Corporate Tax Residency Rules

Introduction

With the implementation of Corporate Tax in the UAE, understanding tax residency rules is critical for businesses and individuals to determine their tax obligations. The tax residency status of a person or entity defines which jurisdiction has the right to tax their income and under what conditions.

Here, we explain the concept of tax residency, who qualifies as a resident or non-resident for Corporate Tax purposes, and the implications under Federal Decree-Law No. 47 of 2022.

________________________________________

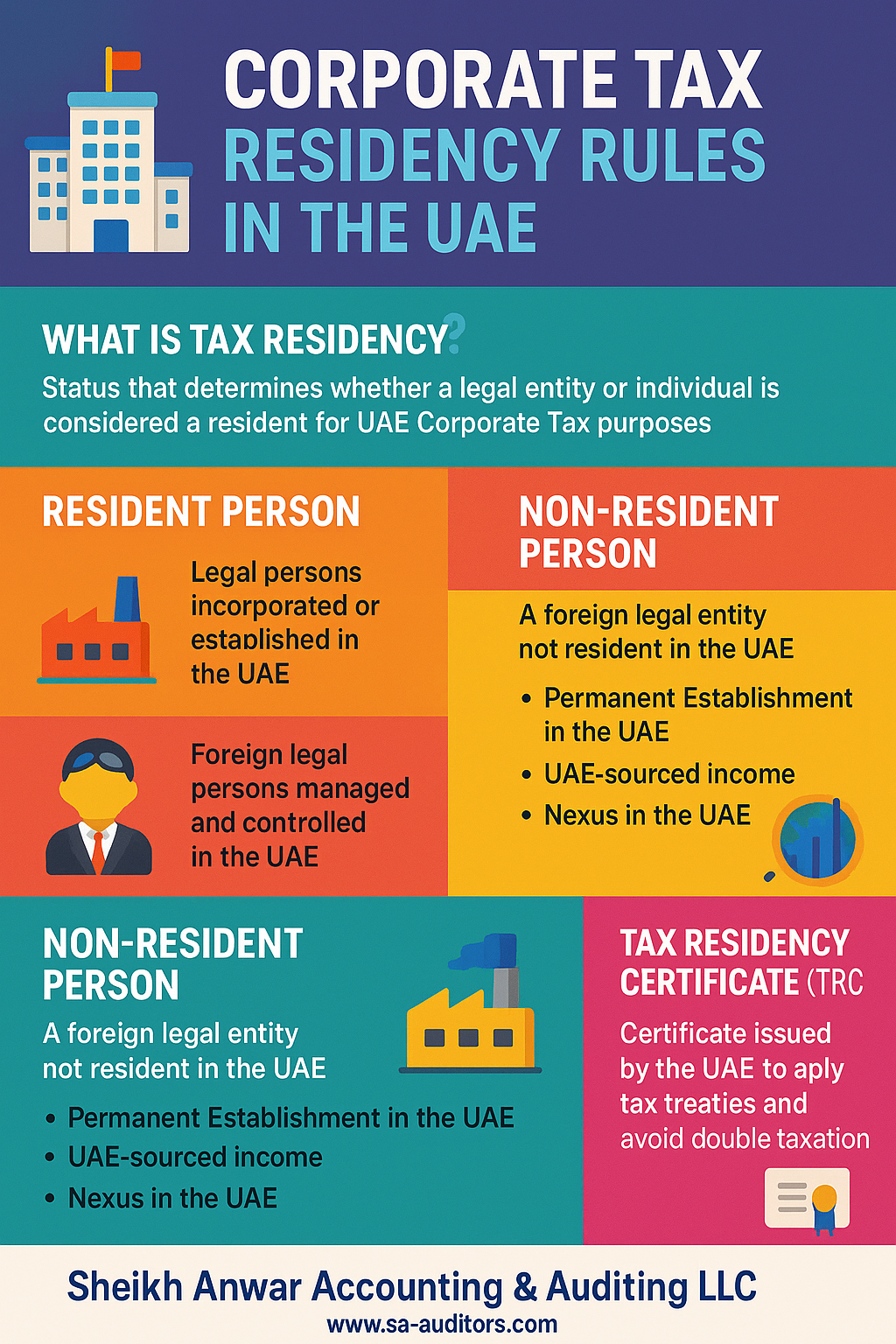

🧾 What Is Tax Residency?

