Economic Substance Requirements and Corporate Tax

Introduction

The UAE’s commitment to global tax transparency and anti-avoidance measures has resulted in the introduction of two key regulatory frameworks:

1. Economic Substance Regulations (ESR)

2. Corporate Tax Law

Although these are separate regimes, they are interconnected, particularly for free zone entities, holding companies, and international structures.

It explains the Economic Substance Requirements, how they relate to UAE Corporate Tax, and what businesses need to do to remain compliant with both.

________________________________________

🧾 Legal Framework

1. Economic Substance Regulations

• Introduced under Cabinet Resolution No. 57 of 2020

• Amended by Ministerial Decision No. 100 of 2020

• Overseen by the Ministry of Finance

2. Corporate Tax Law

• Introduced via Federal Decree-Law No. 47 of 2022

• Enforced by the Federal Tax Authority (FTA)

________________________________________

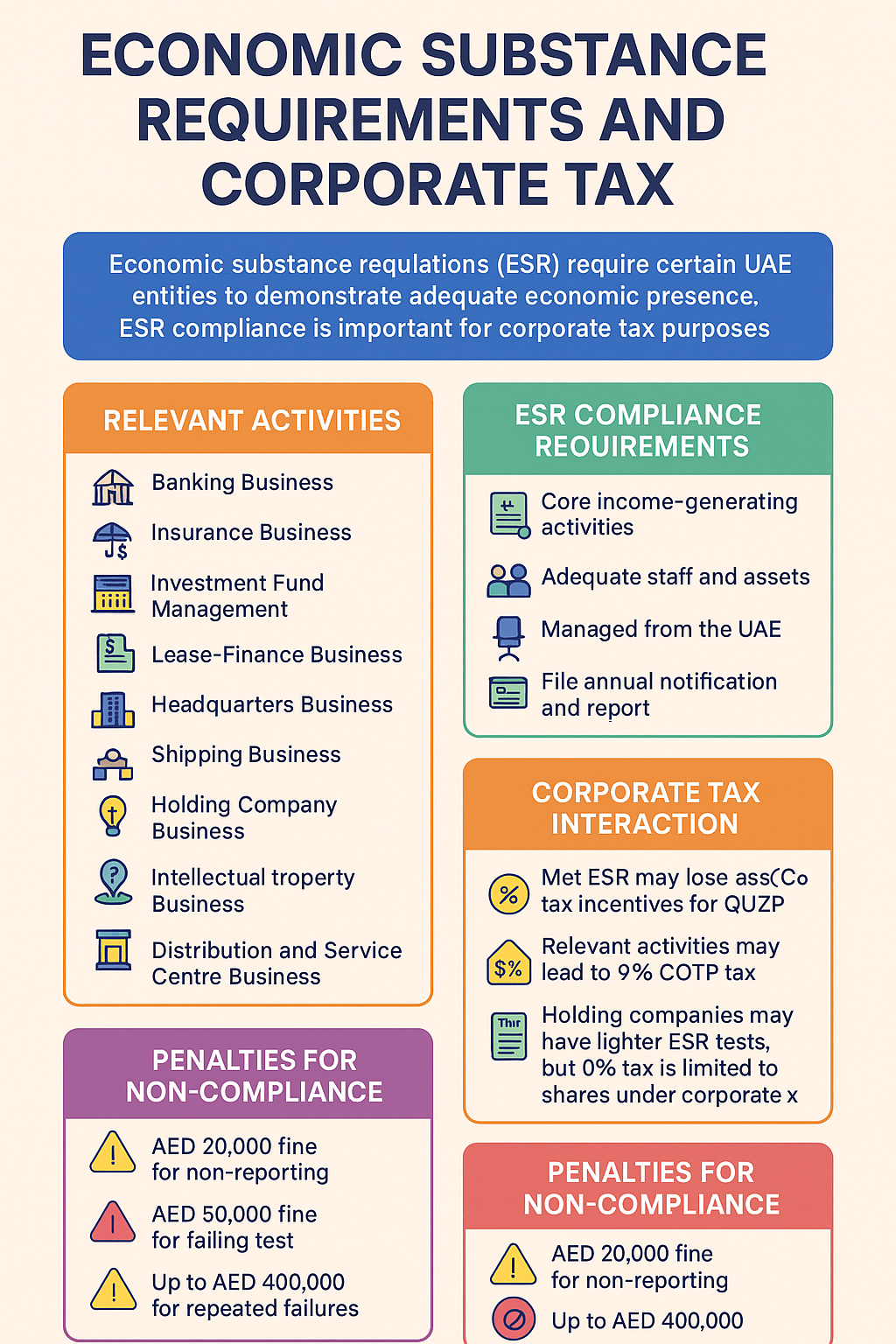

🧩 What are Economic Substance Regulations (ESR)?

ESR require UAE onshore and free zone companies carrying out “Relevant Activities” to:

• Maintain adequate economic presence in the UAE

• Conduct core income-generating activities (CIGAs) in the UAE

• Be directed and managed from within the UAE

• Employ qualified full-time employees

• Have physical offices and operating expenditure in the UAE

________________________________________

✅ Who Must Comply with ESR?

Any UAE-based entity (mainland or free zone) that conducts one or more of the Relevant Activities must comply with ESR, unless it qualifies as an exempt licensee.

________________________________________

🔍 List of “Relevant Activities” under ESR

1. Banking Business

2. Insurance Business

3. Investment Fund Management

4. Lease-Finance Business

5. Headquarters Business

6. Shipping Business

7. Holding Company Business

8. Intellectual Property (IP) Business

9. Distribution and Service Centre Business

Note: Merely holding passive investments (like shares) may fall under "Holding Company Business."

________________________________________

📋 ESR Compliance Requirements

Entities engaged in any of the above must:

• File an ESR Notification annually

• Submit an Economic Substance Report, if not exempt

• Meet substance tests:

o CIGAs performed in the UAE

o Directed and managed from the UAE

o Adequate staff, premises, and expenditure in the UAE

________________________________________

💼 Corporate Tax Interaction with ESR

While ESR applies independently, it has direct implications under the UAE Corporate Tax regime, particularly in the following areas:

________________________________________

🔸 1. Qualifying Free Zone Person (QFZP) Status

To enjoy the 0% Corporate Tax rate, a Free Zone entity must:

• Derive Qualifying Income

• Maintain adequate substance in the Free Zone

This overlaps with ESR, making economic presence a key condition for tax benefits.

FTA will assess ESR compliance when determining whether a Free Zone entity truly qualifies for 0% CT.

________________________________________

🔸 2. Holding Companies and Passive Income

• ESR distinguishes pure holding entities, which have less stringent substance requirements, from other active businesses.

• Under Corporate Tax, holding entities still qualify as Taxable Persons, but may benefit from participation exemption if they hold shares in foreign subsidiaries.

________________________________________

🔸 3. IP and Service Activities

• Businesses that own or license IP must justify UAE presence to avoid being labeled as a high-risk IP business.

• Failure to demonstrate substance can lead to:

o ESR penalties

o Denial of Free Zone tax incentives

o Reclassification as non-Qualifying Free Zone Person

________________________________________

❌ Penalties for Non-Compliance with ESR

• Failure to submit ESR notification: AED 20,000

• Failure to submit report or meet substance: AED 50,000–400,000

• Risk of license being revoked or not renewed

• FTA may deny Corporate Tax exemptions or incentives

________________________________________

🧠 Example Scenarios

📌 Scenario 1: Free Zone Service Company

• Provides consulting services from DMCC

• Has only one employee on paper and operates from a flexi-desk

• Claims 0% CT under QFZP

Risk: May not meet ESR or substance requirements

✅ Action: Increase operational presence to retain CT benefit

________________________________________

📌 Scenario 2: Passive Holding Company

• Holds shares in UAE and foreign companies

• No active income or staff

Outcome: Must file ESR Notification but may qualify as an exempt licensee or meet reduced substance test

________________________________________

📌 Scenario 3: IP-Rich Tech Firm

• Owns patents and earns licensing revenue

• No qualified staff or R&D in UAE

Red flag for ESR and 0% CT status

✅ Action: Establish UAE-based development and management function

________________________________________

🔁 Annual ESR Compliance Calendar

Requirement Deadline

ESR Notification Filing Within 6 months of FY end

ESR Report (if required) Within 12 months of FY end

Corporate Tax Return Filing Within 9 months of FY end

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

We support clients with:

✅ Assessing ESR applicability and classification

✅ Filing ESR Notifications and Reports

✅ Structuring business to meet substance requirements

✅ Coordinating with Corporate Tax planning

✅ Maintaining full FTA and ESR compliance

Let us protect your tax benefits while ensuring regulatory compliance.

________________________________________

📞 Contact Us

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX