Corporate Tax for Free Zone Companies

Introduction

With the implementation of Corporate Tax (CT) in the UAE from 1 June 2023, Free Zone companies are no longer entirely exempt from taxation. However, the UAE Corporate Tax Law provides certain preferential treatments to Free Zone entities that qualify as Qualifying Free Zone Persons (QFZP).

Here, we explore how Corporate Tax applies to Free Zone businesses, the criteria to qualify for 0% tax, compliance requirements, and what Free Zone entities need to do to remain compliant.

________________________________________

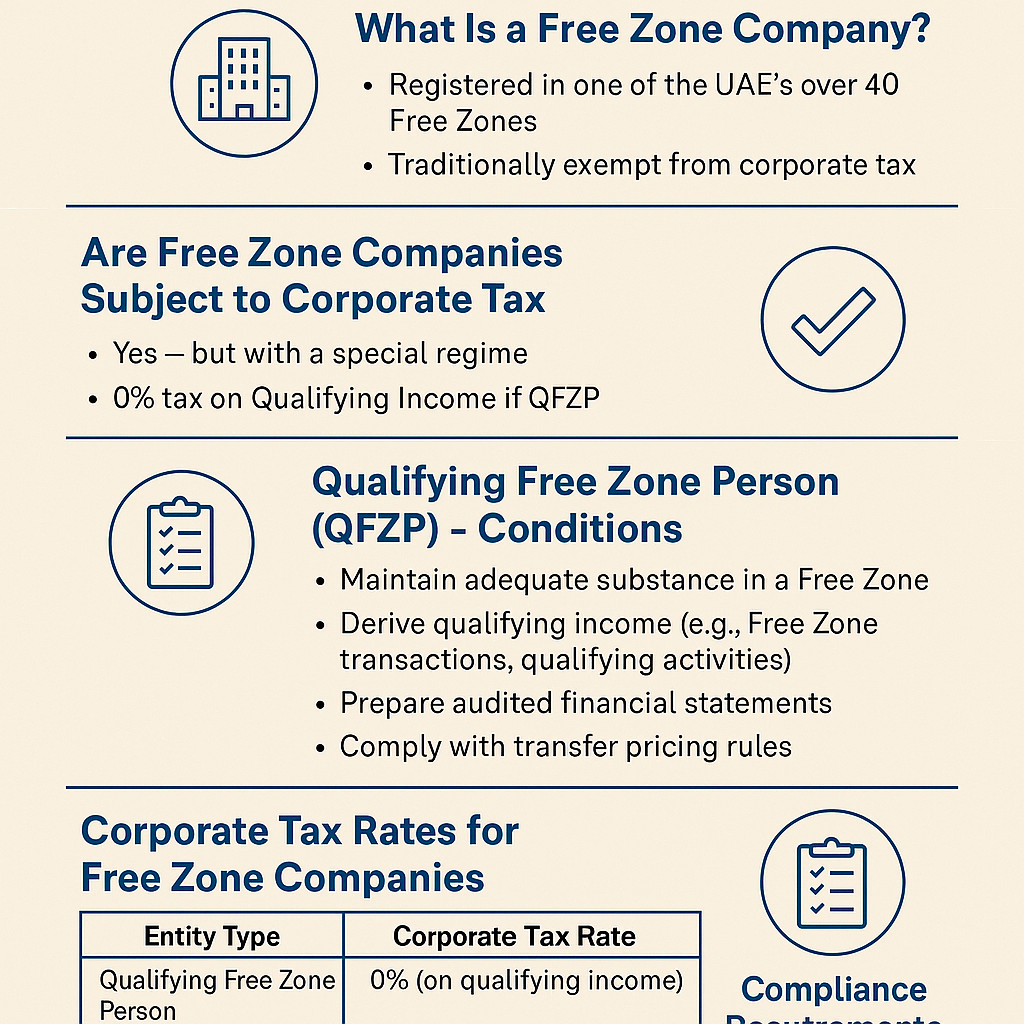

🏢 What Is a Free Zone Company?