Tax residency refers to the status that determines whether a legal entity or individual is considered a resident for UAE Corporate Tax purposes. This classification dictates the scope of taxation:

• Resident Persons: Taxed on worldwide income (unless exempt).

• Non-Resident Persons: Taxed only on UAE-sourced income.

________________________________________

🏢 Who Is a Resident Person for Corporate Tax?

According to Article 11 of UAE Corporate Tax Law, a Resident Person includes:

1. Legal Persons Incorporated or Established in the UAE

• Mainland companies, Free Zone entities, branches, etc.

2. Foreign Legal Persons Managed and Controlled in the UAE

• Even if incorporated abroad, if the entity is effectively managed and controlled from within the UAE, it is considered tax resident.

3. Natural Persons (Individuals) Conducting Business in the UAE

• If an individual is carrying on a business or professional activity, and earns more than AED 1 million in annual turnover, they are tax residents for CT purposes.

________________________________________

🌍 Who Is a Non-Resident Person?

A Non-Resident Person is:

1. A foreign legal entity that is not incorporated in the UAE and is not managed and controlled from the UAE, but:

o Has a Permanent Establishment (PE) in the UAE, or

o Derives UAE-sourced income, or

o Has a Nexus in the UAE as defined by Cabinet Decision No. 56 of 2023

________________________________________

🧠 “Managed and Controlled” Test – Explained

This is a substance-based test. A foreign company is managed and controlled in the UAE if:

• Strategic decisions are made in the UAE.

• Board meetings and senior management are based in the UAE.

• Day-to-day operations and decision-making take place in the UAE.

Example: A British company whose key decision-making and executive functions are conducted from its UAE office may be treated as a UAE tax resident.

________________________________________

🏢 Permanent Establishment (PE) – Non-Resident Persons

A non-resident person will be subject to UAE Corporate Tax if they have a Permanent Establishment (PE) in the UAE. This can include:

• A fixed place of business (e.g., branch, office, factory)

• A dependent agent acting on their behalf in the UAE

The concept of PE is in line with OECD guidelines and international tax treaties.

________________________________________

🌐 Tax Residency Certificate (TRC)

Businesses and individuals may apply for a Tax Residency Certificate from the UAE Ministry of Finance to:

• Claim tax treaty benefits

• Avoid double taxation

• Prove UAE tax residency to foreign authorities

TRC is separate from Corporate Tax registration. It is typically valid for 1 year and requires:

• Audited financials

• Valid Emirates ID and visa

• Lease agreement

• Proof of physical presence and substance

________________________________________

📝 Corporate Tax Impact Based on Residency

Person Type Tax Residency Tax Scope

UAE-incorporated legal entity Resident Taxed on worldwide income

Foreign company managed in UAE Resident Taxed on worldwide income

UAE-branch of foreign company Non-resident Taxed on UAE-sourced income

Foreign company with PE in UAE Non-resident Taxed on PE income in UAE

UAE individual with business > AED 1M Resident Taxed on business income

________________________________________

⚠️ Key Compliance Notes

• Resident persons must register for Corporate Tax, maintain records, and file returns annually.

• Non-residents with UAE-source income must withhold taxes, maintain records, and register if PE or Nexus exists.

• Misclassifying tax residency can lead to non-compliance penalties and audit risks.

________________________________________

🧾 UAE Tax Residency vs International Residency

• The UAE Corporate Tax residency rules are separate from immigration (visa) or personal tax residency rules in other countries.

• Being a UAE tax resident does not automatically exempt you from being taxed abroad unless tax treaties apply.

________________________________________

🧠 Expert Insight from Sheikh Anwar Accounting & Auditing LLC

At Sheikh Anwar Accounting & Auditing LLC, we help clients:

• Assess and determine their correct tax residency status

• Structure cross-border operations to avoid double taxation

• Apply for Tax Residency Certificates

• Remain compliant with UAE Corporate Tax Law, PE rules, and international tax obligations

________________________________________

📞 Need Guidance?

Contact us today at

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX