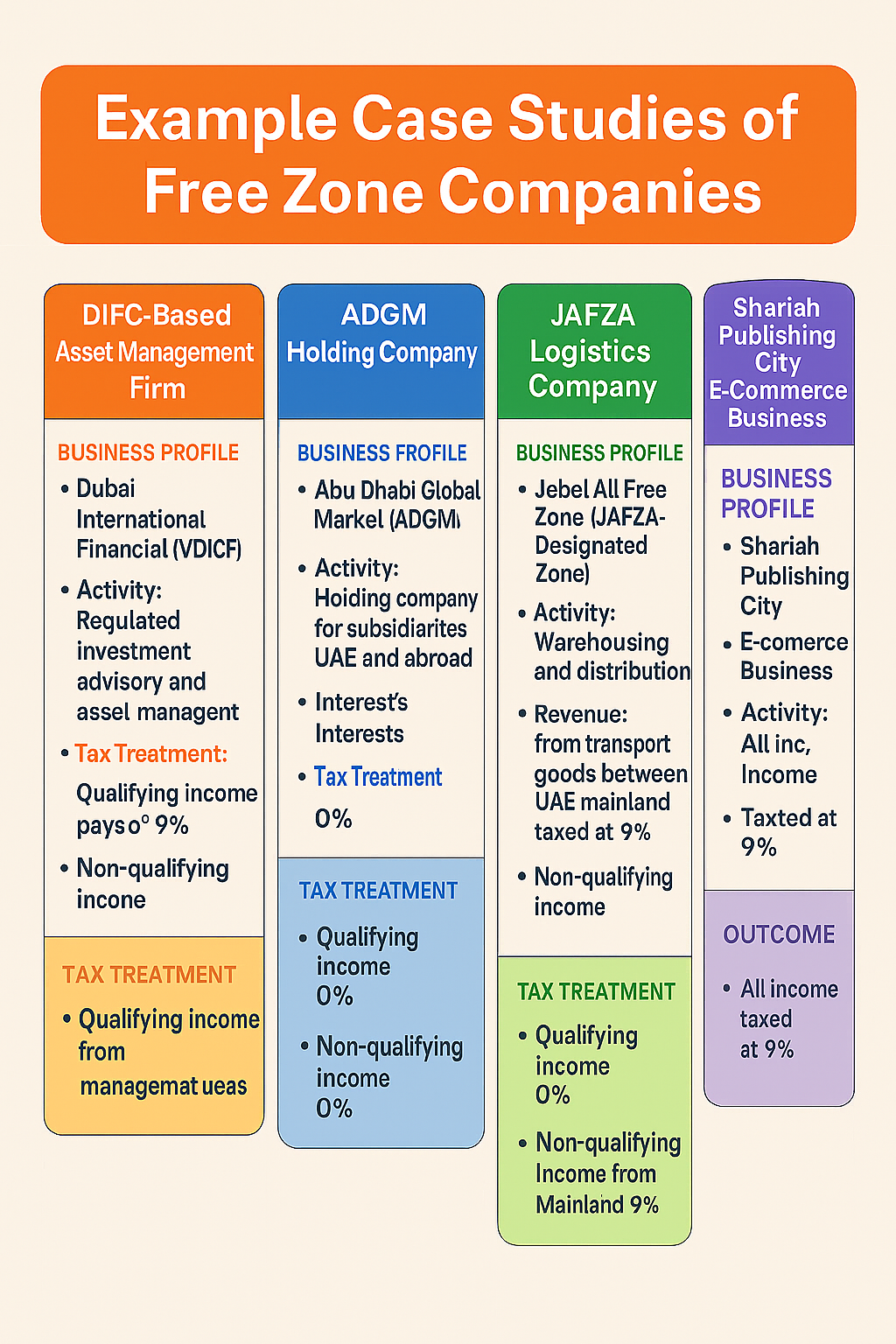

Case Study 1: DIFC-Based Asset Management Firm

Business Profile:

• Location: Dubai International Financial Centre (DIFC)

• Activity: Regulated investment advisory and asset management

• Clients: Mostly foreign investors and other DIFC entities

Tax Treatment:

• Qualifying Income: Fees from portfolio management for foreign clients and other DIFC companies → 0% rate.

