AML Risk Matrix – How to Build One

Introduction

An effective Anti-Money Laundering (AML) compliance program starts with understanding and categorizing risks. One of the most practical tools to achieve this is an AML Risk Matrix — a structured framework that allows organizations to evaluate, quantify, and visualize their exposure to money laundering (ML) and terrorist financing (TF) threats.

For UAE businesses—especially Designated Non-Financial Businesses and Professions (DNFBPs) such as gold traders, real estate firms, accountants, and auditors—developing an AML risk matrix is not just best practice; it’s a regulatory expectation under Federal Decree-Law No. 20 of 2018 and Cabinet Decision No. 10 of 2019.

It provides a comprehensive guide on what an AML risk matrix is, why it’s important, and how to build one step by step.

________________________________________

1. What is an AML Risk Matrix?

An AML Risk Matrix is a visual and analytical tool that helps businesses:

• Identify areas vulnerable to ML/TF risk.

• Score risks across different categories (customers, products, geography, transactions, etc.).

• Evaluate the effectiveness of internal controls.

• Determine the overall residual risk level of the organization.

It allows compliance officers to make informed decisions, allocate resources efficiently, and implement a truly risk-based approach (RBA) aligned with FATF and UAE AML guidelines.

________________________________________

2. Importance of an AML Risk Matrix

A well-designed risk matrix is a key component of an Enterprise-Wide Risk Assessment (EWRA) and helps:

• Standardize how risks are measured across departments.

• Provide evidence of compliance to regulators and auditors.

• Support senior management in setting risk appetite.

• Detect control gaps and prioritize mitigation efforts.

In the UAE, regulators such as the Ministry of Economy (MOE) and free zone authorities like DMCC, ADGM, and DIFC expect every DNFBP to maintain a documented AML risk matrix as part of their compliance records.

________________________________________

3. Key Components of an AML Risk Matrix

Risk Category Example Risk Factors Why It Matters

Customer Risk Type of customer (individual, corporate, offshore, PEP), ownership structure, residency Determines exposure to anonymity or political influence

Product/Service Risk High-value goods, trade in precious metals, virtual assets, real estate Some products are easier to misuse for laundering

Geographic Risk Customer location, business jurisdictions, sanctioned or high-risk countries Cross-border operations can increase exposure

Delivery Channel Risk Face-to-face vs. online onboarding, use of agents/intermediaries Non-face-to-face channels pose verification challenges

Transaction Risk Large cash transactions, third-party payments, rapid fund movements Abnormal patterns may indicate suspicious activity

________________________________________

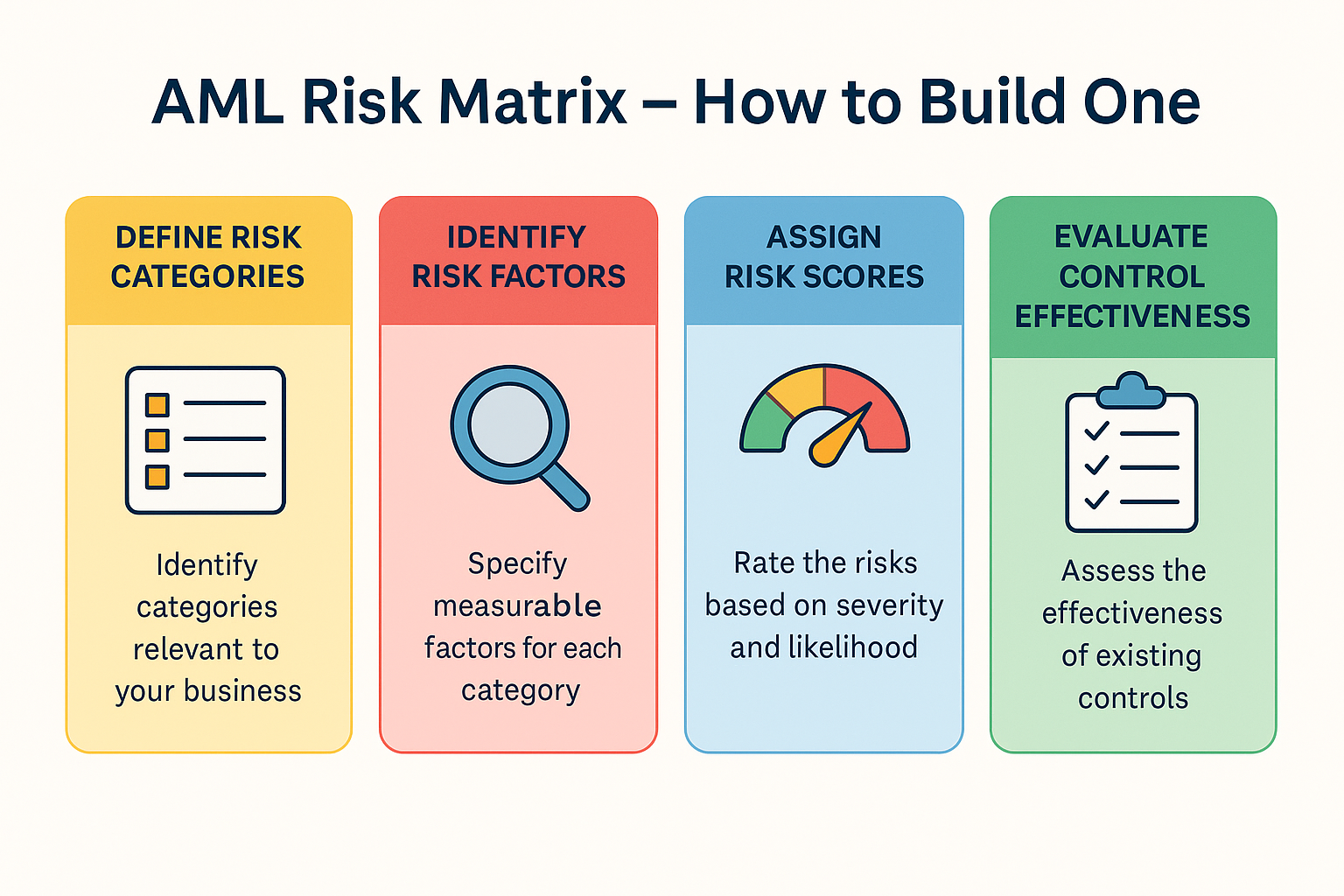

4. How to Build an AML Risk Matrix

Step 1: Define Risk Categories

Begin by identifying categories most relevant to your business. For DNFBPs in the UAE, the typical categories include:

• Customer Risk

• Product/Service Risk

• Geographic Risk

• Delivery Channel Risk

• Transaction Risk

You can also add other categories such as Technology Risk or Third-Party Risk depending on your operations.

________________________________________

Step 2: Identify Risk Factors

Under each category, specify measurable factors that contribute to ML/TF risk.

Example:

• Customer Risk: Offshore company, PEP, high net-worth individual, complex ownership.

• Product Risk: Gold trading, real estate brokerage, cross-border transactions.

• Geography: Clients from FATF greylisted countries.

• Delivery Channel: Remote onboarding or online payments.

________________________________________

Step 3: Assign Risk Scores

Create a scoring scale (e.g., 1 to 5 or Low–High) for each factor.

• 1 = Low Risk

• 2 = Medium-Low Risk

• 3 = Medium Risk

• 4 = Medium-High Risk

• 5 = High Risk

Assign weightages to reflect importance — for instance:

• Customer Risk (30%)

• Product Risk (25%)

• Geographic Risk (20%)

• Delivery Channel Risk (15%)

• Transaction Risk (10%)

________________________________________

Step 4: Evaluate Control Effectiveness

List existing AML controls (KYC, screening, transaction monitoring, reporting) and assess their effectiveness using similar scoring:

• 5 = Strong control, automated and tested

• 3 = Moderate, manual processes

• 1 = Weak, not implemented

This allows you to measure not just exposure, but also how well risks are mitigated.

