AML Indicators in Virtual Asset Transactions

Introduction

The rise of virtual assets (VAs) such as cryptocurrencies, tokens, and other blockchain-based assets has created new opportunities for innovation in the financial sector. However, these same tools are often exploited by criminals for money laundering (ML) and terrorist financing (TF).

For regulators, compliance officers, and financial institutions in the UAE, understanding AML indicators in virtual asset transactions is critical to mitigating risk and ensuring compliance with Federal Decree-Law No. 20 of 2018 (AML/CFT) and the Cabinet Decision No. 10 of 2019, as well as recent FATF guidelines.

________________________________________

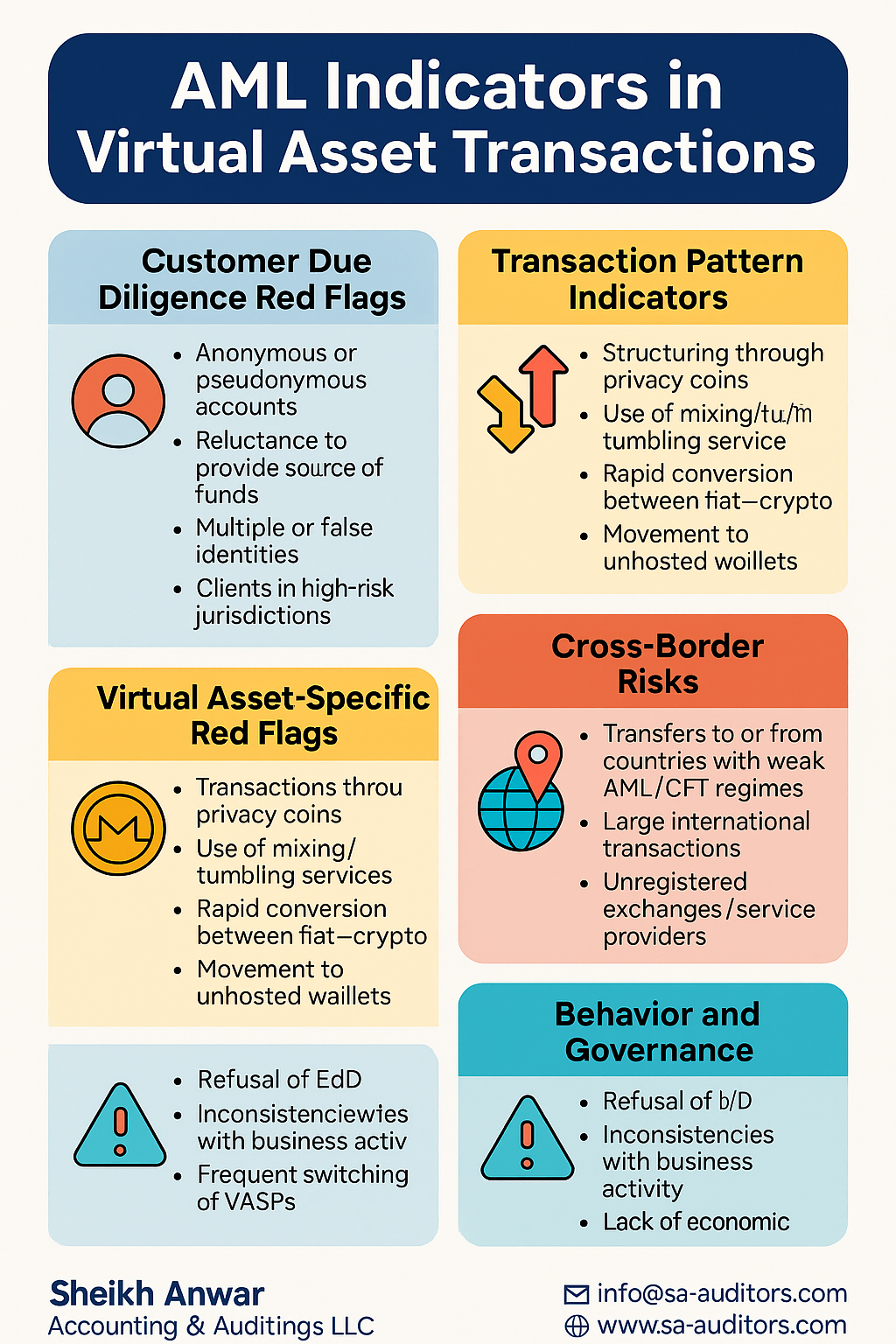

1. Customer Due Diligence (CDD) Red Flags

• Anonymous or pseudonymous accounts with limited KYC information.

• Reluctance to provide source of funds or source of wealth.

• Use of multiple or false identities across different VA platforms.

• Clients based in high-risk jurisdictions or countries on FATF’s grey/black lists.

________________________________________

2. Transaction Pattern Indicators

• Structuring or layering transactions into smaller amounts to avoid reporting thresholds.

• High frequency of transactions inconsistent with the customer’s profile.

• Transactions with no clear business or investment rationale.

• Use of multiple wallets or exchanges for the same transaction chain.

________________________________________

3. Virtual Asset-Specific Red Flags

• Transactions routed through privacy coins (e.g., Monero, Zcash) designed to hide traceability.

• Use of mixing/tumbling services to obscure transaction origins.

• Rapid conversion between fiat and crypto without a clear investment strategy.

• Sudden movement of assets from exchanges to unhosted wallets (self-custody) with no business justification.

________________________________________

4. Cross-Border Risks

• Transfers to or from countries with weak AML/CFT regimes.

• Large transactions conducted across multiple jurisdictions within short periods.

• Involvement of exchanges or service providers not registered with regulators (e.g., FSRA in ADGM or DFSA in DIFC).

________________________________________

5. Behavior and Governance Indicators

• Customers refusing enhanced due diligence (EDD).

• Inconsistencies between declared business activity and transaction volume.

• Frequent switching of virtual asset service providers (VASPs).

• Lack of alignment with UAE’s Economic Substance Regulations (ESR) for entities claiming to deal in VAs.

________________________________________

6. Industry-Specific Concerns in the UAE

• Use of gold, jewellery, or real estate transactions funded by VAs without traceable origins.

• Shell companies set up in free zones with no physical presence, yet engaging in VA trading.

• VAs used in crowdfunding or ICOs without proper licensing or disclosures.

________________________________________

7. How Compliance Officers Can Mitigate These Risks

• Implement blockchain analytics tools to track and trace VA transactions.

• Enforce strict KYC and EDD protocols for all customers dealing in VAs.

• Continuously monitor transactions for unusual or suspicious activity.

• Report Suspicious Activity Reports (SARs) promptly to the UAE FIU via goAML.

• Provide AML training for staff, especially on emerging typologies in the VA sector.

________________________________________

✅ Conclusion

Virtual assets are transforming the global financial system, but they also bring significant AML/CFT risks. By staying vigilant and monitoring these indicators, UAE businesses, auditors, and financial institutions can protect themselves from regulatory penalties, reputational damage, and criminal misuse.

________________________________________

📌 About Us

At Sheikh Anwar Accounting & Auditing LLC, we provide comprehensive support in AML compliance, outsourced MLRO services, transaction monitoring, and regulatory reporting. Our expertise covers high-risk industries, including gold, jewellery, and now virtual assets.

📧 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com