Cap on Deductibility of Net Interest

The UAE Corporate Tax regime, introduced through Federal Decree-Law No. 47 of 2022, brought forward several provisions to prevent base erosion and profit shifting (BEPS). One such provision is the cap on deductibility of net interest expense.

Interest expenses are common in business financing; however, the government places limits on how much of it can be deducted when computing taxable income. These limits are designed to prevent companies from reducing their tax liability through excessive interest payments—especially to related parties.

Sheikh Anwar Accounting & Auditing LLC explains the 30% EBITDA interest deduction cap, its application, exemptions, and implications.

________________________________________

📜 Legal Basis

The cap on net interest deductibility is primarily defined under:

• Article 29 of Federal Decree-Law No. 47 of 2022

• Ministerial Decision No. 126 of 2023

• OECD BEPS Action 4 (international influence)

________________________________________

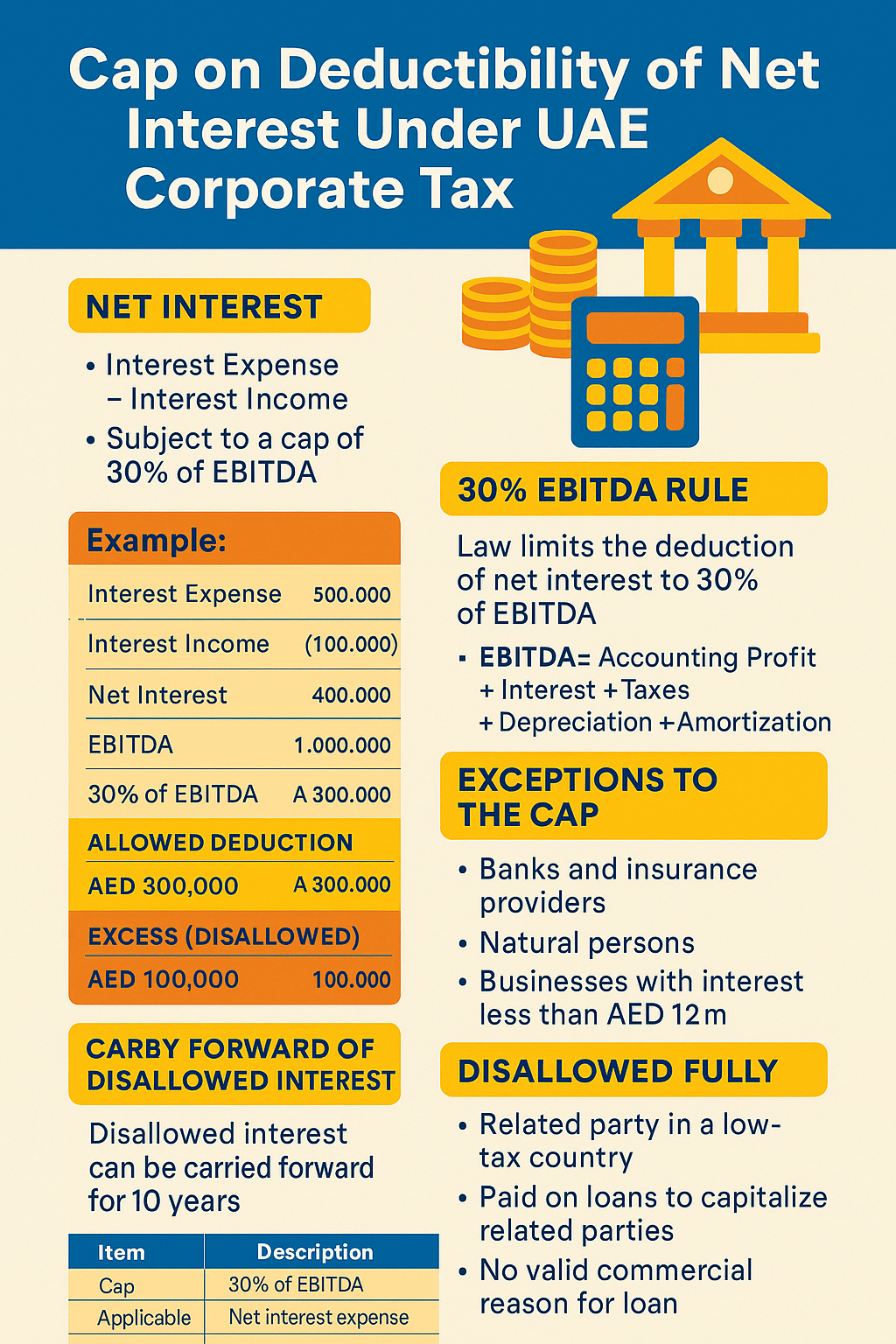

💡 What Is Net Interest?

Net Interest = Interest Expense – Interest Income

Only the net amount of interest can be deducted, and it is subject to a cap of 30% of adjusted EBITDA, unless the business qualifies for exemption.

________________________________________

🧮 How the 30% EBITDA Rule Works

The law limits the deductibility of net interest expense to 30% of the business’s EBITDA, calculated as:

EBITDA = Accounting Profit + Interest + Taxes + Depreciation + Amortization

Example: Amount (AED)

Interest Expense 500,000

Interest Income (100,000)

Net Interest 400,000

EBITDA 1,000,000

30% of EBITDA 300,000

Allowed Deduction = AED 300,000

Excess (disallowed) = AED 100,000 (can be carried forward)

________________________________________

🔁 Carry Forward of Disallowed Interest

Disallowed net interest expense (exceeding the 30% EBITDA cap) can be carried forward for up to 10 years, subject to continued business activity.

________________________________________

🛑 Exceptions to the Cap

The following entities are not subject to the 30% EBITDA limitation:

1. Banks and insurance providers

2. Natural persons conducting business

3. Businesses with total net interest expense of less than AED 12 million per tax year (de minimis threshold)

________________________________________

🚫 Disallowed Interest Regardless of EBITDA

In addition to the cap, interest is not deductible at all if:

• Paid to a related party in a low or no-tax jurisdiction

• Used to finance dividends, share purchases, or capital contributions to related parties

• There is no valid commercial purpose for the loan

These anti-abuse rules override the 30% deduction even if EBITDA allows it.

________________________________________

📁 Documentation & Transfer Pricing

Businesses must also comply with Transfer Pricing rules (Articles 34–36) when dealing with:

• Group loans

• Intra-company financing

• Interest to shareholders or affiliates

✅ Maintain arm’s length pricing

✅ Prepare Master File and Local File (if thresholds are met)

________________________________________

📌 Summary Table

Item Description

Cap 30% of EBITDA

Applicable To Net interest expense (interest expense – interest income)

Exemptions Banks, insurers, businesses < AED 12M interest

Carry Forward Excess deductible for 10 years

Disallowed Fully Related party loans with abusive purpose

TP Rules Must comply if interest is paid to connected parties

________________________________________

🧠 Expert Insight from Sheikh Anwar Accounting & Auditing LLC

Failing to adhere to the 30% cap can result in:

❌ Overstated deductions

❌ Fines and penalties from FTA

❌ Risk to Free Zone 0% status (if applicable)

We assist businesses in:

✅ Applying the cap correctly

✅ Calculating EBITDA accurately

✅ Structuring debt in a tax-efficient manner

✅ Preparing Transfer Pricing documentation

✅ Filing compliant Corporate Tax returns

________________________________________

📞 Contact Us for Advisory Support

If your business uses debt financing or intra-group loans, ensure your interest deductions are optimized and compliant.

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX