Corporate Tax on Partnerships

Introduction

With the enforcement of UAE Corporate Tax Law under Federal Decree-Law No. 47 of 2022, all business structures—including partnerships—must assess their tax obligations. The tax treatment of partnerships in the UAE depends on the legal nature of the partnership, the type of partners, and whether the entity has separate legal personality.

Here, we break down how General Partnerships, Limited Partnerships, and Unincorporated Joint Ventures are taxed under UAE Corporate Tax Law.

________________________________________

📚 Legal Reference

The applicable law is:

• Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses

• Article 15 – Treatment of Unincorporated Partnerships

• Ministerial Decision No. 126 of 2023

• FTA Guidance Notes and Clarifications

________________________________________

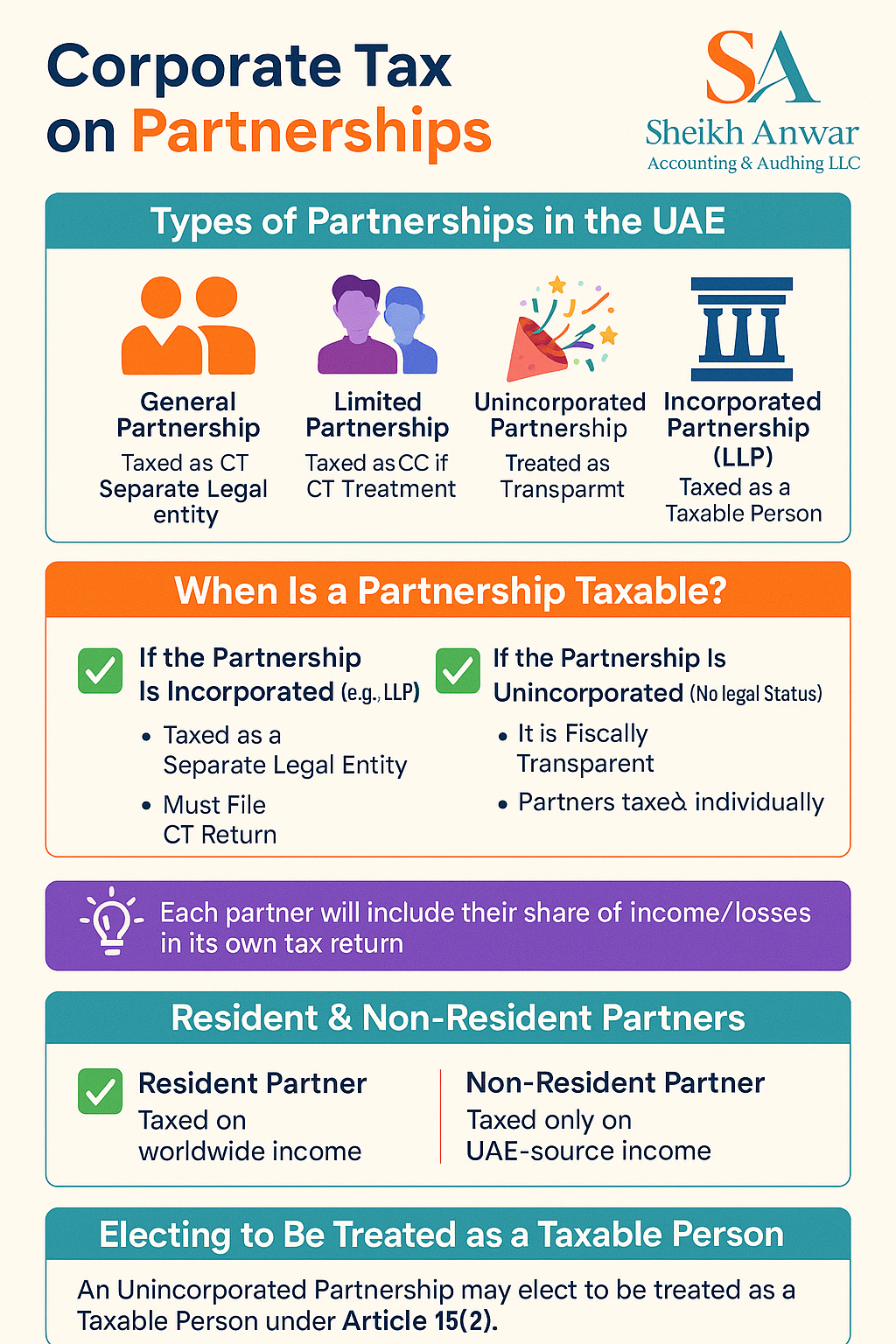

🔍 Types of Partnerships in the UAE

Partnership Type Legal Status CT Treatment

General Partnership (GP) No separate legal entity Partners are taxed individually

