Corporate Tax Forecasting and Budgeting

Introduction

With the introduction of corporate tax in the UAE (effective from 1 June 2023) and increasing global tax regulations, businesses can no longer afford to leave tax management as a year-end exercise. Instead, corporate tax forecasting and budgeting have become essential for effective financial planning, compliance, and long-term growth.

This blog explores why tax forecasting matters, key steps in preparing a tax budget, and best practices for businesses in the UAE.

________________________________________

What is Corporate Tax Forecasting and Budgeting?

• Corporate Tax Forecasting: Estimating a company’s future tax liabilities based on projected revenues, expenses, deductions, and tax rules.

• Tax Budgeting: Integrating these forecasts into the company’s overall budget to allocate funds for timely tax payments and avoid liquidity shocks.

Together, they ensure that businesses not only comply with regulations but also strategically manage cash flows and optimize resources.

________________________________________

Why Corporate Tax Forecasting is Important

1. Cash Flow Management

– Helps avoid sudden tax burdens that disrupt working capital.

2. Compliance Assurance

– Ensures companies meet FTA filing deadlines and avoid penalties.

3. Strategic Planning

– Provides insight into the impact of growth strategies, acquisitions, and new investments on tax obligations.

4. Free Zone Incentives

– Assesses whether the business qualifies as a Qualifying Free Zone Person (QFZP) to avail the 0% tax rate on eligible income.

5. Shareholder Confidence

– Transparent tax planning strengthens governance and investor trust.

________________________________________

Key Elements of Tax Forecasting

1. Revenue Projections

• Forecasting turnover for the year.

• Considering different tax rates (0% on QFZP eligible income, 9% on mainland/non-qualifying income).

2. Deductible & Non-Deductible Expenses

• Identifying which expenses are fully deductible, partially deductible (e.g., entertainment, interest expense caps), or disallowed.

3. Related Party Transactions

• Reviewing transfer pricing adjustments and impact of related party dealings.

4. Loss Utilization

• Assessing carried forward tax losses and offsetting future taxable income.

5. Group Relief & Restructuring

• Evaluating whether group relief or intra-group transfers apply to reduce taxable income.

6. Tax Incentives & Exemptions

• Free Zone exemptions, participation exemption (dividends, capital gains from qualifying holdings).

