Corporate Entertainment and Tax Deductions

Corporate entertainment is an essential part of modern business practices—used to build client relationships, reward employees, and promote brand value. However, with the advent of the UAE Corporate Tax regime under Federal Decree-Law No. 47 of 2022, businesses must understand how entertainment expenses are treated for tax deduction purposes.

Sheikh Anwar Accounting & Auditing LLC explains the rules, limits, and conditions surrounding entertainment expense deductions, as defined in UAE Corporate Tax law and related ministerial decisions.

________________________________________

📜 Legal Reference

The treatment of entertainment expenses is covered under:

• Article 32 of the UAE Corporate Tax Law

• Ministerial Decision No. 114 of 2023

These provisions clarify what qualifies as entertainment, how much can be deducted, and under what circumstances.

________________________________________

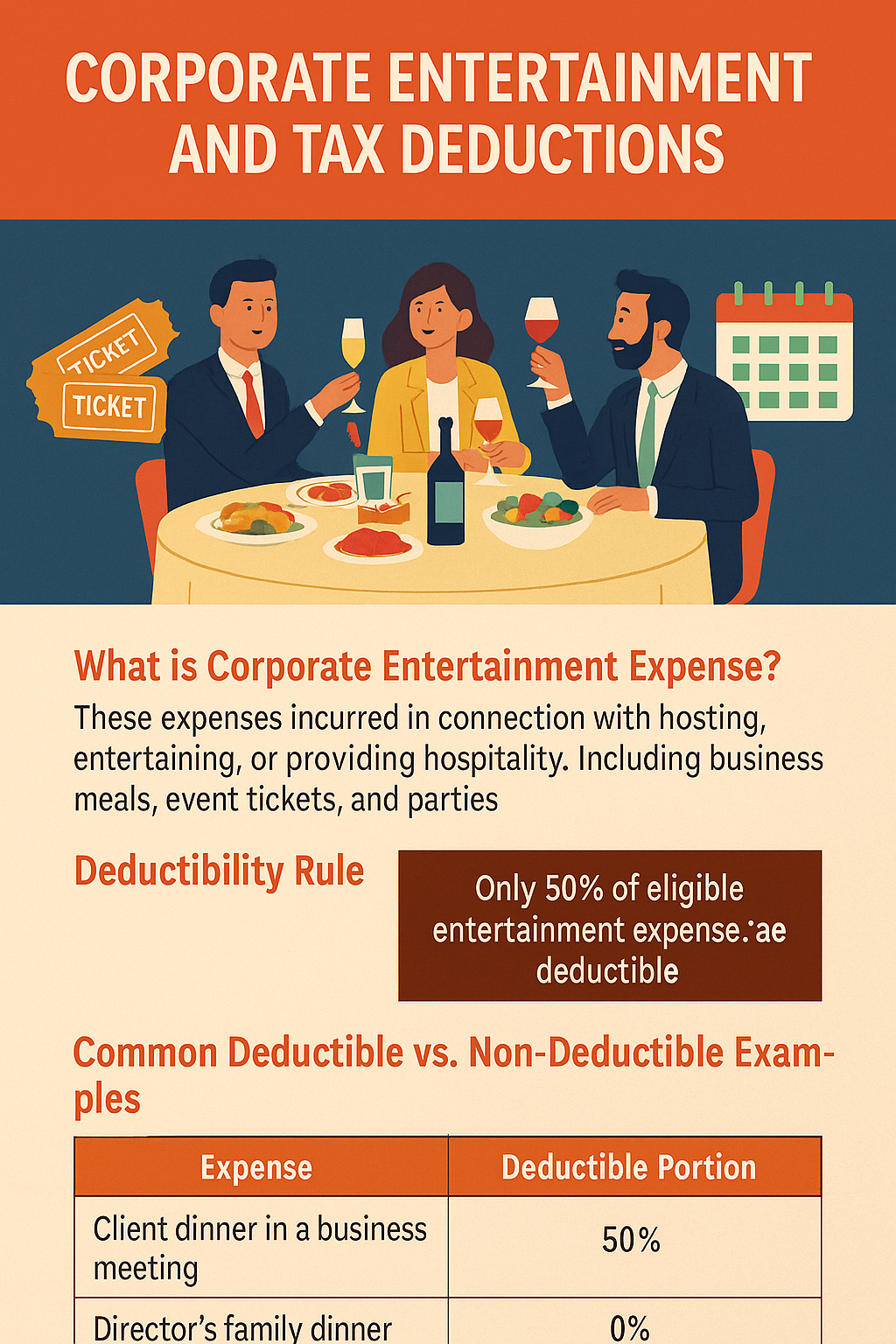

🍽️ What is Considered a Corporate Entertainment Expense?

Corporate entertainment expenses are those incurred in connection with hosting, entertaining, or providing hospitality to:

• Clients

• Customers

• Suppliers

• Business partners

• Employees (under certain events)

These typically include:

• Business meals and restaurant bills

• Hotel stays and travel for entertainment

• Event tickets (concerts, sports matches)

• Corporate parties and receptions

• Recreational activities (e.g., golf, yacht outings)

________________________________________

✅ Deductibility Rule

As per Article 32, only 50% of eligible entertainment expenses are allowed as a tax-deductible expense.

This means that if a company spends AED 100,000 on client entertainment, only AED 50,000 can be claimed as deductible when calculating taxable income.

📌 Key Point: The 50% rule applies only to legitimate business-related entertainment. Personal entertainment is entirely disallowed.

________________________________________

⚠️ Common Deductible vs. Non-Deductible Examples

Expense Deductible Portion Notes

Client dinner in a business meeting ✅ 50% Proper documentation required

Annual corporate event for staff ✅ 50% Valid if business-related

Director’s family dinner ❌ 0% Personal in nature

Tickets for client entertainment ✅ 50% Document reason and attendees

Holiday retreat without business agenda ❌ 0% Considered personal

________________________________________

🧾 Documentation Requirements

To support entertainment expense deductions, businesses should maintain:

• Invoices and receipts

• Purpose of the expense

• List of attendees and their relationship to the business

• Proof that the event was business-related

Lack of proper documentation may lead to complete disallowance during FTA audits.

________________________________________

🧮 Example Calculation

XYZ LLC incurs the following expenses in a tax year:

• Client dinner: AED 10,000

• Corporate event for employees: AED 15,000

• Director’s birthday party: AED 5,000

Deductible Amounts:

• Client dinner → AED 5,000 (50%)

• Corporate event → AED 7,500 (50%)

• Birthday party → AED 0 (not deductible)

Total Deductible Entertainment = AED 12,500

________________________________________

📌 Additional Guidelines

1. Entertainment of Related Parties

– Transfer pricing rules apply. The expense must be at arm’s length and documented appropriately.

2. Event Sponsorship

– If the entertainment is linked to marketing or brand promotion (e.g., public seminars or client acquisition), it may fall under advertising expense, which is fully deductible.

3. Employee Welfare vs. Entertainment

– Routine staff benefits like meals during working hours may be fully deductible, but lavish events are subject to the 50% limit.

4. Free Zone Entities

– Qualifying Free Zone Persons must segregate qualifying vs. non-qualifying income, and improper entertainment claims may risk losing the 0% tax status.

________________________________________

❌ Risks of Overclaiming Entertainment Expenses

• FTA disallowance during audit

• Penalties for incorrect return filing

• Reduction in Qualifying Income for Free Zone entities

• Reputational damage for aggressive tax practices

________________________________________

📌 Summary Table

Topic Explanation

Legal Reference Article 32, Federal Decree-Law No. 47 of 2022

Deductibility Limit 50% of eligible expenses

Applies To Client meals, hospitality, entertainment

Not Allowed Personal entertainment, undocumented events

Required Documents Receipts, purpose, guest list, proof of business intent

________________________________________

🧠 Expert Insight by Sheikh Anwar Accounting & Auditing LLC

At Sheikh Anwar Accounting & Auditing LLC, we help businesses:

✅ Classify entertainment expenses correctly

✅ Maintain tax-compliant documentation

✅ Separate personal and business-related spending

✅ Avoid penalties and overstatements

✅ Maximize allowable deductions under UAE CT law

________________________________________

📞 Contact Us

Have questions about which expenses qualify or how to document your entertainment spending?

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX