Checklist for Reverse Charge Compliance

Introduction

The Reverse Charge Mechanism (RCM) shifts the responsibility of accounting for VAT from the supplier to the buyer in specific cases, such as import of services or goods, and certain local supplies. While RCM can simplify cross-border trade, it imposes additional compliance obligations on businesses in the UAE.

To ensure you're fully compliant, use this comprehensive checklist tailored to UAE VAT regulations.

________________________________________

📋 Reverse Charge Compliance Checklist

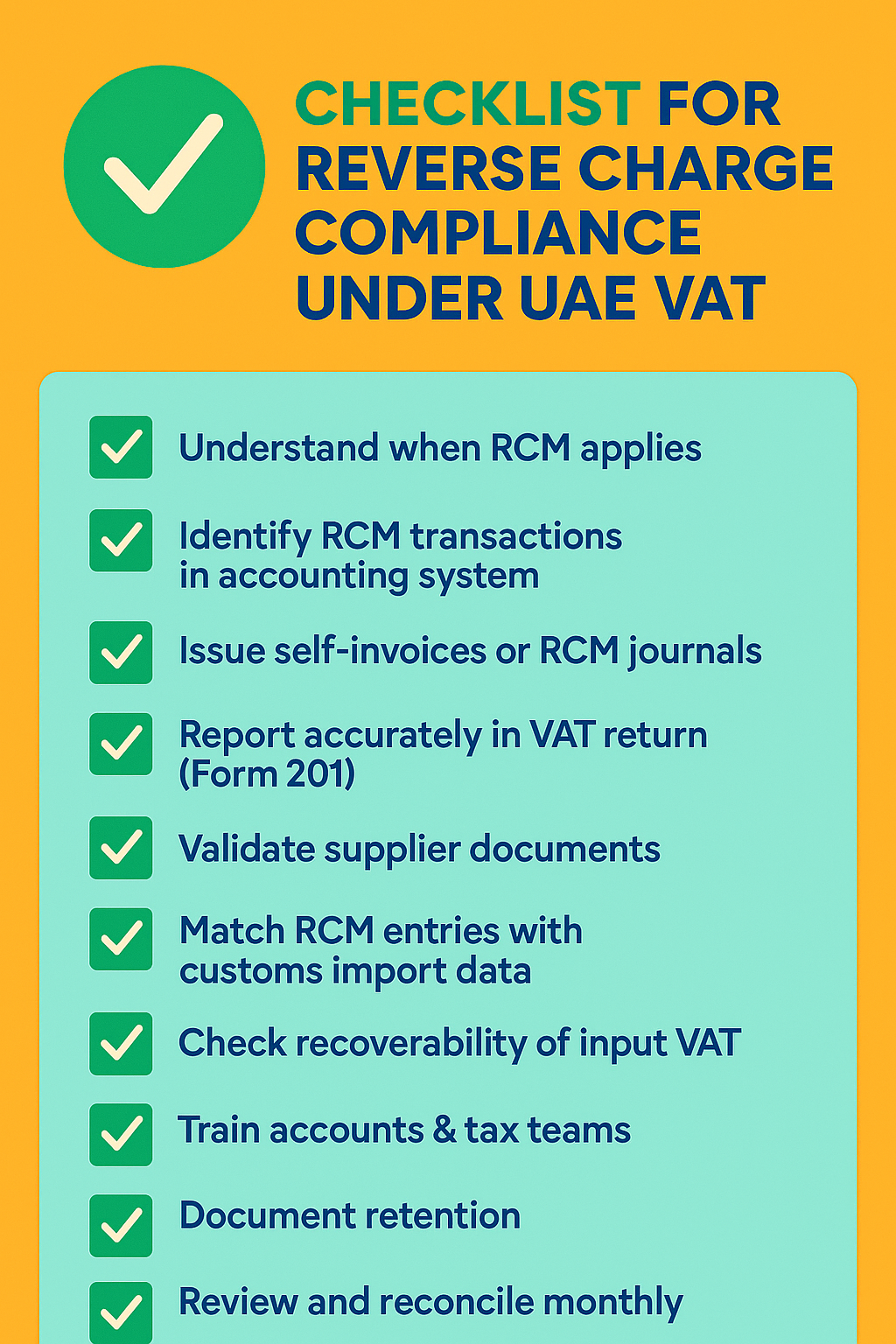

✅ 1. Understand When RCM Applies

Ensure your team is aware of all cases where RCM applies, including:

• Import of services from outside UAE (Article 48 of the VAT Law)

• Import of goods via customs (Box 3 auto-populated)

• Specified local supplies (e.g., gold, crude oil, hydrocarbons, real estate transactions in designated zones)

🔍 Refer to FTA Public Clarifications and Cabinet Decision No. 52 of 2017 for full list.

________________________________________

✅ 2. Identify RCM Transactions in Accounting System

• Maintain separate RCM ledger/accounts in your ERP or accounting software.

• Mark all supplier invoices where VAT is not charged but must be accounted via RCM.

________________________________________

✅ 3. Issue Self-Invoices or RCM Journals

• Generate RCM self-invoices for imported services or goods if not provided by the supplier.

• Create journal entries:

o Debit: Expense or asset

o Credit: Output VAT (Box 6)

o Debit: Input VAT (Box 10), if eligible

________________________________________

✅ 4. Report Accurately in VAT Return (Form 201)

• Box 3: Imports of goods via customs (auto-filled)

• Box 6: All other RCM supplies – manually entered

• Box 10: Recoverable VAT – include eligible RCM input VAT

Make sure the output VAT in Box 6 matches input VAT in Box 10 if fully recoverable.

________________________________________

✅ 5. Validate Supplier Documents

• Confirm supplier is non-resident and the supply would be taxable in UAE.

• Keep contracts, invoices, and import documentation ready for FTA audits.

________________________________________

✅ 6. Match RCM Entries With Customs Import Data

• Verify the values in Box 3 match customs declarations.

• Ensure TRN is linked with the customs system to avoid missing imports.

________________________________________

✅ 7. Check Recoverability of Input VAT

• Input VAT under RCM can only be recovered if related to taxable supplies.

• Do not claim input VAT for exempt or non-business use.

________________________________________

✅ 8. Train Accounts & Tax Teams

• Conduct internal training on how to:

o Identify RCM transactions

o Record entries correctly

o File VAT returns accurately

________________________________________

✅ 9. Document Retention

• Retain documents for 5 years (15 years for real estate).

• Include:

o Invoices

o Customs declarations

o Journal vouchers

o Contracts and agreements

________________________________________

✅ 10. Review and Reconcile Monthly

• Perform monthly checks:

o Compare RCM entries with VAT return

o Verify no missed entries or incorrect input tax recovery

• Reconcile with suppliers and freight agents

________________________________________

⚠️ Penalties for Non-Compliance

• Incorrect filing or failure to apply RCM may result in:

o AED 1,000 to AED 5,000 penalties per return

o Audit red flags and interest on unpaid VAT

________________________________________

🛡️ Final Tip

RCM compliance is a critical part of VAT health in your business. Automate wherever possible, stay updated with FTA changes, and consult a registered Tax Agent when in doubt.

If you need professional support, contact Sheikh Anwar Accounting & Auditing LLC or visit www.sa-auditors.com.