Corporate Tax for Professional Services Firms

Introduction

With the implementation of the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) from 1 June 2023, professional services firms—such as law firms, audit firms, management consultancies, engineering firms, architects, designers, trainers, and even freelancers—must now ensure full compliance with the new corporate tax regime.

It outlines the tax implications, registration criteria, calculation methods, and best practices for professional services providers under UAE Corporate Tax.

________________________________________

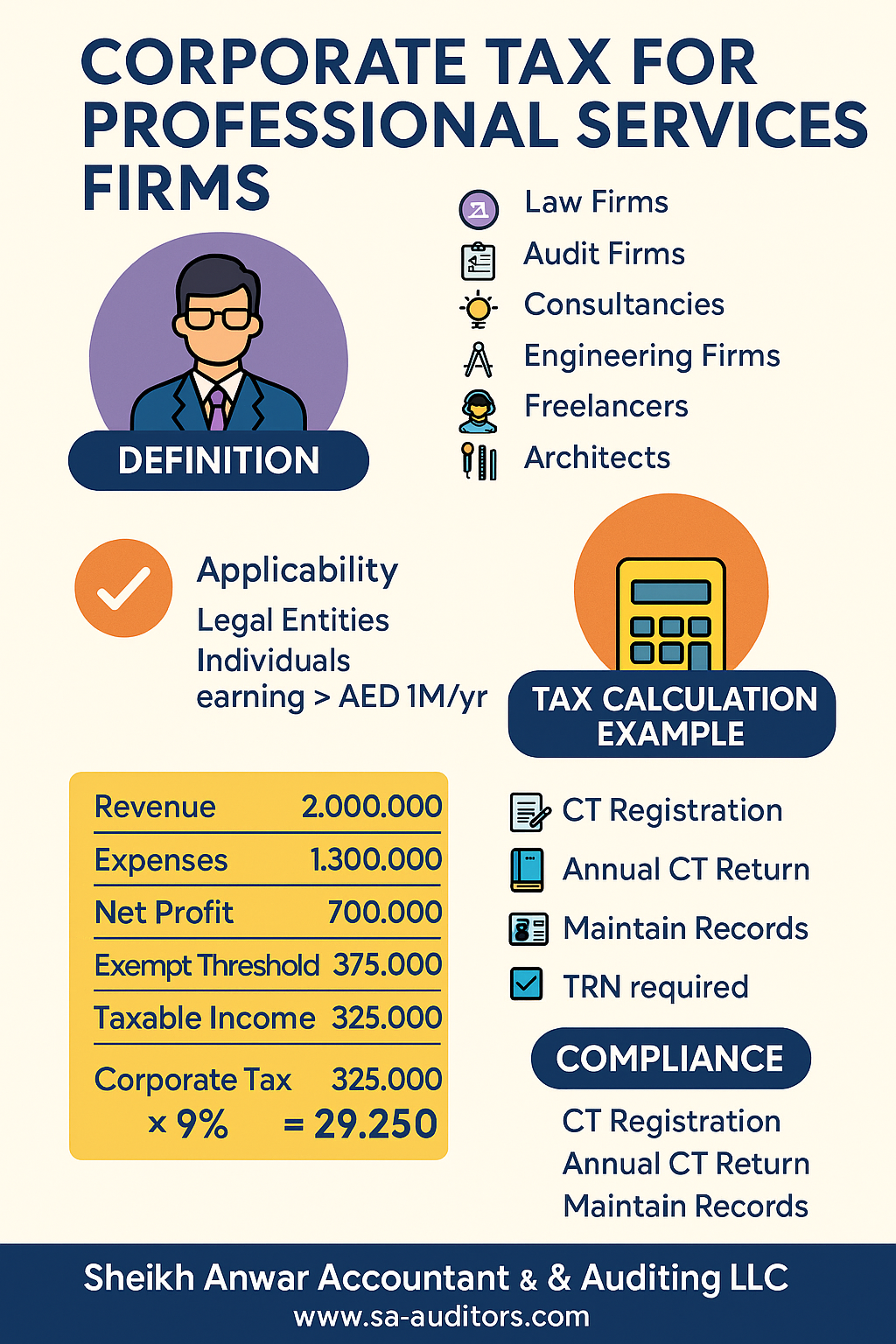

🧾 Who Is a “Professional Services Provider”?

