Corporate Tax in Group Holding Structures

The introduction of Corporate Tax (CT) in the UAE has reshaped how businesses plan their structures, particularly group holding companies. Holding structures—where a parent entity owns shares in subsidiaries—are widely used in the UAE across industries such as real estate, trading, gold & diamonds, and services. These setups allow for centralized ownership, better governance, and tax efficiency.

With the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) and subsequent Cabinet Decisions, holding companies and their subsidiaries must carefully analyze their tax positions, exemptions, and group relief options.

________________________________________

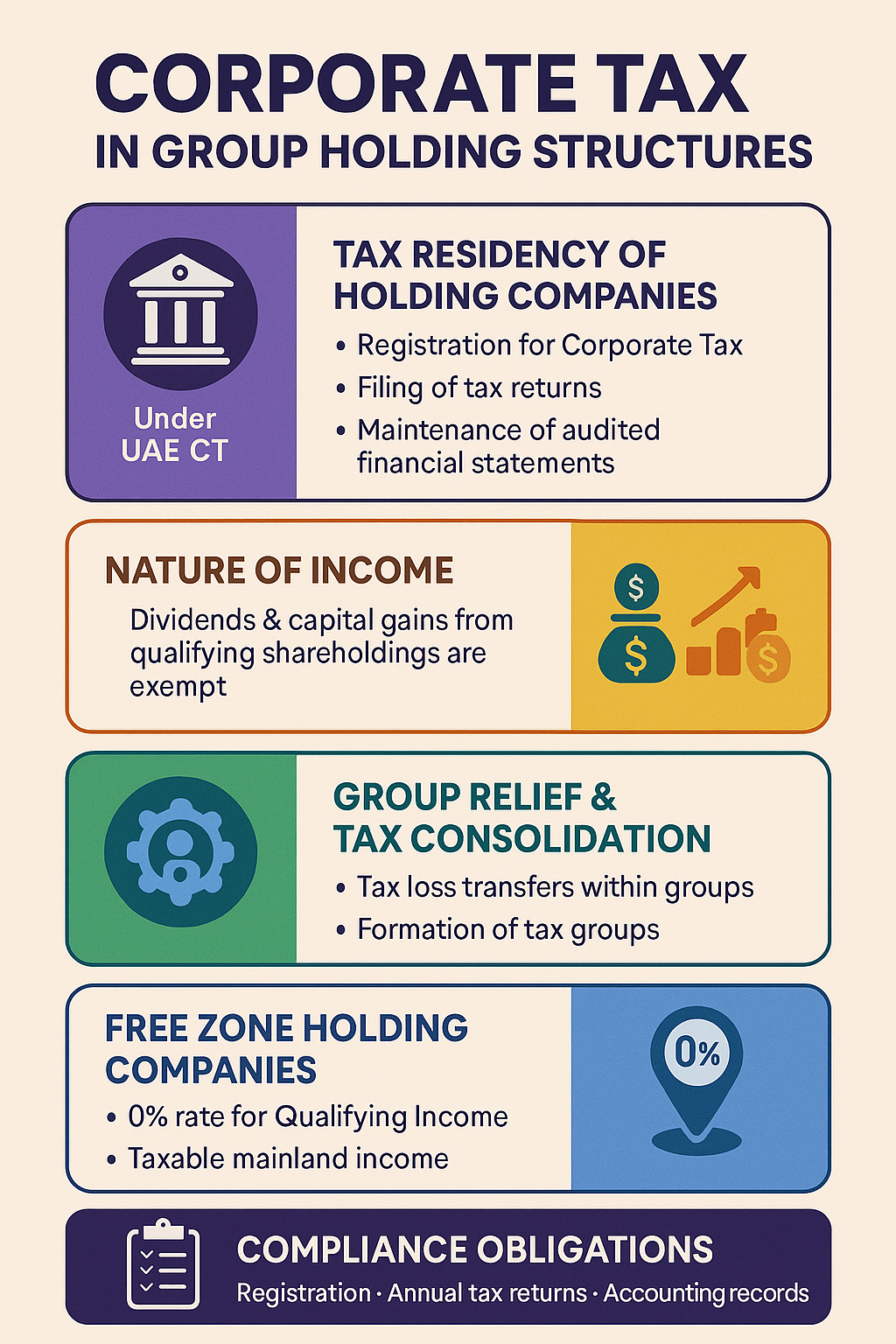

1. Tax Residency of Holding Companies

A holding company incorporated in the UAE is automatically considered a Resident Person and falls under the scope of UAE Corporate Tax. Even if the entity only holds investments and does not carry out “active” trading, it may still have obligations such as:

• Registration for Corporate Tax.