Limited Partnership (LP) Depends on structure May be taxed at entity level or partners

Unincorporated Partnership No legal personality Treated as transparent for tax

Incorporated Partnership (LLP) Has legal personality Taxed as a separate taxable person

Joint Venture/Consortium Often informal/unregistered Transparent if no legal personality

________________________________________

🧾 When Is a Partnership Taxable in the UAE?

✅ 1. If the Partnership Is Incorporated (e.g., LLP or Company Form)

• If the partnership is registered as a legal person under UAE law (e.g., as an LLC or LLP), it is treated as a taxable person and subject to Corporate Tax as a company.

Tax Rate: 9% on taxable income exceeding AED 375,000

Registration: Must obtain a TRN and file CT returns annually

________________________________________

✅ 2. If the Partnership Is Unincorporated (No Separate Legal Status)

These are fiscally transparent. The partners are taxed individually, not the partnership itself.

• Each partner must account for their share of income, losses, and deductions

• No separate CT return is filed for the partnership entity

• This applies to general partnerships, unregistered joint ventures, and some limited partnerships

Tax Rate: Tax is applied at the partner level depending on whether the partner is a natural person or a juridical person

________________________________________

📌 Important: Who Files the Return?

Partnership Type Corporate Tax Registration Who Files Return?

LLP / Incorporated Partnership ✅ Yes The partnership (as a legal person)

Unincorporated GP / JV ❌ No Each partner separately

LP with legal registration ✅ Yes (if legal entity) The entity or partners, based on form

________________________________________

👥 Resident vs. Non-Resident Partners

• If the partner is a UAE resident person (individual or entity), they are taxed on their worldwide income share from the partnership.

• If the partner is non-resident, they are taxed only on UAE-source income, e.g., via Permanent Establishment or Nexus.

________________________________________

💡 Electing to Be Treated as a Taxable Person

Under Article 15(2), an unincorporated partnership may elect to be treated as a taxable person by:

• Filing an election with the Federal Tax Authority (FTA)

• Satisfying administrative and record-keeping requirements

Why Elect?

For ease of administration, centralized tax filing, or if partners are foreign investors who want the partnership to manage UAE tax obligations.

________________________________________

✅ Benefits of Transparency (Unincorporated Status)

• Avoids double taxation

• Partners retain flexibility in tax planning

• Simpler for small ventures or short-term projects

________________________________________

🚫 Risks and Challenges

• Unclear ownership may lead to disputes or audit issues

• Each partner must maintain accurate tax records

• Cannot benefit from group taxation or loss transfers

• May create complexity if partners are based in multiple jurisdictions

________________________________________

🧠 Example Scenarios

📌 Scenario 1: Unincorporated General Partnership

• Two individuals form a partnership to operate a small trading business in Dubai.

• No LLC or legal entity is formed.

• Partnership income: AED 600,000

• Each partner will include their share (AED 300,000) in their individual Corporate Tax return. The partnership itself is not taxed.

📌 Scenario 2: LLP Registered in Abu Dhabi

• A legal partnership firm registered as an LLP with 3 partners.

• It has a trade license and separate legal personality.

• Taxable as a Resident Person under Corporate Tax Law

• Files a Corporate Tax return as a legal entity

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

We assist businesses in:

✅ Identifying the correct partnership structure

✅ Determining whether the partnership or the partners are taxable

✅ Corporate Tax registration and return filing

✅ Drafting elections under Article 15(2)

✅ Advising on transparent vs taxable treatment

________________________________________

📞 Contact Us

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX