Corporate Tax for IT & Software Companies

Introduction

The UAE has become a leading hub for technology, IT, and software development companies, attracting startups, multinational corporations, and freelancers in the digital economy. With the introduction of UAE Corporate Tax (Federal Decree-Law No. 47 of 2022), IT and software businesses must now carefully assess how taxation applies to their services, licensing arrangements, and cross-border digital operations.

Given the sector’s reliance on intellectual property (IP), software licensing, and cross-border revenue streams, tax structuring and compliance are especially important for IT and software firms.

________________________________________

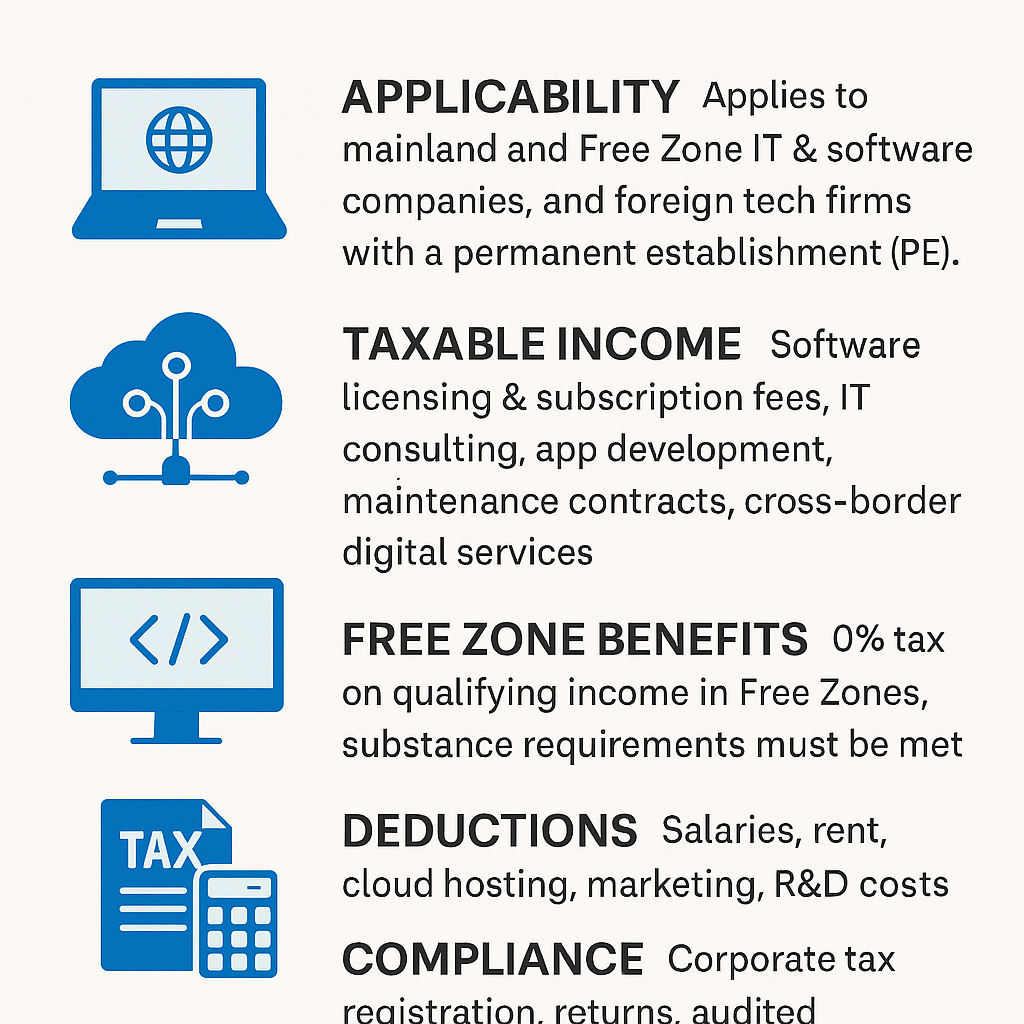

1. Applicability of Corporate Tax to IT & Software Companies

• Mainland IT & Software Companies: Fully subject to Corporate Tax at standard rates.

• Free Zone Entities: May enjoy 0% Corporate Tax on qualifying income (e.g., cross-border software services, Free Zone-to-Free Zone projects) if they meet economic substance requirements.

• Foreign Tech Companies: Liable to UAE Corporate Tax if they maintain a permanent establishment (PE) in the UAE, such as local offices, servers, or agents.

________________________________________

2. Corporate Tax Rates for IT & Software Firms

• 0% on taxable income up to AED 375,000.

• 9% on taxable income above AED 375,000.

• Free Zone Firms: 0% on qualifying income, 9% on mainland client income unless exceptions apply.

________________________________________

3. Taxable Income for IT & Software Companies

Taxable income includes multiple streams relevant to digital businesses:

• Software Licensing & Subscription Fees (SaaS, cloud-based services).

• IT Consulting & Implementation Services.

• Mobile & Web App Development Fees.

• Maintenance & Support Contracts.

• Advertising Revenue (for platforms).

• Cross-Border Digital Services provided to clients outside UAE.

________________________________________

4. Deductible vs. Non-Deductible Expenses

IT and software firms incur significant technology-related costs.

• Deductible Expenses:

o Salaries for developers, engineers, and IT staff.

o Rent, utilities, and IT infrastructure costs.

o Cloud hosting, data storage, and cybersecurity expenses.

o Marketing, advertising, and digital campaigns.

o Depreciation of equipment and intangible assets.

o R&D expenses for software innovation.

• Non-Deductible Expenses:

o Fines and penalties.

o Personal expenses.

o Non-business related travel and entertainment.

________________________________________

5. Free Zone Benefits for IT & Software Companies

Free Zones such as Dubai Internet City, Dubai Silicon Oasis, ADGM, and DIFC cater specifically to technology firms.

• Advantages:

o 0% Corporate Tax on qualifying income.

o Advanced digital infrastructure and co-working hubs.

o Customs and import duty exemptions.

• Requirements:

o Must demonstrate economic substance (office, staff, management in UAE).

o Mainland service income generally taxed at 9%.

________________________________________

6. Transfer Pricing and IP Considerations

IT & software firms often operate in international structures where intellectual property (IP) plays a major role.

• Transfer Pricing (TP) rules apply to:

o Licensing IP between group companies.

o Shared services (e.g., global R&D costs).

o Intercompany royalties, cloud hosting, or IT support services.

• Firms must comply with the arm’s length principle and maintain TP documentation (Local File, Master File, Benchmarking) if thresholds are met.

________________________________________

7. Permanent Establishment (PE) Risks for Foreign Tech Firms

Foreign IT firms serving UAE clients may create a PE if they:

• Have servers or data centers in the UAE.

• Employ staff or dependent agents working locally.

• Operate significant digital presence targeting UAE users.

This can make foreign software companies liable to UAE Corporate Tax.

________________________________________

8. Compliance Requirements for IT & Software Companies

• Corporate Tax Registration with the Federal Tax Authority (FTA).

• Annual Corporate Tax Return filed within 9 months of year-end.

• Audited Financial Statements (required for most Free Zone and medium/large companies).

• Record-Keeping: Invoices, contracts, licensing agreements, and expense records must be retained for 7 years.

________________________________________

9. Strategic Tax Planning for IT & Software Firms

• Leverage Free Zone Benefits for cross-border software exports.

• Optimize IP Structures to manage royalties and licensing income efficiently.

• Expense Management: Ensure all deductible R&D and IT costs are claimed.

• Loss Relief: Carry forward tax losses to offset against future profits.

• ERP & Compliance Tools: Automate VAT + Corporate Tax compliance using integrated accounting software.

________________________________________

Conclusion

The introduction of Corporate Tax reshapes the financial landscape for IT & software companies in the UAE. With multiple revenue streams, IP arrangements, and cross-border services, the sector must adopt robust compliance practices, Transfer Pricing discipline, and smart Free Zone structuring.

Proper planning today ensures businesses remain compliant while continuing to innovate and expand in the UAE’s dynamic technology ecosystem.

________________________________________

✍️ By Sheikh Anwar Accounting and Auditing LLC (SA-Auditors)

📍 Dubai, United Arab Emirates

🌐 www.sa-auditors.com | ✉️ info@sa-auditors.com