Benchmarking Studies in Transfer Pricing

Introduction

Benchmarking is the backbone of transfer pricing (TP). It provides independent market evidence that related-party prices or margins are arm’s length—which is the core requirement under OECD Guidelines and the UAE Corporate Tax regime (Federal Decree-Law No. 47 of 2022). A well-executed benchmarking study reduces audit risk, avoids penalties, and brings clarity to pricing policies across the group.

________________________________________

1) What is a Benchmarking Study?

A benchmarking study identifies comparable uncontrolled transactions (or companies) and derives an arm’s length range of prices or profit indicators. Your related-party results are then tested against this range. In practice, benchmarking supports:

• Pricing for intercompany goods (buy–sell/distribution)

• Services (management, IT, support)

• Intra-group financing (interest rates, guarantees)

• IP licensing/royalties (rates and bases)

• Contract manufacturing and tolling arrangements

________________________________________

2) When do UAE businesses need it?

• You have material related-party cross-border dealings

• You must prepare a Local File/Master File (when prescribed thresholds apply)

• The FTA requests contemporaneous documentation

• You’re implementing/renewing an APA or defending an audit

________________________________________

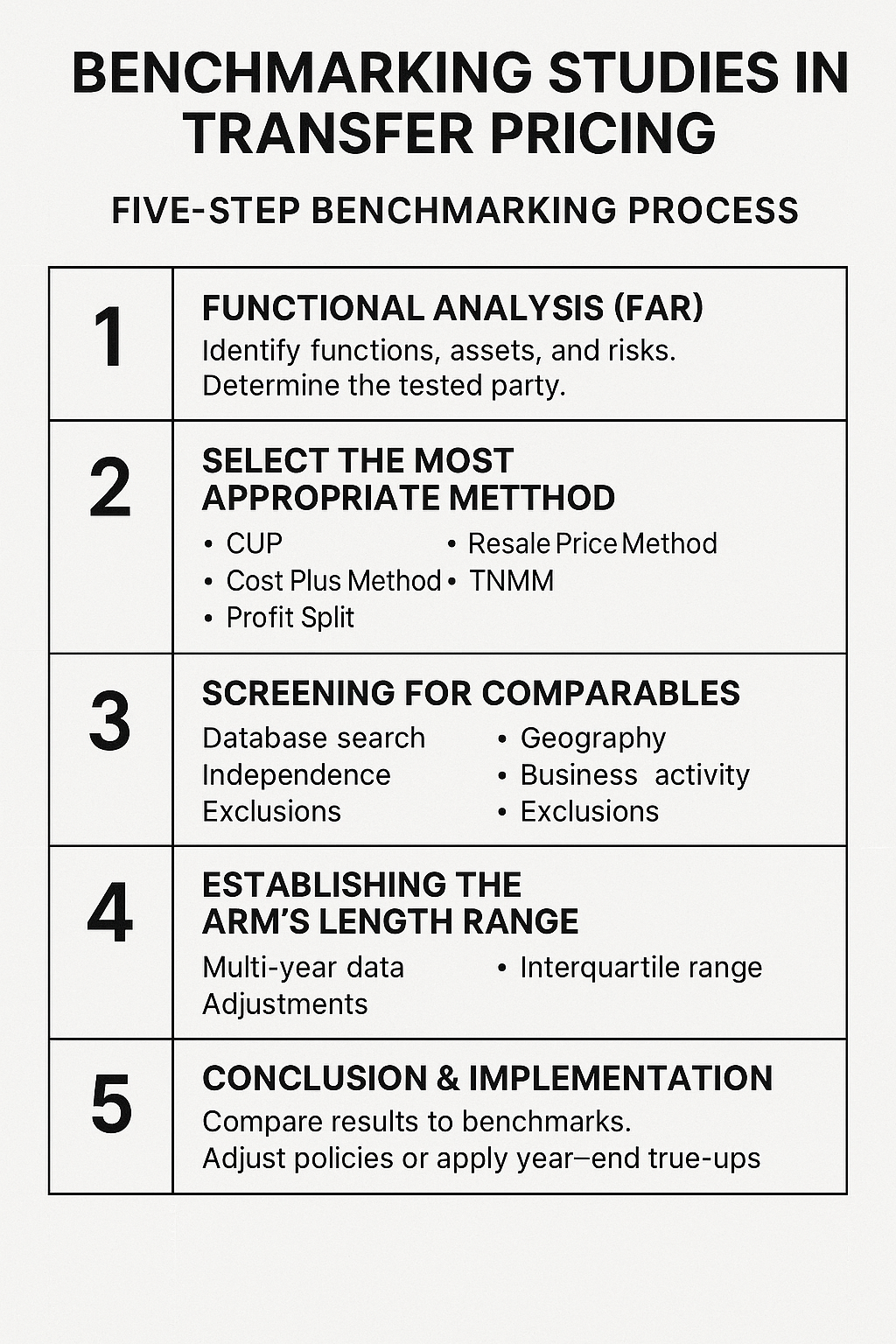

3) Core Methodology—Step by Step

Step A: Delineate the Controlled Transaction

• Map who does what, uses which assets, and assumes which risks (FAR analysis).

• Confirm the tested party: the entity with the simpler functions and limited intangibles/risks (often the distributor or contract manufacturer).

Step B: Select the “Most Appropriate Method”

• CUP (Comparable Uncontrolled Price) – strongest for commodities/royalties.

• Resale Price Method – limited-risk distributors.

• Cost Plus Method – routine service providers/contract manufacturers.

• TNMM – most common; tests a profit level indicator (PLI) such as:

o Operating Margin (OP/OR)

o Return on Costs (OP/OC)

o Berry Ratio (Gross Profit/Operating Expenses) for limited-risk distributors/services

o Return on Capital Employed (ROCE) where asset intensity is key

• Profit Split – integrated operations or unique intangibles on both sides.

Step C: Build a Comparable Set (Database Screening)

Use reputable databases (e.g., Orbis, Bloomberg, RoyaltyStat, ktMINE). Apply objective filters:

• Geography: UAE / GCC / Middle East–Africa; expand to broader EMEA only if needed.

• Status: Independent, active, non-governmental, non-consolidated.

• Size: Reasonable revenue/asset bands to exclude micro or outlier giants.

• Qualitative screening:

o Match business model (e.g., wholesale distributor vs. retailer)

o Exclude own-brand/entrepreneurial companies if testing a limited-risk distributor

o Remove entities with persistent losses, distress, or extraordinary events

o Check for R&D/marketing intangibles that don’t match the tested party

Step D: Compute the Arm’s Length Range

• Use multi-year data (typically 3 years) to smooth volatility.

• Calculate the PLI for each comparable, remove statistical outliers, and apply the interquartile range (IQR: 25th–75th percentiles).

• Consider comparability adjustments where relevant:

o Working capital (receivables, payables, inventory)

o Capacity utilisation differences

o Accounting reclassifications (e.g., operating vs. non-operating items)

Step E: Conclude & Implement

• Compare the tested party’s actual results to the arm’s length range.

• Policy outcome examples:

o Distribution: set a target OP/OR of, say, 3.5%–6.5% (IQR example).

o Services: charge cost plus 5%–8% based on routine support services.

o Loans: set an arm’s length interest rate using credit rating/tenor curves.

• Document any true-up/true-down mechanism before year-end.

________________________________________

4) Special Topics (UAE-relevant)

a) Free Zone Entities (FZEs/FZCOs)

• If claiming Qualifying Income under Free Zone rules, ensure related-party pricing is arm’s length—or you risk disqualification. Benchmarking supports substance and arm’s length outcomes.

b) Commodity & Jewellery Sector

• Where CUP exists (e.g., LME for metals), CUP often prevails. For downstream distribution, TNMM with Berry Ratio or OP/OR may be appropriate if inventory risk is limited.

c) Management/Head-Office Charges

• Apply the benefit test and maintain time-writing / allocation keys. Benchmark cost-plus mark-ups against routine support-service studies, not high-value advisory.

d) Intra-Group Financing

• Align with credit rating, tenor, currency, collateral/guarantees. Use internal/external comparables and consider implicit support.

e) Intangibles & Royalties

• Start with CUP (license databases). Cross-check with profit-split/TNMM where returns to intangibles are shared.

________________________________________

5) What Goes into a Benchmarking Report?

• Executive summary & conclusion

• Group overview, industry analysis

• Detailed FAR and tested party selection

• Method choice & PLI rationale

• Search strategy, quantitative filters, qualitative screening notes

• Comparable financials, adjustments, IQR calculations

• Sensitivity checks (single-year vs. multi-year; with/without certain comparables)

• Pricing policy and year-end adjustment mechanism

• Compliance mapping to Local File/Master File requirements

________________________________________

6) Quality Pitfalls to Avoid

• Treating global giants or brand-owners as comparables for a limited-risk entity

• Mixing retail with wholesale distributors

• Ignoring working capital differences

• Using single-year data in a volatile market without explanation

• Blind “database dumps” without qualitative review

• Copy-pasting foreign ranges without regional reality checks

________________________________________

7) Refresh & Maintenance

• Annual update of financials to monitor compliance during the year.

• Full refresh (search & screening) every 3 years or when business model/market changes.

• Maintain contemporaneous documentation—ready to share with the FTA upon request.

________________________________________

8) Illustrative Example (TNMM – Limited-Risk Distributor)

• Tested party: UAE distributor, no marketing intangibles, routine risks

• PLI: Operating Margin (OP/OR)

• Result of screening: 10 comparables; after outlier removal, IQR = 3.2% – 6.8%

• Tested party projected OP/OR: 5.1% → Compliant (within IQR)

• Pricing policy: quarterly monitoring; year-end true-up if margin <3.2%

________________________________________

9) Practical Checklist (Save This)

• Clear FAR and tested party

• Right method & PLI

• Transparent search filters + qualitative screening

• Multi-year analysis + IQR

• Adjustments (working capital/capacity)

• Policy & true-up mechanism

• Map to Local File and Master File

________________________________________

How We Can Help

Benchmarking Studies (distribution, services, manufacturing, financing, royalties)

Local File / Master File preparation

Intra-group policy design & year-end true-ups

APA feasibility and submissions

FTA audit support & defence files

________________________________________

Sheikh Anwar Accounting & Auditing LLC

MOE Registered Auditor – Entry No. 5817 · Company Entry No. LC4695-01

🌐 www.sa-auditors.com ·

✉️ info@sa-auditors.com ·

📱 +971-XX-XXXXXXX