Documentation for Maintaining QFZP Status

Introduction

Maintaining your status as a Qualifying Free Zone Person (QFZP) is crucial for continuing to benefit from the 0% corporate tax rate on qualifying income. This outlines the practical documentation and compliance requirements companies must follow under the UAE Corporate Tax regime.

________________________________________

⚖️ Legal Basis

To retain QFZP status, a Free Zone entity must comply with:

• Article 18 of Federal Decree-Law No. 47 of 2022

• Cabinet Decision No. 55 of 2023 (QFZP conditions)

• Ministerial Decision No. 139 of 2023 (Qualifying activities and excluded income)

• Ministerial Decision No. 265 of 2023 (TP documentation)

• FTA's guidance on registration, filing, and annual declaration

Failure to comply with any condition may result in the loss of QFZP status and the application of 9% tax on full income.

________________________________________

🗂️ Key Documentation for QFZP Compliance

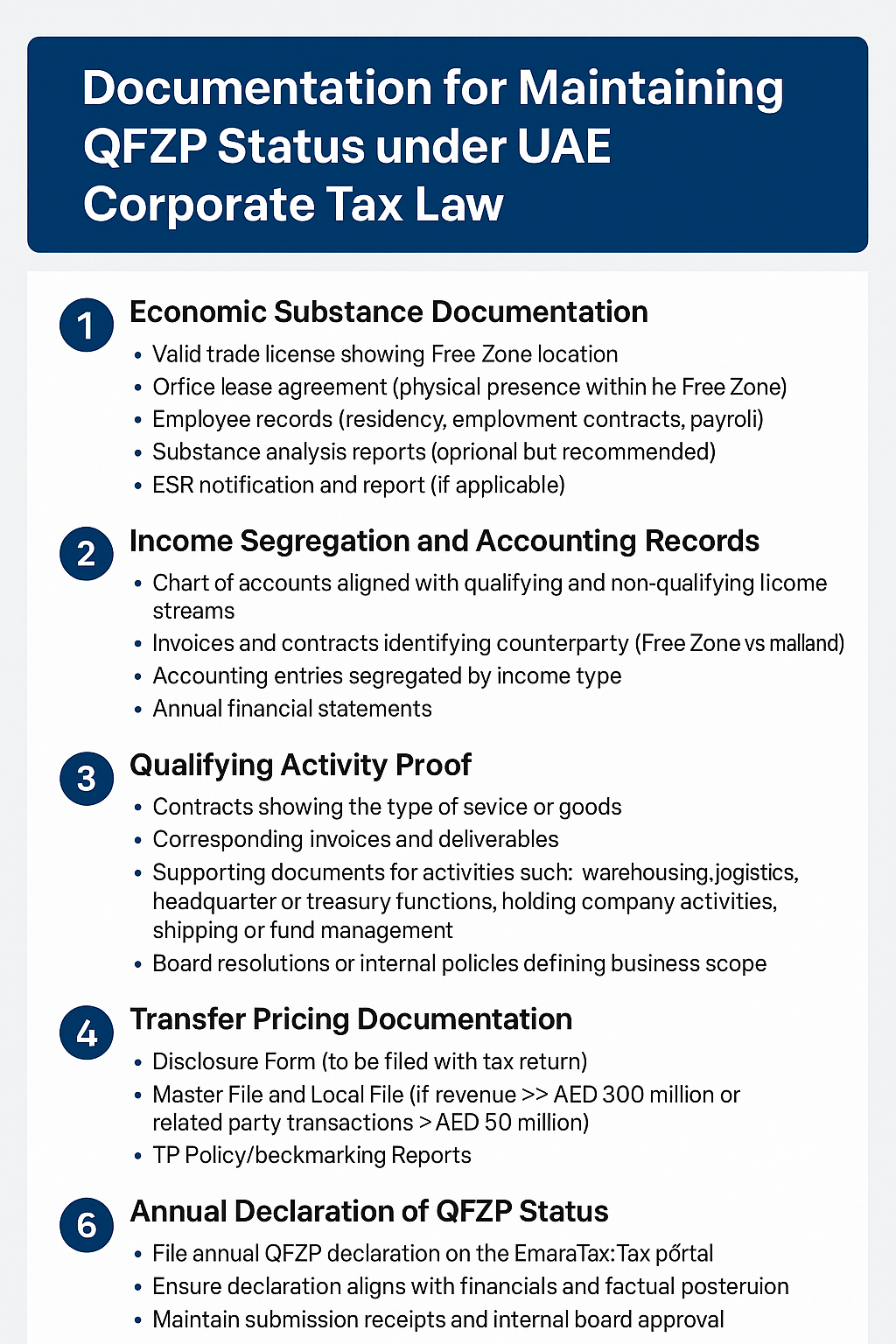

1. Economic Substance Documentation

✅ Purpose: To demonstrate that the entity has adequate presence in the Free Zone.

Documents to maintain:

• Valid trade license showing Free Zone location

• Office lease agreement (physical presence within the Free Zone)

• Employee records (residency, employment contracts, payroll)

• Substance analysis reports (optional but recommended)

• ESR notification and report (if applicable)

________________________________________

2. Income Segregation and Accounting Records

✅ Purpose: To clearly separate qualifying and non-qualifying income.

Required records:

• Chart of accounts aligned with qualifying and non-qualifying income streams

• Invoices and contracts identifying counterparty (Free Zone vs mainland)

• Accounting entries segregated by income type

• Annual financial statements

o Audit report if revenue > AED 50 million

o Internal classification of income as per Article 18(3)

Maintain for 7 years in accordance with UAE tax recordkeeping laws.

________________________________________

3. Qualifying Activity Proof

✅ Purpose: To demonstrate that income is derived from approved qualifying activities.

Documents required:

• Contracts showing the type of service or goods

• Corresponding invoices and deliverables

• Supporting documents for activities such as:

o Warehousing, logistics

o Headquarter or treasury functions

o Holding company activities

o Shipping or fund management

• Board resolutions or internal policies defining business scope

________________________________________

4. Transfer Pricing Documentation

✅ Purpose: To prove that related party and connected person transactions are at arm’s length.

Mandatory if thresholds are met:

• Disclosure Form (to be filed with tax return)

• Master File and Local File (if revenue > AED 200 million or related party transactions > AED 50 million)

• TP Policy/Benchmarking Reports

Maintain supporting agreements (e.g., service agreements, intercompany loans).

________________________________________

5. Annual Declaration of QFZP Status

✅ Purpose: To confirm to FTA that all conditions for QFZP status are met.

Required actions:

• File annual QFZP declaration on the EmaraTax portal

• Ensure the declaration aligns with financials and factual position

• Maintain submission receipts and internal board approval

This is a critical compliance step — failing to submit on time may result in automatic loss of QFZP status.

________________________________________

6. Corporate Tax Return & Related Filings

✅ Purpose: Fulfilling core tax obligations.

• Corporate Tax Registration Certificate

• Timely return filing (within 9 months of end of tax period)

• Backup documentation:

o Return summary

o Payment receipts

o FTA communication logs

________________________________________

📌 Additional Best Practices

• Conduct an annual QFZP eligibility assessment

• Retain meeting minutes approving qualifying transactions

• Establish a TP policy even if not legally required (for transparency)

• Regularly review FTA guidance and update documentation

• Keep a QFZP compliance file with all key records in one place

________________________________________

🚨 Consequences of Non-Compliance

Risk Area Consequence

Failure to meet substance Loss of QFZP status & 9% tax on full income

Misclassified income Tax on non-qualifying income + penalties

Missing declaration Disqualification + administrative penalties

TP non-compliance TP adjustments + penalties

________________________________________

🧾 Conclusion

Maintaining QFZP status is not just a one-time setup—it requires ongoing documentation, procedural discipline, and annual filings. Failure to comply with any single requirement could jeopardize the 0% corporate tax benefit.

________________________________________

🧑💼 Need Professional Help?

If your business needs assistance with QFZP documentation, tax return filing, or Transfer Pricing compliance, reach out to:

📧 Email: info@sa-auditors.com

🌐 Website: https://www.sa-auditors.com