________________________________________

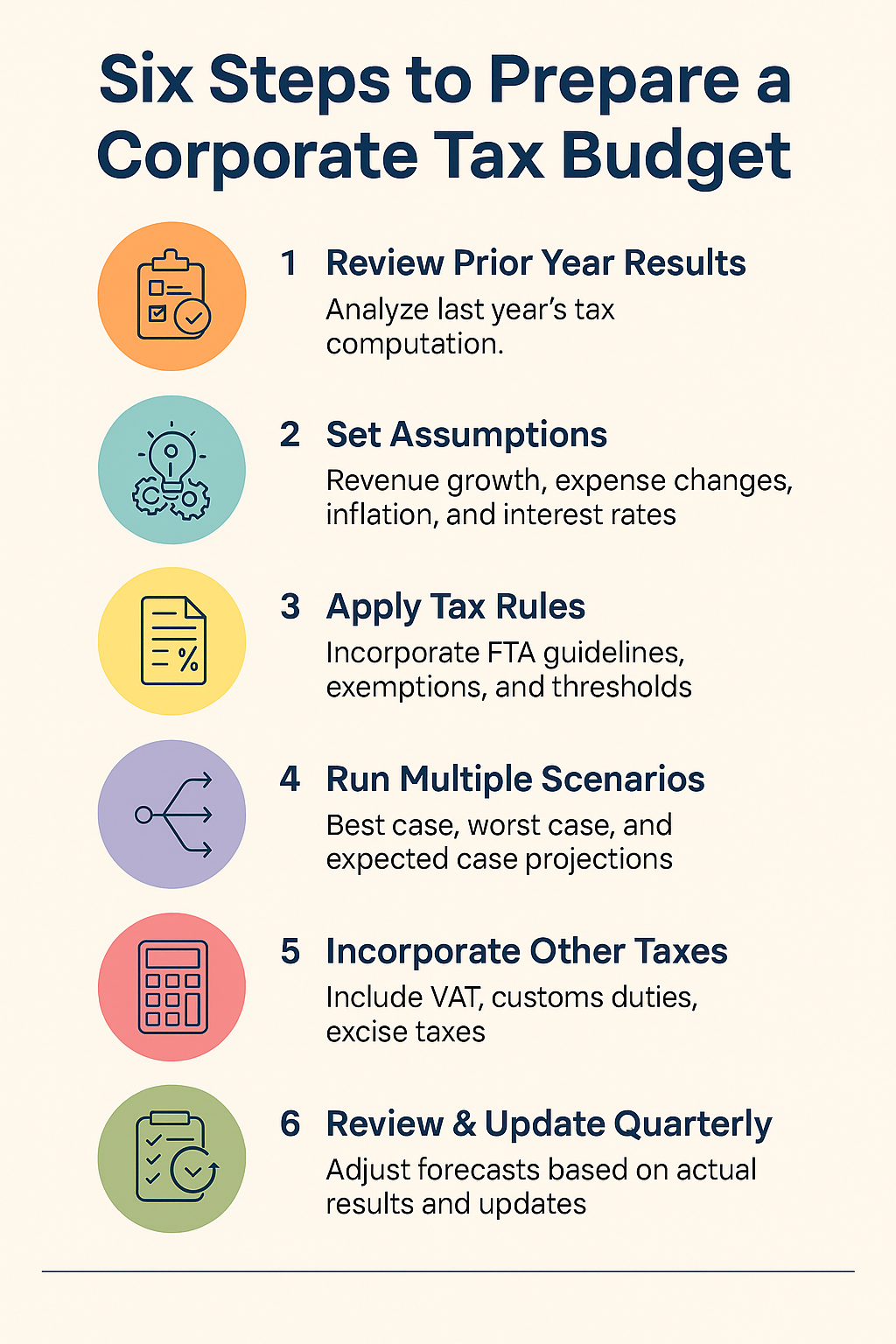

Steps in Preparing a Tax Budget

1. Review Prior Year Results – Analyze last year’s tax computation.

2. Set Assumptions – Revenue growth, expense changes, inflation, and interest rates.

3. Apply UAE Corporate Tax Rules – Incorporate FTA guidelines, exemptions, and thresholds.

4. Run Multiple Scenarios – Best case, worst case, and expected case projections.

5. Incorporate VAT & Other Taxes – Include VAT refunds/payments, customs duties, excise taxes.

6. Integrate with Overall Budget – Align tax estimates with business cash flow and investment plans.

7. Review & Update Quarterly – Adjust forecasts based on actual results and regulatory updates.

________________________________________

Best Practices for Accurate Forecasting

• Use Technology – ERP and forecasting software (like Finabooks ERP) for automated calculations.

• Involve Tax Experts – Work with auditors and tax consultants to validate assumptions.

• Stay Updated – Monitor FTA updates, Cabinet Decisions, and OECD rules.

• Stress-Test Scenarios – Prepare for changes in profitability, restructuring, or cross-border deals.

• Maintain Documentation – Ensure tax positions are backed by clear records to defend against audits.

________________________________________

Challenges in UAE Tax Forecasting

• Evolving Regulations – The UAE Corporate Tax law is new and subject to updates.

• Complex Group Structures – Multi-entity and cross-border operations increase forecasting difficulty.

• Transfer Pricing Compliance – Requires detailed documentation and arm’s length pricing.

• Economic Substance – Ensuring ESR compliance impacts tax status and incentives.

________________________________________

Conclusion

Corporate tax forecasting and budgeting are no longer optional—they are strategic necessities. By forecasting tax liabilities, businesses can avoid surprises, optimize cash flow, and take advantage of available tax reliefs.

In the UAE, where corporate tax is still in its early phase, companies that implement strong forecasting and budgeting frameworks today will gain a competitive advantage tomorrow.

________________________________________

📌 Sheikh Anwar Accounting & Auditing LLC

Approved Auditor – UAE Ministry of Economy (Entry No. 5817)

📧 info@sa-auditors.com

🌐 www.sa-auditors.com