Asset Impairment Losses

Introduction

In the dynamic business environment of the UAE, assets may lose value due to market conditions, technological changes, or operational damage. The resulting impairment losses must be accounted for in the financial statements—but how are these treated under the UAE Corporate Tax Law?

Sheikh Anwar Accounting and Auditing LLC explains what constitutes an impairment loss, when such losses are tax-deductible, and what documentation is necessary to support such claims in the eyes of the Federal Tax Authority (FTA).

________________________________________

📜 Legal & Accounting Framework

The treatment of impairment losses in the UAE is governed by:

• Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses

• Ministerial Decision No. 114 of 2023 on Deductible and Non-Deductible Expenses

• IFRS Standards (IAS 36 – Impairment of Assets)

________________________________________

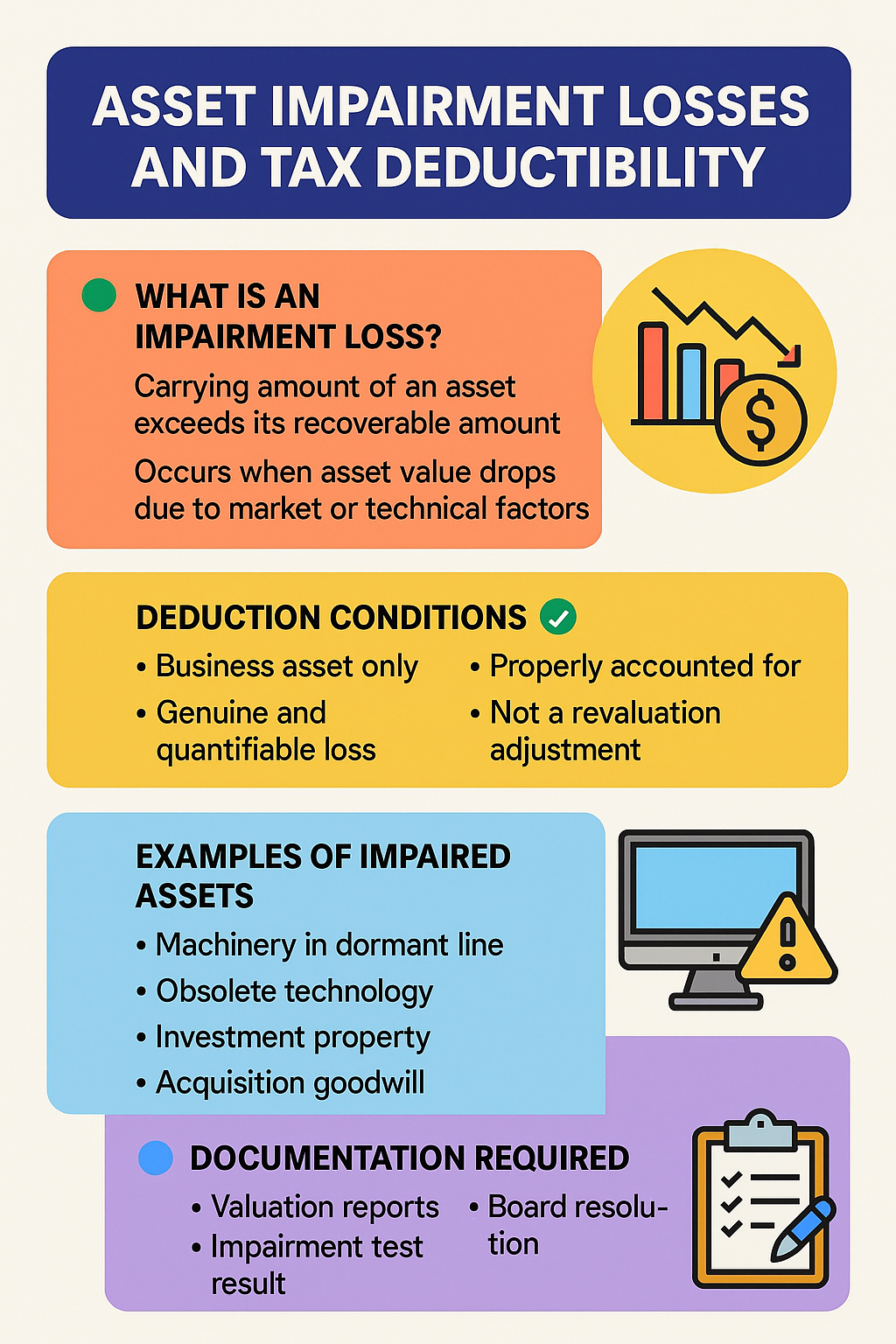

📌 What is an Impairment Loss?

An impairment loss arises when the carrying amount of an asset exceeds its recoverable amount, which is the higher of:

1. Fair Value Less Costs to Sell

2. Value in Use (Present value of future cash flows from the asset)

This usually happens when:

• Market value declines due to economic downturns

• Machinery or equipment becomes obsolete

• A factory or branch shuts down

• Intangible assets (e.g., goodwill) lose commercial value

________________________________________

✅ Are Impairment Losses Deductible Under Corporate Tax?

Yes, but only if the loss meets specific conditions. UAE Corporate Tax Law allows deduction of genuine, verifiable impairment losses, especially where the asset is used in business operations.

Deductibility Conditions:

Condition Requirement

Business Use The asset must be used wholly and exclusively for the taxable business

Impairment is genuine and measurable Backed by technical, financial, or market valuation evidence

Proper accounting treatment Impairment loss must be recognized in books as per IFRS

Not a capital revaluation Revaluation adjustments are not deductible

Not related to exempt or unrelated income Only losses related to taxable operations are deductible

________________________________________

🧾 Examples of Impaired Assets

Asset Type Impairment Trigger Deductible?

Machinery in discontinued line Market demand collapse ✅ Yes

Goodwill from past acquisition Declining cash flows from acquired unit ✅ Yes

Investment property Long-term tenant exits, no new income expected ✅ Yes

Land revalued below cost Passive holding, not used in business ❌ No

Intangible software license Technology obsolete, no future benefit ✅ Yes

________________________________________

🚫 Non-Deductible Impairment Scenarios

• Impairment of non-business assets (e.g., private vehicles, personal real estate)

• Revaluation losses on passive investments

• Subjective impairments with no documentation

• Provisions for impairment without recognition in accounts

• Impairment on assets used to generate exempt income

________________________________________

📂 Documentation Requirements

To ensure deductibility of impairment losses, businesses should maintain:

• Valuation reports from qualified experts

• Impairment testing schedules (as per IAS 36)

• Board resolutions approving the impairment

• Ledger entries and financial statements

• Detailed asset registers and usage logs

• Evidence of business use (photos, lease, invoices)

Sheikh Anwar Accounting and Auditing LLC helps ensure that impairment losses are substantiated, accurately measured, and compliant with both tax and IFRS guidelines.

________________________________________

🧠 Real-Life Example

ABC Manufacturing LLC has an old CNC machine with AED 500,000 carrying value. Due to automation upgrades, its fair value dropped to AED 150,000 and expected future use is limited.

• Impairment Test: Recoverable value = AED 150,000

• Impairment Loss = AED 500,000 – AED 150,000 = AED 350,000

✅ The loss is recognized in the accounts and is deductible for corporate tax in that year, assuming documentation is in place.

________________________________________

🧾 IFRS vs. Tax Treatment

Aspect IFRS UAE Corporate Tax

Recognition Required under IAS 36 Allowed if all tax conditions are met

Reversal of impairment Allowed in later periods (except goodwill) Deduction must be adjusted accordingly

Disclosure Required in notes to financials May be reviewed during FTA audit

________________________________________

🏢 Free Zone Entities & Impairment

For Free Zone entities benefiting from 0% tax on Qualifying Income, impairment losses must be allocated only to taxable income segments. Proper segregation of accounts is critical.

________________________________________

📣 Final Thoughts

Impairment is not just an accounting adjustment—it has real tax implications. UAE businesses can deduct impairment losses, but only with proper documentation, accounting alignment, and a clear business connection.

At Sheikh Anwar Accounting and Auditing LLC, we:

• Help businesses conduct impairment tests in line with IFRS

• Advise on tax-deductible treatment of asset write-downs

• Prepare FTA-audit-ready documentation and reporting

________________________________________

📩 Need assistance with impairment testing and tax reporting?

📧 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com