A professional services provider includes any business or individual that offers specialized, knowledge-based, or skill-based services such as:

• Legal advisory and law firms

• Audit and accounting firms

• Tax and consulting agencies

• Engineering and architectural firms

• IT service providers and software consultants

• Medical, training, or HR consulting companies

• Freelancers and sole practitioners

These may operate as mainland companies, free zone entities, or even as individuals without a formal license.

________________________________________

✅ Applicability of Corporate Tax

Professional services firms are subject to UAE Corporate Tax if:

• They are a legal entity (LLC, branch, FZCO, etc.) earning taxable income

• They are natural persons (freelancers, consultants) earning over AED 1 million annually

📌 Corporate Tax applies at a standard rate of 9% on taxable profits exceeding AED 375,000.

________________________________________

🔍 Legal Reference

• Corporate Tax Law: Federal Decree-Law No. 47 of 2022

• Ministerial Decision No. 73 of 2023 – Business or Business Activity of a Natural Person

• Cabinet Decision No. 49 of 2023 – Thresholds for natural persons

________________________________________

💼 Corporate Tax Registration

All firms and qualifying individuals must:

• Register with the Federal Tax Authority (FTA) via EmaraTax portal

• Obtain a Tax Registration Number (TRN)

• File annual Corporate Tax returns

• Maintain accounting and business records for at least 7 years

________________________________________

🧮 Tax Calculation Example

Description Amount (AED)

Revenue 2,000,000

Expenses (salaries, rent, tools) 1,300,000

Net Profit 700,000

Exempt Threshold 375,000

Taxable Income 325,000

Corporate Tax @9% AED 29,250

Businesses may also deduct non-recoverable VAT, bad debts, depreciation, and other allowable costs under the law.

________________________________________

🧑💼 Individuals Providing Professional Services

If you are a freelancer, trainer, consultant, or IT expert operating without a company setup, and your annual revenue exceeds AED 1 million, you must:

• Register for Corporate Tax

• File returns and pay 9% on profits over AED 375,000

• Maintain basic accounting records

You are not required to form a company, but you must register as a taxable natural person if thresholds are crossed.

________________________________________

🏢 Free Zone Professional Firms

Free Zone professional services firms can benefit from the 0% Corporate Tax rate only if they meet the conditions of a Qualifying Free Zone Person (QFZP):

• Derive Qualifying Income from other Free Zone Persons or foreign clients

• Maintain adequate economic substance in the Free Zone

• Have audited financial statements

• Avoid earning Non-Qualifying Income (like mainland business income)

Failure to meet conditions will result in losing 0% rate and being taxed at 9%.

________________________________________

📋 Key Compliance Requirements

Requirement Applicable to

CT Registration All professional firms and individuals earning > AED 1M/year

Audited Financial Statements Required for Qualifying Free Zone firms

Record Keeping (7 years) All taxable persons

Transfer Pricing Documentation (if applicable) Firms with related-party transactions

CT Return Filing (Annually) Mandatory for all taxable persons

________________________________________

⚠️ Common Mistakes to Avoid

❌ Assuming CT doesn’t apply to individuals

❌ Mixing personal and business income in records

❌ Claiming non-deductible personal expenses

❌ Ignoring Free Zone qualification conditions

❌ Delaying CT registration beyond FTA deadlines

________________________________________

🧠 Example Scenarios

📌 Scenario 1: Management Consultant (Individual)

• Earns AED 1.5M from freelance consulting

• No company setup

✅ Must register for CT and pay 9% on profit above AED 375k

________________________________________

📌 Scenario 2: Audit Firm (Mainland)

• Operates as LLC

• Earns AED 3M per year

✅ Must register, maintain books, file returns, and pay CT at 9%

________________________________________

📌 Scenario 3: Software Consultant (Free Zone)

• Earns 70% from foreign clients

• 30% from UAE mainland

❌ Loses QFZP status → taxed at 9% on all income

________________________________________

📌 Best Practices

✅ Register early and comply with deadlines

✅ Maintain detailed revenue and cost tracking

✅ Separate personal and business bank accounts

✅ Seek professional advice on QFZP status and tax planning

✅ Ensure accurate accounting and timely filings

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

We support professional services firms with:

✅ Corporate Tax registration and return filing

✅ Revenue structuring to optimize tax liability

✅ Free Zone qualification assessment

✅ Bookkeeping and financial reporting

✅ Natural person CT advisory and compliance

________________________________________

📞 Contact Us

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX