Case Study – Holding Structure with QFZP

Introduction

The UAE Corporate Tax (CT) regime has introduced unique opportunities for businesses operating within Free Zones. One such opportunity is the Qualifying Free Zone Person (QFZP) regime, which allows certain income to be subject to a 0% corporate tax rate, provided the entity meets specific conditions.

It examines how a holding company structure can benefit under the QFZP regime, highlighting eligibility, advantages, and compliance requirements.

________________________________________

📌 Background

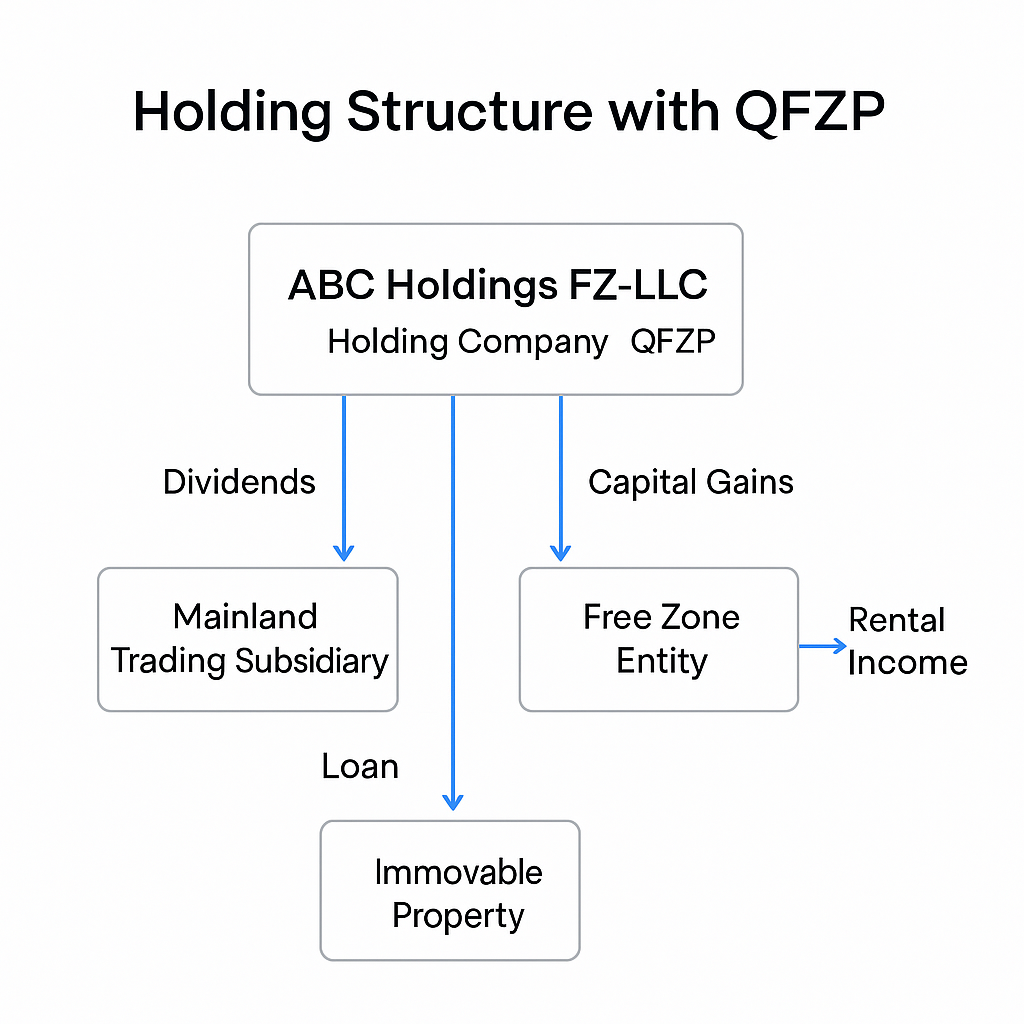

A group of investors establishes ABC Holdings FZ-LLC in a UAE Free Zone. The primary role of ABC Holdings is to:

• Hold shares in multiple operating subsidiaries (both mainland and free zone entities).

• Receive dividends and capital gains from these subsidiaries.

• Manage financing activities within the group.

The investors wish to leverage the QFZP status to reduce the overall tax liability while maintaining compliance with UAE CT Law.

________________________________________

✅ Qualifying Conditions for QFZP

For ABC Holdings FZ-LLC to qualify as a QFZP, it must meet these requirements:

1. Adequate Substance – The company should have staff, premises, and adequate expenditure in the Free Zone to carry out holding activities.

2. Qualifying Income – The main income should be from:

o Dividends from subsidiaries

o Capital gains on disposal of shares

o Passive income (interest, royalties) from related parties in line with Cabinet Decision No. 100 of 2024

3. Non-Excluded Activities – The holding company must avoid excluded activities (e.g., income from immovable property in the UAE other than commercial property, or income from non-qualifying related party financing).

4. Transfer Pricing Compliance – Related-party transactions must be at arm’s length and documented.

5. Audited Financial Statements – Annual audited accounts are mandatory to maintain QFZP status.

________________________________________

💡 Case Analysis

1. Dividend Income

ABC Holdings receives AED 10 million in dividends from its 100% owned mainland trading subsidiary.

• Treatment: Dividend income is considered Qualifying Income, hence subject to 0% tax under the QFZP regime.

2. Capital Gains

The company sells its 20% stake in another free zone entity, realizing a capital gain of AED 3 million.

• Treatment: Capital gains on shares are Qualifying Income, taxed at 0%.

3. Intercompany Loan

ABC Holdings extends a loan to its mainland subsidiary at market interest rates. The subsidiary pays AED 1 million in annual interest.

• Treatment: If the loan qualifies under permissible related-party financing rules, interest may also be treated as Qualifying Income. However, if deemed an Excluded Activity (e.g., lending outside permitted scope), the income could attract 9% tax.

4. Non-Qualifying Revenue

Suppose ABC Holdings leases out office space in the Free Zone and earns AED 500,000 rental income.

• Treatment: Rental income from immovable property is non-qualifying, subject to 9% tax.

________________________________________

📊 Summary of Tax Impact

Income Stream Amount (AED) QFZP Treatment Tax Rate Tax Payable (AED)

Dividend Income 10,000,000 Qualifying 0% 0

Capital Gains 3,000,000 Qualifying 0% 0

Intercompany Loan Interest 1,000,000 Conditional 0% / 9% 0 or 90,000

Rental Income 500,000 Non-Qualifying 9% 45,000

Total 14,500,000 — — 45,000 (max)

________________________________________

⚖️ Key Takeaways

• Holding structures in Free Zones are highly efficient for managing group entities.

• Dividend and capital gains are generally tax-free under QFZP, provided conditions are satisfied.

• Careful structuring of intercompany loans and property income is essential to avoid disqualification.

• Maintaining substance, audited accounts, and TP compliance is non-negotiable for QFZP status.

________________________________________

🏢 About Us

At Sheikh Anwar Accounting & Auditing LLC (MOE Reg. Entry No. 5817 | LC4695-01), we assist businesses in structuring their entities to maximize QFZP benefits, ensure corporate tax compliance, and achieve long-term tax efficiency.

📩 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com