• Filing of CT returns (even if exempt income applies).

• Maintenance of audited financial statements (as required for groups exceeding thresholds).

________________________________________

2. Nature of Income in Holding Companies

Holding companies typically earn passive income, such as:

• Dividends from subsidiaries.

• Capital gains from disposal of shares.

• Royalties from intellectual property.

• Management or service fees charged to group entities.

Exemption Rules:

• Dividends & Capital Gains: Exempt from CT if earned from a Qualifying Shareholding (ownership of at least 5% in a legal entity meeting certain substance and tax requirements).

• Foreign Subsidiaries: Relief applies if the foreign entity is subject to tax of at least 9% (or an acceptable equivalent).

• Royalties & Service Income: Generally taxable at 9%, unless qualifying for group relief.

________________________________________

3. Group Relief & Tax Consolidation

One of the most beneficial aspects of UAE CT for holding structures is the possibility of group taxation:

• Group Relief (Loss Transfer): Tax losses from one group company can be transferred to another, provided common ownership conditions (≥75%) are met.

• Tax Grouping: Two or more companies can apply to be treated as a single taxable person, simplifying filing and allowing intra-group neutrality.

• Intra-group Transfers: Transfers of assets and liabilities between group companies can be made tax neutral if the qualifying ownership conditions are met.

This means that holding structures can significantly reduce effective tax burdens if properly planned.

________________________________________

4. Free Zone Holding Companies

Many UAE businesses use Free Zone Holding Companies (e.g., in DMCC, JAFZA, IFZA, ADGM, DIFC) to own shares in local or foreign subsidiaries.

• Qualifying Free Zone Person (QFZP): If the holding company meets substance rules and earns only “Qualifying Income” (e.g., dividends, capital gains, and income from foreign permanent establishments), it may enjoy a 0% CT rate.

• Non-Qualifying Income: Interest, royalties, or management fees charged to mainland subsidiaries may be subject to 9% CT.

• Careful Structuring Needed: To maintain QFZP status, holding companies must avoid tainting income streams.

________________________________________

5. Compliance Obligations

Even if a holding company primarily earns exempt income, it must:

• Register for Corporate Tax (no exemptions from registration).

• File annual CT returns.

• Maintain adequate accounting records.

• Substantiate economic substance (especially for free zone entities claiming 0%).

Failure to comply may result in penalties and potential disqualification from tax benefits.

________________________________________

6. Strategic Considerations for Groups

When designing or restructuring holding company setups under UAE CT, businesses should consider:

• Location of Holding Company: Mainland vs Free Zone impacts taxation.

• Type of Income: Whether mostly dividends/capital gains (exempt) or management/royalty income (taxable).

• Foreign Subsidiaries: Ensure they qualify for exemption to avoid double taxation.

• Group Relief Options: Explore forming a tax group to consolidate profits and losses.

• Transfer Pricing: Intra-group transactions must comply with arm’s length pricing and documentation requirements.

________________________________________

Conclusion

The UAE Corporate Tax framework offers both opportunities and risks for group holding structures. While exemptions on dividends and capital gains can preserve tax efficiency, businesses must comply with registration, filing, and substance rules. Strategic use of group relief and careful income structuring can optimize tax outcomes.

Holding companies in the UAE should revisit their structures now, ensuring alignment with Corporate Tax law and avoiding penalties. With the right planning, a UAE holding structure remains a powerful tool for tax efficiency, asset protection, and growth.

________________________________________

✍️ Sheikh Anwar Accounting & Auditing LLC

📍 Dubai, UAE | 🌐 www.sa-auditors.com

📧 info@sa-auditors.com