Arm’s Length Principle Explained

Introduction

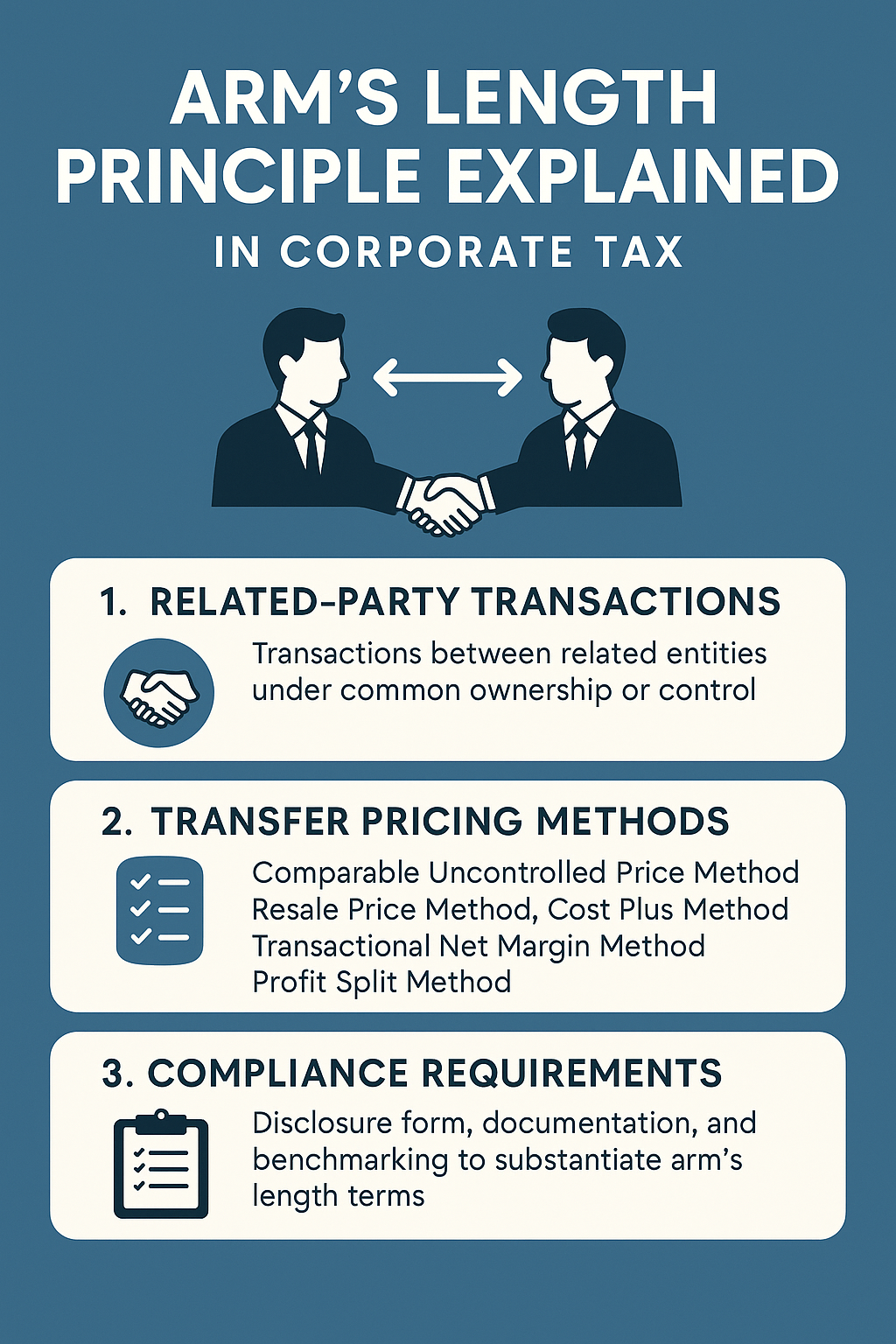

The Arm’s Length Principle (ALP) is a cornerstone of Transfer Pricing (TP), now embedded in the UAE Corporate Tax framework under Federal Decree-Law No. 47 of 2022. It requires that all transactions between related parties and connected persons be conducted as if they were independent entities dealing at market terms.

This principle prevents profit shifting, ensures fairness in taxation, and strengthens the UAE’s compliance with OECD standards and global tax transparency initiatives.

1. What Does the Arm’s Length Principle Mean?

At its core, the Arm’s Length Principle means:

👉 Related parties must transact as if they were unrelated.

The price, terms, and conditions applied must reflect what two independent businesses would agree upon in comparable circumstances.

This applies to:

Sale/purchase of goods.

Services (management, IT, back-office support).

Loans and financing arrangements.

Use of intellectual property (royalties, licensing).

Cost-sharing agreements within group companies.

2. Why is it Important in UAE Corporate Tax?

Prevents base erosion and profit shifting (BEPS).

Ensures taxable profits are reported where economic activity occurs.

Protects government tax revenues while maintaining fairness.

Builds international trust, keeping UAE off tax blacklists.

Helps companies maintain Free Zone incentives, since non-arm’s length pricing can disqualify them.

3. Transfer Pricing Methods under ALP

The UAE follows OECD-approved methods for applying the Arm’s Length Principle:

Comparable Uncontrolled Price (CUP) Method – comparing prices to similar transactions between unrelated parties.

Resale Price Method – ensuring resale margins are consistent with independent distributors.

Cost Plus Method – adding an arm’s length margin to the cost of providing goods/services.

Transactional Net Margin Method (TNMM) – comparing net profit margins to industry benchmarks.

Profit Split Method – dividing combined profits among group entities based on value contribution.

👉 Businesses must choose the “most appropriate method” based on the nature of the transaction and available data.

4. Documentation Requirements in UAE

To demonstrate compliance with ALP, UAE businesses must maintain:

Transfer Pricing Disclosure Form (filed with Corporate Tax Return).

Local File – detailing UAE entity’s related-party transactions and benchmarks.

Master File – providing group-level information on transfer pricing policies.

Intercompany Agreements – formal contracts reflecting ALP-based terms.

📌 Records must be retained for at least 7 years and align with financial statements and VAT filings.

5. Practical Examples

Example 1: Intragroup Services

A UAE parent company provides HR and IT services to its subsidiary.

ALP requires a fair allocation of costs plus an arm’s length markup (e.g., 5-10%) supported by benchmarking.

Example 2: Intragroup Loans

A UAE company lends funds to its affiliate abroad.

ALP requires the interest rate to reflect the borrower’s credit rating and market conditions, not just an arbitrary rate.

Example 3: Royalty Payments

A UAE subsidiary pays royalties to its parent for trademark use.

ALP requires the rate to be consistent with comparable licensing agreements in the market.

6. Risks of Non-Compliance

Failure to comply with ALP can lead to:

Tax adjustments by the Federal Tax Authority (FTA).

Penalties for under-reporting taxable income.

Loss of Free Zone 0% Corporate Tax benefits.

Higher risk of international tax disputes.

7. Strategic Approach for Businesses

Conduct FAR Analysis (Functions, Assets, Risks).

Benchmark Regularly to support transfer pricing.

Review Contracts to ensure they align with actual conduct.

Use ERP & Compliance Systems for accurate reporting.

Prepare for FTA Audits with complete documentation.

Conclusion

The Arm’s Length Principle is more than a technical rule—it’s the foundation of fair taxation under the UAE Corporate Tax regime. By applying OECD-approved TP methods, keeping robust documentation, and aligning related-party transactions with market conditions, businesses can mitigate risks, retain Free Zone benefits, and remain fully compliant.

For UAE companies, adopting a proactive ALP strategy means not only avoiding penalties but also building investor confidence and safeguarding long-term growth.

✍️ By Sheikh Anwar Accounting and Auditing LLC (SA-Auditors)

📍 Dubai, United Arab Emirates

🌐 www.sa-auditors.com

| ✉️ info@sa-auditors.com