Corporate Tax for E-Commerce Businesses

Introduction

The UAE has emerged as one of the fastest-growing e-commerce markets in the Middle East, with rising demand for online retail, digital marketplaces, and cross-border trade. With the introduction of UAE Corporate Tax (Federal Decree-Law No. 47 of 2022), e-commerce businesses — from online retailers to large global platforms — must understand their tax obligations, compliance requirements, and planning opportunities.

Unlike VAT, which is transaction-based, Corporate Tax is profit-based, making accurate financial reporting and strategic planning essential for digital businesses.

________________________________________

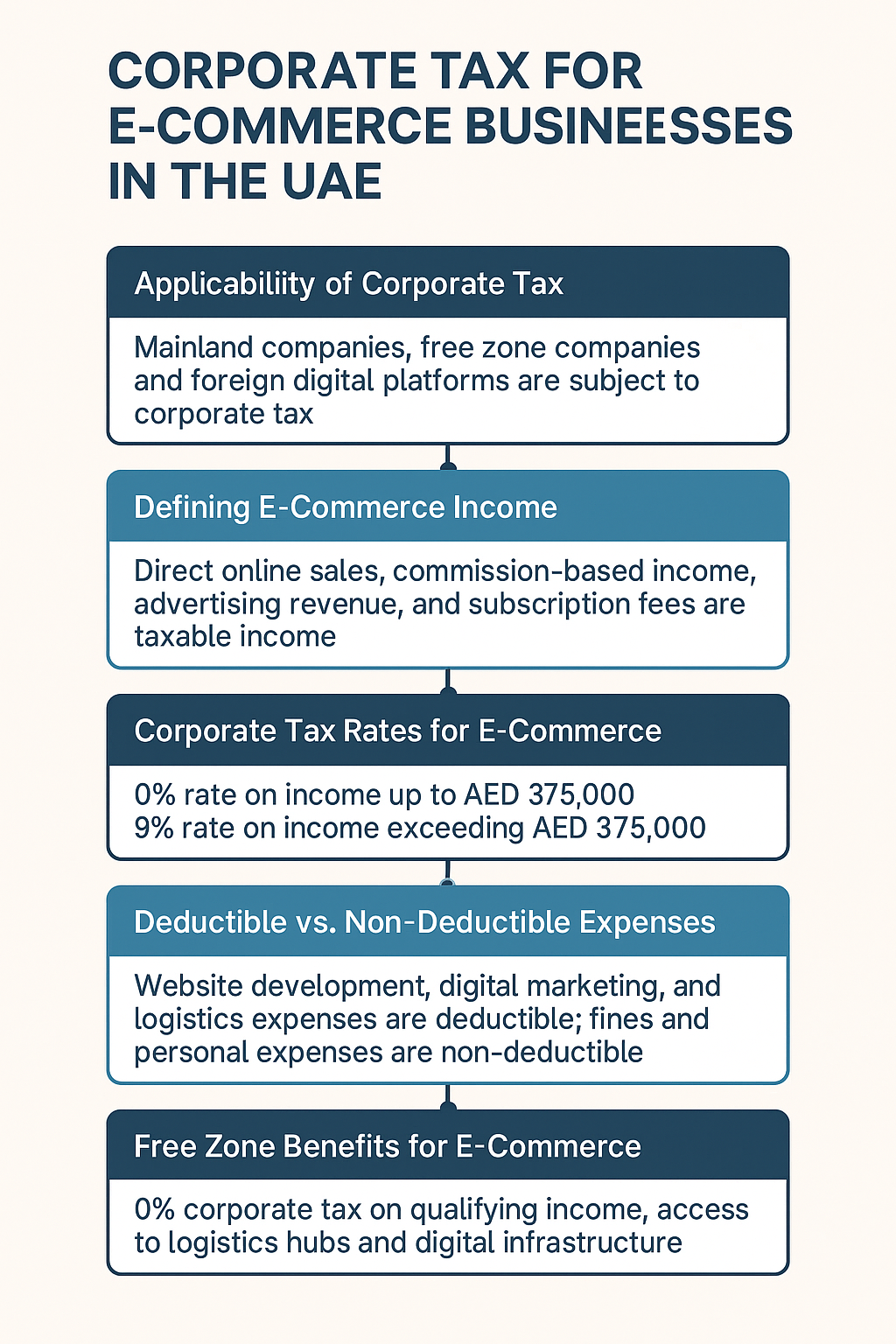

1. Applicability of Corporate Tax to E-Commerce

Corporate Tax applies to all businesses engaged in e-commerce activities, whether operating through:

• Mainland Companies – subject to 9% Corporate Tax on taxable income above AED 375,000.

• Free Zone Companies – may benefit from 0% Corporate Tax on qualifying income if substance requirements are met.

• Foreign Digital Platforms – subject to UAE Corporate Tax if they have a permanent establishment or nexus in the UAE (e.g., local servers, warehouses, or significant digital presence).

________________________________________

2. Defining E-Commerce Income

E-commerce businesses typically generate multiple types of income streams, including:

• Direct Online Sales of goods or services.

• Commission-Based Income from operating marketplaces.

• Advertising Revenue from online platforms.

• Subscription Fees for digital services or memberships.

• Logistics & Fulfillment Income if bundled into the digital offering.

All such income is considered taxable unless specifically exempt.

________________________________________

3. Corporate Tax Rates for E-Commerce

• 0% rate on taxable income up to AED 375,000.

• 9% rate on taxable income exceeding AED 375,000.

• Free Zone E-Commerce Companies may enjoy 0% CT on qualifying income (cross-border sales, transactions with other Free Zone Persons), but mainland sales typically attract 9%.

________________________________________

4. Deductible vs. Non-Deductible Expenses

E-commerce businesses incur significant digital, logistical, and marketing expenses. Tax treatment is as follows:

• Deductible Expenses:

o Website development and hosting costs.

o Digital marketing, advertising, and SEO costs.

o Payment gateway and platform fees.

o Staff salaries, rent, and logistics expenses.

o Depreciation of IT infrastructure.

• Non-Deductible Expenses:

o Fines, penalties, and donations not meeting tax criteria.

o Personal expenses recorded in business accounts.

________________________________________

5. Free Zone Benefits for E-Commerce

Free Zones such as Dubai CommerCity, DIFC, ADGM, and DMCC attract e-commerce businesses by offering:

• 0% Corporate Tax on qualifying cross-border transactions.

• Access to logistics hubs and digital infrastructure.

• Exemption on customs duties for re-exports.

To maintain Qualifying Free Zone Person (QFZP) status:

• The business must have adequate economic substance in the UAE.

• Transactions with mainland customers are either excluded or subject to 9% CT.

________________________________________

6. Transfer Pricing and Digital Businesses

Many e-commerce businesses operate through group structures (parent companies abroad with UAE subsidiaries).

• Transfer Pricing (TP) rules apply to related-party transactions such as:

o Intercompany licensing of software.

o Shared IT and marketing costs.

o Royalty payments and IP usage fees.

• TP compliance requires Local File, Master File, and Benchmarking documentation.

________________________________________

7. Digital Presence and Permanent Establishment (PE) Risk

Foreign e-commerce companies may be taxed in the UAE if they have:

• Servers or Warehouses in the UAE.

• Significant Customer Base or Digital Nexus in the UAE.

• Dependent Agents operating in the UAE on their behalf.

This concept ensures that digital businesses without a physical store but with significant UAE activity are brought into the tax net.

________________________________________

8. Compliance and Record-Keeping Requirements

E-commerce businesses must maintain:

• Audited financial statements prepared under IFRS/IFRS for SMEs.

• Complete records of sales, commissions, and advertising income.

• Contracts with third-party logistics and payment providers.

• Documentation for all cross-border digital service transactions.

Records must be retained for 7 years for Corporate Tax audit purposes.

________________________________________

9. Strategic Tax Planning for E-Commerce

• Free Zone Structuring: Optimize use of Free Zones for cross-border sales.

• IP Holding Companies: Locate intellectual property in favorable jurisdictions to minimize royalty tax leakage.

• Cost Allocation: Correctly allocate global marketing and IT costs for TP compliance.

• Loss Relief: Utilize carried-forward losses to offset future taxable profits.

• ERP Integration: Implement accounting systems that seamlessly track both VAT and Corporate Tax.

________________________________________

Conclusion

The UAE’s Corporate Tax regime significantly impacts the e-commerce industry, requiring businesses to align financial reporting, digital operations, and cross-border structures with the new tax rules. While Free Zones offer attractive benefits, compliance with economic substance, transfer pricing, and record-keeping obligations is essential.

With proactive planning and robust compliance, e-commerce businesses can remain competitive while meeting their obligations under the UAE Corporate Tax framework.

________________________________________

✍️ By Sheikh Anwar Accounting and Auditing LLC (SA-Auditors)

📍 Dubai, United Arab Emirates

🌐 www.sa-auditors.com | ✉️ info@sa-auditors.com