A Free Zone company is registered in one of the UAE’s more than 40 Free Zones. These entities were traditionally exempt from corporate tax, customs duties, and foreign ownership restrictions. However, under the new CT regime, all businesses are subject to corporate tax, unless specifically exempted or eligible for preferential treatment.

________________________________________

⚖️ Legal Framework

Corporate Tax for Free Zones is governed by:

• Federal Decree-Law No. 47 of 2022

• Ministerial Decision No. 139 of 2023 (Conditions for QFZP)

• Cabinet Decision No. 55 of 2023 (Regulation on Free Zone Persons)

• FTA Public Clarification CT-FZP1

________________________________________

💼 Are Free Zone Companies Subject to Corporate Tax?

✅ YES – but with a special regime:

• Free Zone companies are taxable persons under the law.

• However, they may be eligible for 0% tax on Qualifying Income if they meet the QFZP criteria.

If a Free Zone company does not meet the conditions, they will be taxed at 9% on their full taxable income.

________________________________________

✅ Qualifying Free Zone Person (QFZP) – Conditions

To be considered a QFZP and benefit from 0% Corporate Tax, the Free Zone entity must:

1. Maintain adequate substance in the Free Zone.

2. Derive qualifying income such as:

o Income from transactions with other Free Zone entities.

o Income from qualifying activities with non-Free Zone persons (as listed in the law).

3. Not have elected to be taxed under the standard regime.

4. Prepare audited financial statements.

5. Comply with transfer pricing rules.

________________________________________

💼 What Is Qualifying Income?

Qualifying income includes:

• Income from transactions with other Free Zone Persons.

• Income from transactions with non-Free Zone persons related to Qualifying Activities, including:

o Holding of shares and securities

o Reinsurance services

o Fund management

o Headquarter services to group companies

o Warehousing and logistics services

o Manufacturing and processing of goods

o Distribution of goods in/outside the UAE

• Income derived from owning or exploiting intellectual property is excluded from qualifying income and taxed at 9%.

________________________________________

❌ What Disqualifies a Free Zone Company?

A Free Zone company loses QFZP status if:

• It derives non-qualifying income that exceeds de minimis threshold (5% or AED 5 million of total revenue).

• It fails to maintain proper substance.

• It elects to be subject to standard Corporate Tax.

• It fails to meet the accounting or filing requirements.

Once disqualified, it becomes subject to 9% Corporate Tax on all income and loses QFZP status for five years.

________________________________________

📝 Corporate Tax Rates for Free Zone Companies

Entity Type Corporate Tax Rate

Qualifying Free Zone Person 0% (on qualifying income)

Non-Qualifying Free Zone Person 9% (on full taxable income)

Income from excluded activities or IP 9%

________________________________________

🗂️ Compliance Requirements

✅ For All Free Zone Companies:

• Corporate Tax Registration with the FTA via EmaraTax

• Maintain audited financial statements

• File annual Corporate Tax return within 9 months of end of financial year

• Prepare transfer pricing documentation, if applicable

________________________________________

📅 Corporate Tax Return Deadlines

Free Zone entities must file their return:

• Within 9 months from the end of their financial year

• E.g., If the financial year ends 31 December 2024, return due by 30 September 2025

________________________________________

🚫 Penalties for Non-Compliance

• AED 10,000 for failure to register

• Penalties for late filing, inaccurate information, or failure to maintain records

________________________________________

🧠 Why Choose Sheikh Anwar Accounting & Auditing LLC?

At Sheikh Anwar Accounting & Auditing LLC, we specialize in helping Free Zone businesses:

• Assess whether they qualify as QFZPs

• Structure operations to retain 0% tax benefits

• Prepare and audit financial statements

• Register and file Corporate Tax returns

• Comply with transfer pricing and substance requirements

📞 Contact us today at

www.sa-auditors.com

________________________________________

🧾 Conclusion

Corporate Tax is now a reality for Free Zone businesses in the UAE. While the 0% rate remains available, it comes with strict conditions and compliance requirements. Proper planning and documentation are key to staying compliant and tax efficient.

Let Sheikh Anwar Accounting & Auditing LLC be your trusted partner in navigating the complexities of the UAE Corporate Tax landscape.