________________________________________

Step 5: Calculate Residual Risk

Apply the following formula for each category:

Residual Risk = Inherent Risk × (1 – Control Effectiveness%)

Example:

• Inherent Risk (Customer) = 4.5

• Control Effectiveness = 70%

• Residual Risk = 4.5 × (1 - 0.70) = 1.35 (Low)

Aggregate the residual risks across categories to determine your overall company risk level (Low, Medium, or High).

________________________________________

Step 6: Visualize the Results

Plot your results on a heat map:

Control Effectiveness ↓ / Risk Severity → Low (1–2) Medium (3) High (4–5)

Strong (4–5) Low Low-Medium Medium

Moderate (3) Low-Medium Medium High

Weak (1–2) Medium High Very High

This helps management and regulators quickly interpret where your greatest vulnerabilities lie.

________________________________________

5. Example of an AML Risk Matrix

Risk Category Inherent Risk (1–5) Control Effectiveness (%) Residual Risk Score Residual Risk Rating

Customer Risk 5 60% 2.0 Medium-High

Product Risk 4 80% 0.8 Low

Geography Risk 3 70% 0.9 Low

Delivery Channel Risk 4 60% 1.6 Medium

Transaction Risk 3 65% 1.05 Low-Medium

Overall Risk Rating: Medium

This example illustrates how a company can use the matrix to identify which risk areas require Enhanced Due Diligence (EDD) or stronger controls.

________________________________________

6. Common Mistakes When Building a Risk Matrix

❌ Using a generic template without customizing to your business.

❌ Assigning equal weight to all risk categories.

❌ Ignoring the role of control testing in risk calculation.

❌ Failing to update the matrix after regulatory or business changes.

❌ Treating the risk matrix as a one-time document instead of a living framework.

________________________________________

7. How Often Should You Update the Risk Matrix?

Your AML Risk Matrix should be reviewed and updated:

• Annually as part of your EWRA.

• When new products, services, or geographies are introduced.

• After regulatory updates (e.g., FATF grey/blacklist changes).

• Following major control failures or audit findings.

________________________________________

8. Tools and Technology for Automating Risk Matrices

Modern AML software can automate matrix creation by:

• Integrating customer data and transaction trends.

• Applying AI-driven risk scoring models.

• Updating FATF and sanctions lists automatically.

• Generating real-time dashboards and risk heat maps.

Automation ensures accuracy, reduces manual workload, and strengthens compliance readiness.

________________________________________

9. Linking the Matrix to the Enterprise-Wide AML Risk Assessment (EWRA)

The AML risk matrix forms the quantitative core of your EWRA.

It helps justify:

• Why certain customers or countries are considered high risk.

• Why Enhanced Due Diligence (EDD) is necessary.

• How your AML resources are proportionally allocated.

This linkage demonstrates to regulators that your risk-based approach (RBA) is both measurable and defensible.

________________________________________

Conclusion

An AML Risk Matrix transforms abstract risk concepts into clear, measurable, and actionable insights. It allows businesses—especially in high-risk sectors like gold trading, real estate, and professional services—to comply with UAE AML laws effectively while maintaining operational efficiency.

At Sheikh Anwar Accounting & Auditing LLC, we assist UAE DNFBPs in building customized AML risk matrices that align with FATF standards and UAE Ministry of Economy guidance. Our tailored frameworks simplify risk scoring, ensure proper documentation, and strengthen regulatory compliance.

________________________________________

By Sheikh Anwar Accounting & Auditing LLC

AML & Compliance Experts in the UAE

📞 +971 4 876 9890 | ✉️ info@sa-auditors.com | 🌐 www.sa-auditors.com