Corporate Tax for Gold and Jewelry Traders

Introduction

The UAE’s gold and jewelry sector is one of the most significant contributors to its economy, serving as a global hub for bullion trading, jewelry manufacturing, and retail. With the introduction of UAE Corporate Tax (Federal Decree-Law No. 47 of 2022), gold and jewelry traders must now integrate tax planning and compliance into their business strategies.

While the sector already complies with Value Added Tax (VAT) and strict Anti-Money Laundering (AML) regulations, Corporate Tax introduces an additional layer of compliance that requires careful attention to accounting, reporting, and structuring.

________________________________________

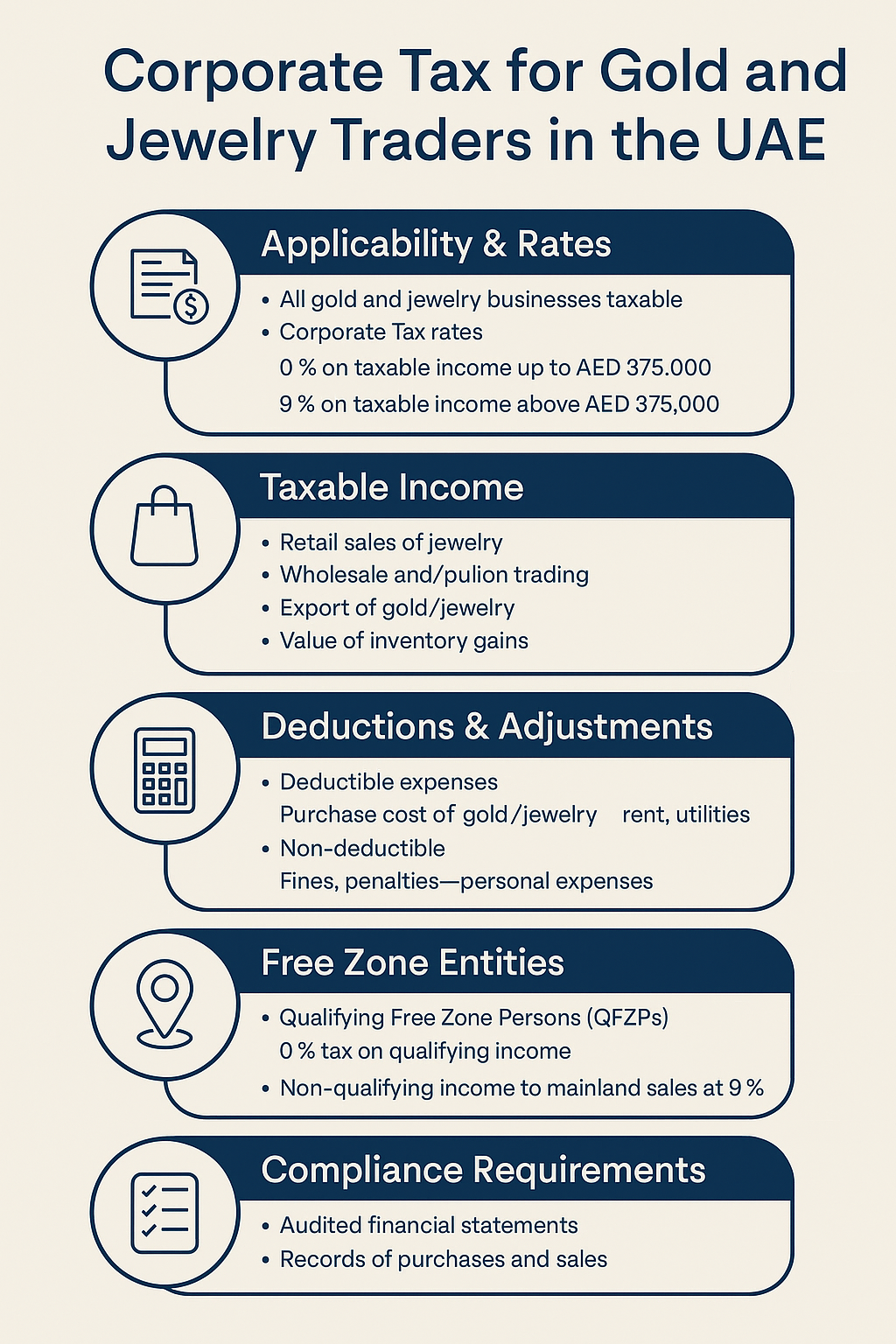

1. Applicability of Corporate Tax to Gold and Jewelry Traders

• Taxable Persons: All gold and jewelry businesses incorporated in the UAE (mainland or free zones) are subject to Corporate Tax.

• Corporate Tax Rate:

o 0% on taxable income up to AED 375,000.

o 9% on taxable income above AED 375,000.

• Exemptions: Entities directly engaged in extractive industries or natural resource exploitation may be exempt, but typical gold trading and jewelry businesses do not qualify.

________________________________________

2. Taxable Income for Gold and Jewelry Businesses

Gold and jewelry traders generate multiple revenue streams, all of which may be taxable unless specifically exempt:

• Retail Sales of Jewelry – taxable as ordinary income.

• Wholesale and Bullion Trading – subject to Corporate Tax on net profits.

• Export of Gold/Jewelry – zero-rated for VAT but included in corporate tax profits.

• Value of Inventory Gains – adjustments for unrealized gains or revaluation may impact taxable income.

________________________________________

3. Key Deductions and Adjustments

• Deductible Expenses:

o Purchase cost of gold/jewelry (cost of goods sold).

o Staff salaries, rent, and utilities.

o Depreciation on machinery, safes, and equipment.

o Security and insurance costs.

• Non-Deductible Expenses:

o Fines, penalties, personal expenses, and excessive entertainment costs.

• Interest Deduction: Limited to 30% of EBITDA if debt-financed.

Accurate segregation of deductible vs non-deductible expenses in financial statements is critical for jewelers to minimize tax liabilities.

________________________________________

4. Free Zone Entities and Qualifying Income

Many jewelers operate through Free Zones such as DMCC, JAFZA, and Sharjah Gold Refinery Zones.

• Qualifying Free Zone Persons (QFZP) may enjoy 0% Corporate Tax on qualifying income.

• Qualifying Income for Gold/Jewelry Traders:

o Trading with other Free Zone entities.

o Export transactions outside the UAE.

• Non-Qualifying Income: Sales to mainland customers (unless structured via designated rules) will likely attract 9% Corporate Tax.

________________________________________

5. Interaction with VAT and RCM (Reverse Charge Mechanism)

• The gold and diamond sector already operates under Cabinet Decision No. 25 of 2018, applying the Reverse Charge Mechanism (RCM) on wholesale supplies between registered businesses.

• For Corporate Tax:

o Profits from RCM-based supplies are taxable.

o VAT recoverability continues separately from Corporate Tax.

Jewelers must maintain clear reconciliation between VAT returns and Corporate Tax filings.

________________________________________

6. Transfer Pricing and Related-Party Transactions

Gold and jewelry traders often operate through family-owned groups or related-party businesses across the UAE and abroad.

• Transfer Pricing (TP) rules require related-party transactions (e.g., intra-group gold sales, loans, or management fees) to follow the arm’s length principle.

• Documentation: Depending on turnover thresholds, jewelers may need to maintain Local File, Master File, and Benchmarking studies.

________________________________________

7. Inventory Valuation and Its Tax Impact

• Gold and jewelry businesses deal with fluctuating commodity prices.

• Inventory must be valued in accordance with IFRS standards.

• Revaluation gains/losses may need adjustments when computing taxable income.

• Proper treatment of wastage, purity adjustments (21k, 22k, 24k), and by-products is essential.

________________________________________

8. Compliance and Record-Keeping Requirements

Gold and jewelry traders must maintain:

• Audited financial statements prepared under IFRS.

• Complete books and records of purchases, sales, and customer details.

• AML-related documentation (e.g., CDD, KYC records) which may overlap with tax audit requirements.

• Minimum retention period of 7 years for tax purposes.

________________________________________

9. Strategic Tax Planning for Jewelers

• Free Zone Structuring: Maximize 0% Corporate Tax on qualifying exports.

• Inventory Planning: Efficient stock management to reduce taxable profits.

• Loss Relief: Carry forward losses to offset future profits (subject to conditions).

• Group Relief: Utilize group loss transfer and tax grouping options if multiple jewelry companies exist under the same ownership.

• ERP Systems: Adopt accounting systems that integrate VAT + Corporate Tax + AML compliance.

________________________________________

Conclusion

The introduction of Corporate Tax marks a significant change for the UAE’s gold and jewelry industry. While the regime is designed to be competitive and business-friendly, compliance will require robust financial reporting, inventory valuation, and tax planning strategies.

By proactively aligning with the new Corporate Tax framework — alongside VAT and AML obligations — gold and jewelry traders can ensure both compliance and profitability in one of the UAE’s most important sectors.

________________________________________

✍️ By Sheikh Anwar Accounting and Auditing LLC (SA-Auditors)

📍 Dubai, United Arab Emirates

🌐 www.sa-auditors.com | ✉️ info@sa-auditors.com