Corporate Tax for Holding Companies

Introduction

The UAE is a popular jurisdiction for holding companies, used to manage investments, own shares in subsidiaries, and structure international business groups. With the implementation of Corporate Tax (CT) via Federal Decree-Law No. 47 of 2022, it’s essential for holding entities to understand their obligations, exemptions, and reporting requirements under UAE law.

It explains how Corporate Tax applies to holding companies, whether based in the mainland, free zones, or offshore jurisdictions.

________________________________________

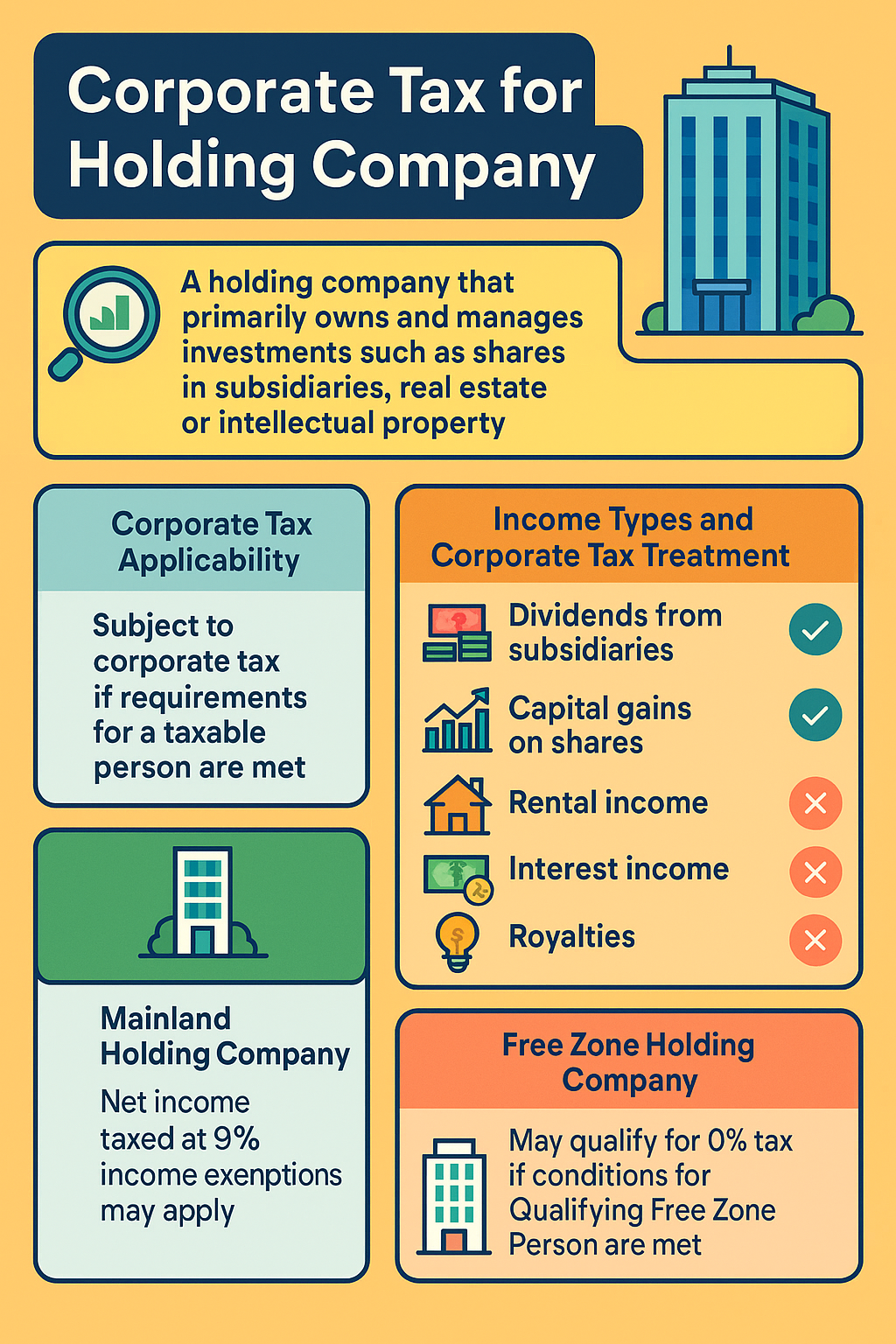

🧾 What is a Holding Company?

A holding company is an entity established primarily to own and manage investments such as:

• Shares in other companies

• Intellectual property (IP)

• Real estate assets

• Subsidiary entities

It typically does not engage in operational or trading activities itself.

________________________________________

✅ Corporate Tax Applicability to Holding Companies

A UAE holding company is subject to Corporate Tax if it meets the definition of a Taxable Person under the law. However, the income it earns may be exempt, depending on the type of income and whether certain conditions are met.

________________________________________

🧾 Key Income Sources for Holding Companies and CT Treatment

Income Type CT Treatment

Dividends from UAE resident companies ✅ Exempt under Participation Exemption rules

Dividends from foreign subsidiaries ✅ Exempt if participation conditions are met

Capital gains on disposal of shares ✅ Exempt if participation exemption applies

Rental income from real estate ✅ Taxable, unless exempt for individuals under CT thresholds

Interest income ✅ Taxable

Royalties or license fees ✅ Taxable, especially for IP holding companies

________________________________________

🎯 Participation Exemption – Article 23 of CT Law

The Participation Exemption allows holding companies to exclude income such as dividends and capital gains from their CT base, provided that:

✅ The holding company owns at least 5% of the shares in the subsidiary

✅ The subsidiary is subject to at least 9% tax (or comparable rate) in its home country

✅ The shares are held for at least 12 months, or there’s an intention to do so

✅ The subsidiary is not a passive or portfolio investment

________________________________________

🏢 Mainland vs. Free Zone Holding Companies

1. Mainland Holding Companies

• Must register for Corporate Tax

• Subject to 9% CT on non-exempt income

• Can claim Participation Exemption for dividend and capital gains income

• Must maintain accounting records and file returns

________________________________________

2. Free Zone Holding Companies

• May qualify for 0% Corporate Tax if they meet Qualifying Free Zone Person (QFZP) criteria:

o Earn Qualifying Income (e.g., dividends from foreign subsidiaries)

o Maintain adequate substance in the Free Zone

o Have audited financial statements

❗ If the entity earns income from mainland UAE, it may lose QFZP status and be taxed at 9%.

________________________________________

3. Offshore Holding Companies (RAK ICC, JAFZA Offshore, etc.)

• Not considered tax residents unless they have real presence in the UAE

• If they have UAE nexus (like real estate or PE), they may become taxable

• Must assess if they are resident persons under UAE CT law

________________________________________

🧠 Example Scenarios

📌 Scenario 1: Mainland Holding Company

• Owns 100% of a UAE subsidiary and receives AED 2M in annual dividends

✅ Exempt under participation exemption

________________________________________

📌 Scenario 2: Free Zone Holding Company (QFZP)

• Owns foreign subsidiaries, earns dividends and capital gains

• Maintains proper accounting, audited financials

✅ Eligible for 0% Corporate Tax

________________________________________

📌 Scenario 3: Holding Co. with Mainland Rent Income

• Owns shares and also leases a building in Dubai

❌ Rental income is taxable → entity loses QFZP status → entire income taxed at 9%

________________________________________

📋 Corporate Tax Compliance for Holding Companies

Requirement Details

CT Registration Mandatory if holding company earns income

Accounting Records Must be maintained for 7 years

Audited Financials Mandatory for QFZP status

Participation Exemption Documentation Ownership %, holding period, subsidiary tax proof

Transfer Pricing Compliance Required if dealing with related parties

________________________________________

❌ Common Pitfalls

• ❌ Assuming dividend income is always exempt

• ❌ Not maintaining proof of participation conditions

• ❌ Ignoring 9% tax exposure on interest and rental income

• ❌ Loss of QFZP status due to non-qualifying income

• ❌ Misclassifying holding companies with operational activity

________________________________________

✅ Best Practices

• Maintain detailed shareholding records

• Verify foreign subsidiary tax rates for exemption qualification

• Keep audited financial statements

• Avoid earning mainland UAE income through Free Zone entities

• Conduct substance checks for Free Zone status

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

We assist holding companies with:

✅ Corporate Tax registration and exemption claims

✅ Participation exemption qualification assessment

✅ Free Zone vs. mainland structuring guidance

✅ Preparation of financials and CT returns

✅ Nexus and tax residency advisory

________________________________________

📞 Contact Us

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX