Difference Between RCM and Forward Charge

Introduction

Understanding the difference between Reverse Charge Mechanism (RCM) and the Forward Charge mechanism is essential for businesses operating in the UAE under the VAT regime. Misapplying either can lead to compliance risks, incorrect VAT returns, and penalties from the Federal Tax Authority (FTA).

It provides a comprehensive comparison of both mechanisms, their applicability, key differences, and examples under the UAE VAT law.

________________________________________

✅ What is Forward Charge?

Under the Forward Charge Mechanism, the supplier of goods or services is responsible for:

• Charging VAT on the invoice.

• Collecting VAT from the customer.

• Paying the collected VAT to the FTA.

This is the default VAT system for most domestic transactions in the UAE.

🧾 Example of Forward Charge:

A Dubai-based IT company provides services to another UAE-based business:

• Invoice: AED 10,000 + AED 500 (5% VAT)

• The supplier collects AED 500 VAT from the buyer and remits it to the FTA.

________________________________________

🔄 What is Reverse Charge Mechanism (RCM)?

Under the Reverse Charge Mechanism, the recipient (buyer/importer) of goods or services:

• Accounts for VAT on behalf of the non-resident supplier.

• Reports the VAT in both output and input tax sections of the VAT return.

• Pays VAT directly to the FTA (if not recoverable).

RCM is mainly used in:

• Cross-border transactions (imports of goods and services).

• Domestic supplies of specific goods (like gold, crude oil, hydrocarbons) as per Cabinet Decision No. 59 of 2017.

📥 Example of RCM:

A UAE-based company purchases consultancy services from a non-registered UK firm:

• The UK firm does not charge VAT.

• The UAE company self-accounts for VAT (reverse charge) and reports it in their VAT return.

________________________________________

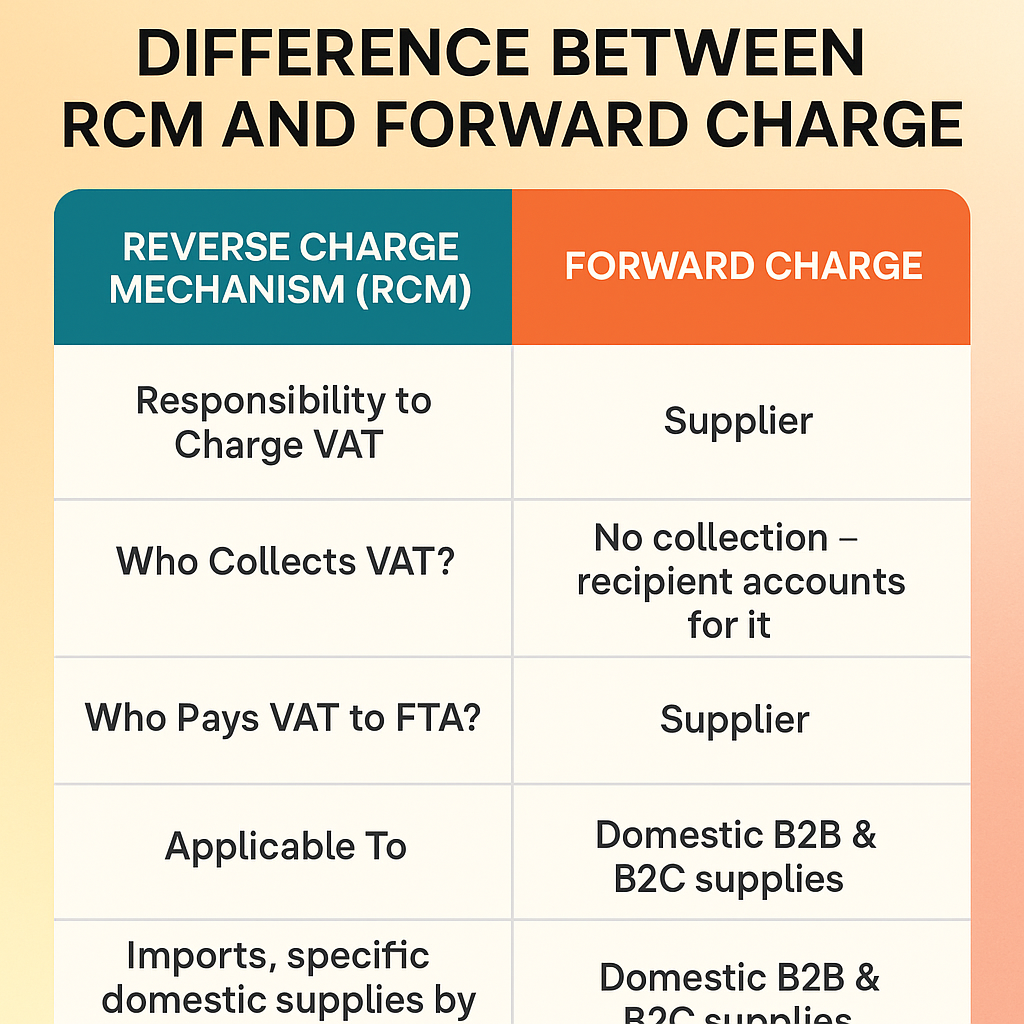

📊 Key Differences Between Forward Charge and RCM

Feature Forward Charge Reverse Charge Mechanism (RCM)

Responsibility to Charge VAT Supplier Recipient (buyer/importer)

Who Collects VAT? Supplier No collection – recipient accounts for it

Who Pays VAT to FTA? Supplier Recipient

Applicable To Domestic B2B & B2C supplies Imports, specific domestic supplies by non-residents or listed sectors

Invoice Format Includes VAT charged by supplier No VAT on supplier’s invoice, VAT noted by buyer

VAT Registration of Supplier Supplier must be VAT registered Supplier can be non-registered/non-resident

Input Tax Recovery Recipient can recover if eligible Usually recoverable by recipient in same VAT return

FTA Reporting Reported by supplier Reported by recipient under Box 3 & Box 10 in VAT 201 return

________________________________________

📝 Legal References

• Federal Decree-Law No. 8 of 2017 on VAT

• Cabinet Decision No. 52 of 2017 (Executive Regulations)

• Cabinet Decision No. 59 of 2017 on RCM-specific supplies

• FTA VAT Guide and Clarifications

________________________________________

🧠 Practical Tips for Businesses

🔹 Always verify if your supplier is UAE VAT registered.

🔹 For imports, review contracts and invoices to determine if RCM applies.

🔹 Maintain clear documentation to support your VAT treatment.

🔹 Consult tax professionals if dealing with non-resident suppliers or cross-border supplies.

________________________________________

📌 Conclusion

While the Forward Charge is the most common VAT application for domestic transactions, the Reverse Charge Mechanism plays a critical role in ensuring VAT compliance for imports and specified high-risk sectors. Both mechanisms are complementary and help plug revenue leakages in the VAT system.

💡 Businesses must understand which mechanism applies to which transaction to ensure accurate reporting and avoid VAT penalties.

🌐 Visit us: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📱 WhatsApp: +971-XX-XXXXXXX