Corporate Tax Treatment for DIFC Entities

Introduction

The Dubai International Financial Centre (DIFC) is one of the UAE’s most prominent free zones, serving as a hub for banking, asset management, fintech, law, and professional services. Known for its independent legal system based on English common law, the DIFC offers global businesses a gateway to the Middle East, Africa, and South Asia.

With the introduction of the UAE Corporate Tax regime under Federal Decree-Law No. 47 of 2022, all DIFC-registered companies now fall within the scope of UAE corporate tax — but certain tax incentives remain available for those who meet the Qualifying Free Zone Person (QFZP) criteria.

________________________________________

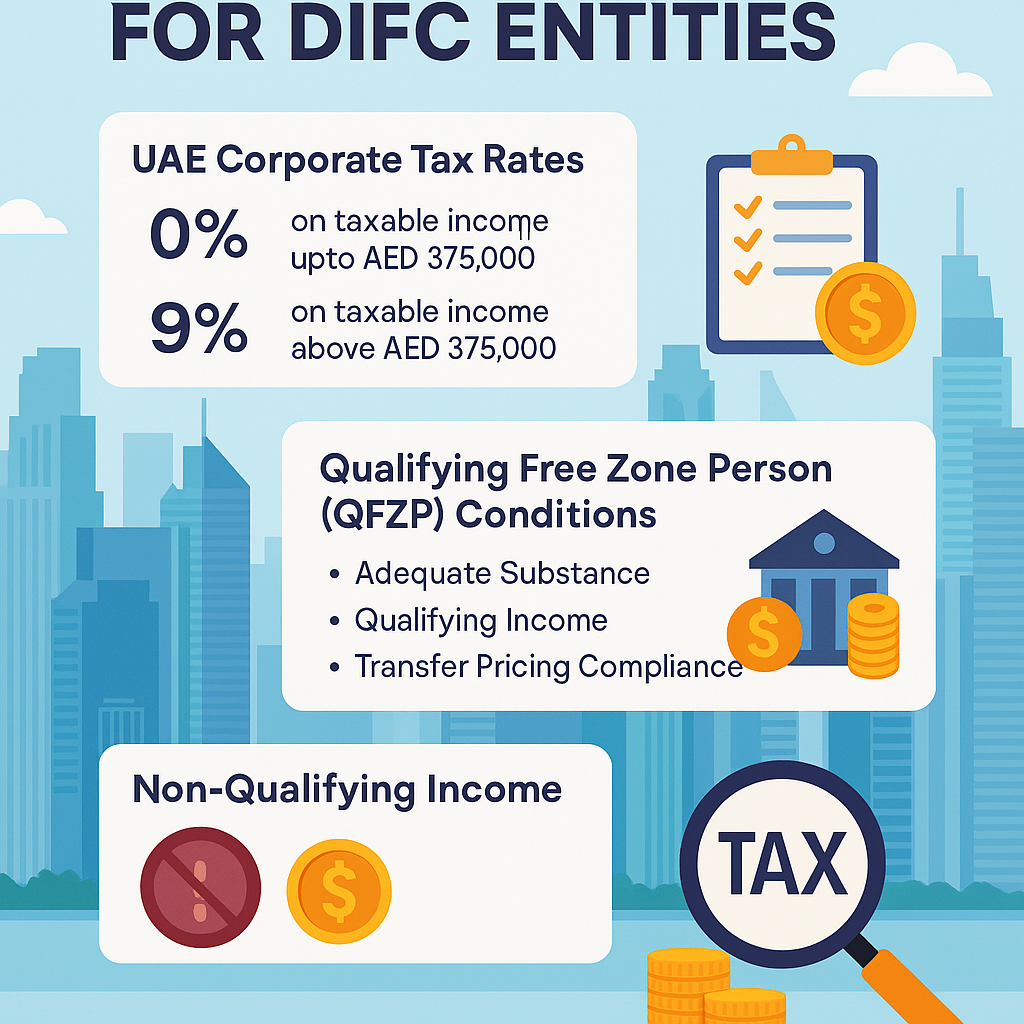

1. Applicability of UAE Corporate Tax to DIFC Entities

• General Rule: All companies in the UAE, including those in free zones like the DIFC, are subject to UAE corporate tax.

• Free Zone Incentive: DIFC companies that qualify as QFZPs are eligible for a 0% corporate tax rate on qualifying income.

• Taxable Income Rates:

o 0% on taxable income up to AED 375,000 (for all businesses).

o 9% on taxable income above AED 375,000 (unless exempted as QFZP on qualifying income).

________________________________________

2. Qualifying Free Zone Person (QFZP) Status

To benefit from the 0% corporate tax rate, a DIFC entity must meet all of the following conditions:

a) Adequate Substance in DIFC

The company must demonstrate real operational presence:

• Maintain a physical office in DIFC.

• Employ qualified employees.

• Incur operating expenses in proportion to business activity.

b) Earn Qualifying Income

Income must be derived from Qualifying Activities specified in Cabinet Decision No. 55 of 2023 and Ministerial Decision No. 265 of 2023, including:

• Regulated financial services (banking, insurance, investment management, brokerage).

• Wealth and asset management.

• Holding company activities.

• Headquarter services to related parties.

• Treasury and financing services to related parties.

• Certain distribution activities within or from a Designated Zone.

• Certain intellectual property activities.

c) Comply with Transfer Pricing Requirements

• Related-party transactions must follow the Arm’s Length Principle.

• Maintain Transfer Pricing documentation (Master File, Local File) where applicable.

d) Meet Economic Substance Regulations (ESR)

• File ESR Notifications and Reports with the Ministry of Finance.

e) Stay Within Non-Qualifying Income Limits

• Non-qualifying income must not exceed 5% of total revenue or AED 5 million, whichever is lower.

f) No Voluntary Election for Mainland Tax

The entity must not opt out of QFZP benefits by choosing standard corporate tax rates.

________________________________________

3. Qualifying vs. Non-Qualifying Income

Income Type Tax Rate

Transactions with other free zone persons for qualifying activities 0%

Qualifying transactions with mainland UAE customers (as permitted by law) 0%

Passive income from mainland (interest, dividends, royalties) 0%

Non-qualifying activities (e.g., retail to mainland customers) 9%

Income from excluded activities (natural resource extraction, certain IP) 9%

________________________________________

4. Corporate Tax Registration for DIFC Companies

All DIFC entities — whether benefiting from 0% or not — must:

• Register with the Federal Tax Authority (FTA) for corporate tax.

• Obtain a Tax Registration Number (TRN).

• File annual corporate tax returns through the EmaraTax portal.

• Maintain IFRS-compliant financial statements.

• Have audited accounts (mandatory under DIFC rules).

________________________________________

5. Compliance Timeline

1. Registration Deadline: Check your FTA-assigned deadline based on trade licence issue date.

2. Tax Return Filing: Within 9 months of the end of the relevant tax period.

3. Payment Deadline: Same as return filing deadline.

4. Record Keeping: Minimum 7 years.

________________________________________

6. Consequences of Losing QFZP Status

If a DIFC company fails to meet the QFZP conditions:

• The 0% rate is lost for the relevant tax period.

• 9% corporate tax applies to the entire taxable income.

• Loss of status may also impact future eligibility.

• FTA can impose administrative penalties for non-compliance.

________________________________________

7. Strategic Planning for DIFC Entities

To ensure maximum tax efficiency while remaining compliant:

• Conduct annual QFZP status reviews.

• Structure transactions to maintain qualifying income thresholds.

• Ensure economic substance is demonstrable.

• Keep transfer pricing documentation ready for audit.

• Maintain a tax calendar to avoid late filings.

________________________________________

8. Professional Assistance for DIFC Corporate Tax Compliance

The rules for QFZP eligibility are complex and evolving. An error can lead to substantial tax liabilities and penalties.

At Sheikh Anwar Accounting and Auditing LLC, we help DIFC entities by:

• Assessing QFZP eligibility.

• Advising on transaction structuring to protect the 0% benefit.

• Preparing corporate tax returns.

• Ensuring ESR and transfer pricing compliance.

• Providing ongoing advisory for regulatory changes.

📍 Dubai, UAE

🌐 Website: www.sa-auditors.com

📧 Email: info@sa-auditors.com