• Non-Qualifying Income: None — all income is within qualifying activities.

• Outcome: The firm retains full QFZP status and pays 0% corporate tax on all taxable profits.

Key Compliance Factors:

• Maintains adequate staff and office space in DIFC.

• Files ESR reports and complies with Transfer Pricing rules.

________________________________________

Case Study 2: ADGM Holding Company

Business Profile:

• Location: Abu Dhabi Global Market (ADGM)

• Activity: Holding company for subsidiaries in UAE and abroad

• Revenue: Dividends from foreign subsidiaries, interest on intercompany loans

Tax Treatment:

• Qualifying Income: Dividend and interest income from foreign subsidiaries → 0% rate.

• Non-Qualifying Income: None.

• Outcome: Entire taxable income is exempt under QFZP rules; corporate tax return filed with zero tax payable.

Key Compliance Factors:

• Minimal operational expenses, but meets substance requirements for holding companies.

• Keeps detailed intercompany loan agreements to support TP compliance.

________________________________________

Case Study 3: JAFZA Logistics Company

Business Profile:

• Location: Jebel Ali Free Zone (Designated Zone)

• Activity: Warehousing and distribution of goods to GCC countries

• Customers: Primarily other free zone companies and foreign buyers

Tax Treatment:

• Qualifying Income: Distribution to other free zone companies and exports to foreign clients → 0% rate.

• Non-Qualifying Income: Domestic UAE retail sales (to mainland customers) → taxed at 9%.

• Outcome: Mixed tax position — partial 0% and partial 9% depending on transaction type.

Key Compliance Factors:

• Segregates accounting for qualifying vs. non-qualifying income.

• Maintains proper customs documentation to prove goods left the UAE.

________________________________________

Case Study 4: Dubai Media City Production House

Business Profile:

• Location: Dubai Media City (Non-Designated Free Zone)

• Activity: Produces advertising content for UAE mainland companies

• Revenue: 90% from mainland UAE clients

Tax Treatment:

• Qualifying Income: Minimal, as most work is for mainland clients without meeting qualifying criteria.

• Non-Qualifying Income: Advertising services to mainland → 9% rate.

• Outcome: Company fails de-minimis rule (more than 5% non-qualifying income) and loses QFZP status for the year → taxed at 9% on total income.

Key Compliance Factors:

• Needs to restructure contracts and client base to restore QFZP status.

________________________________________

Case Study 5: Sharjah Publishing City E-Commerce Business

Business Profile:

• Location: Sharjah Publishing City Free Zone

• Activity: Online sales of educational materials to global customers

• Revenue: 80% exports, 20% mainland UAE sales

Tax Treatment:

• Qualifying Income: Export sales to overseas customers → 0% rate.

• Non-Qualifying Income: Mainland UAE sales → taxed at 9%.

• Outcome: Company remains a QFZP as non-qualifying income is within 5% limit.

Key Compliance Factors:

• Maintains clear separation of income sources.

• Keeps detailed shipping and export proof for 0% transactions.

________________________________________

Lessons from These Case Studies

1. Segregate Income Sources – Clearly track qualifying vs. non-qualifying income.

2. Monitor De-Minimis Thresholds – Exceeding them can cost the 0% benefit.

3. Maintain Substance – Physical presence, staffing, and operations matter.

4. Comply with ESR & TP Rules – Documentation is essential for audits.

5. Plan Transactions – Strategic structuring can preserve QFZP status.

________________________________________

Conclusion

Free zone companies still enjoy a powerful tax advantage in the UAE, but compliance is key. The 0% corporate tax rate is available only to those who meet QFZP conditions and manage their income mix carefully.

At Sheikh Anwar Accounting and Auditing LLC, we help free zone businesses across the UAE — from DIFC to JAFZA — maintain compliance and maximise their tax benefits through strategic planning and expert guidance.

📍 Dubai, UAE

🌐 Website: www.sa-auditors.com

📧 Email: info@sa-auditors.com