AML in Free Zones for DNFBPs

Introduction

The United Arab Emirates (UAE) is home to more than 40 free zones, each designed to attract foreign investment and foster international trade. From Dubai Multi Commodities Centre (DMCC) to Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC), these free zones have become hubs for diverse businesses. Among them, Designated Non-Financial Businesses and Professions (DNFBPs)—including jewellers, real estate brokers, lawyers, accountants, and corporate service providers—play a significant role.

However, with opportunity comes responsibility. Free zone DNFBPs are subject to strict Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) regulations, in line with UAE federal laws and international FATF standards. Non-compliance carries severe penalties, from heavy fines to license suspension.

________________________________________

1. AML Legal Framework for Free Zone DNFBPs

Although free zones operate under independent regulatory authorities, AML laws apply across the UAE. The following frameworks govern DNFBPs:

• Federal Decree-Law No. 20 of 2018 on AML and CTF – the cornerstone legislation.

• Cabinet Decision No. 10 of 2019 – implementing regulations, covering DNFBPs.

• Cabinet Resolution No. 74 of 2020 – concerning Targeted Financial Sanctions (TFS).

• Ministry of Economy AML oversight – supervises DNFBPs in most free zones, except those with independent regulators.

• Independent Free Zone Regulators:

o DIFC – supervised by the Dubai Financial Services Authority (DFSA).

o ADGM – supervised by the Financial Services Regulatory Authority (FSRA).

o DMCC, JAFZA, SAIF Zone, DAFZA – supervised by the Ministry of Economy as DNFBP regulators.

________________________________________

2. AML Obligations for Free Zone DNFBPs

Free zone DNFBPs must comply with the same obligations as mainland businesses, with added oversight from zone regulators. Key requirements include:

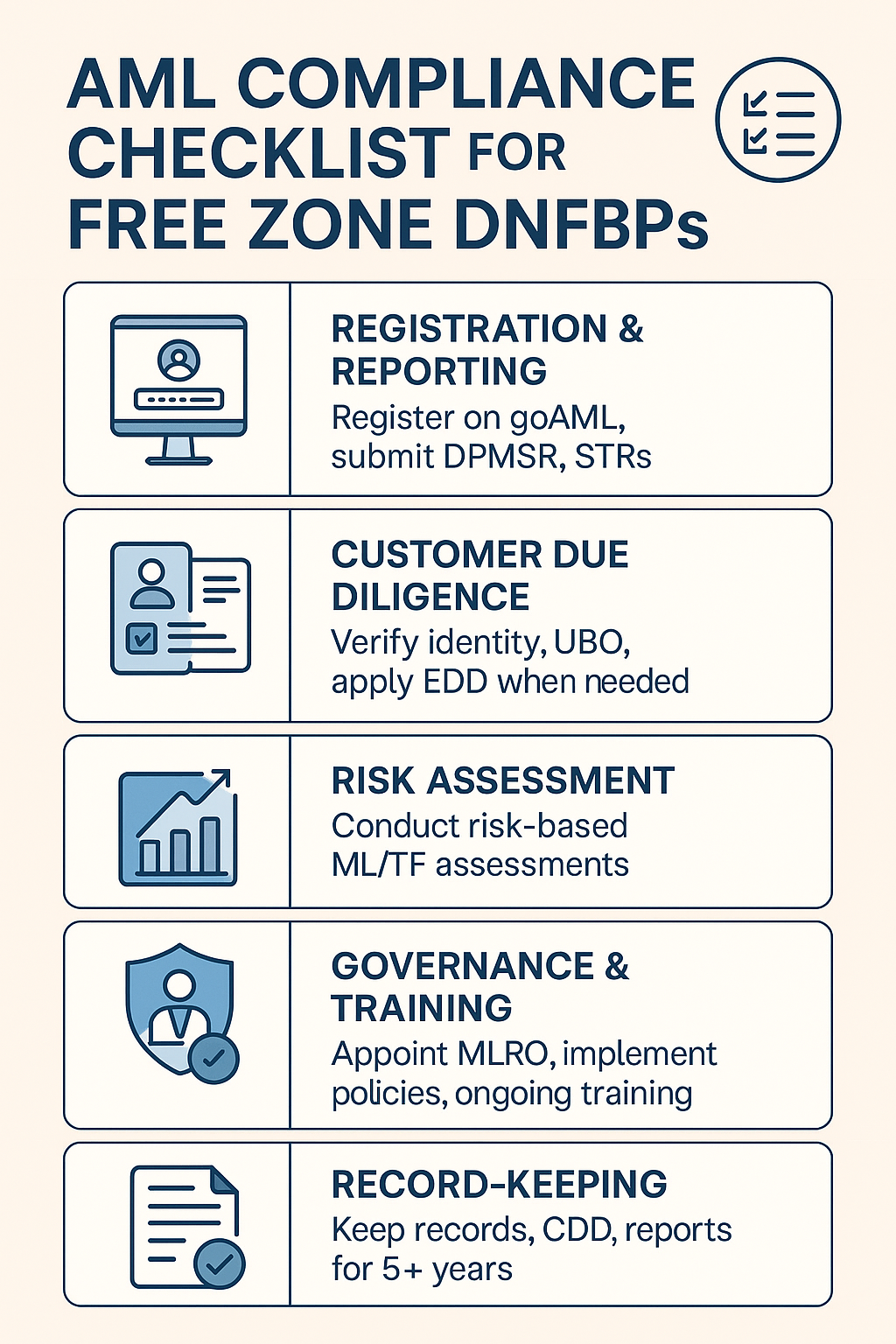

a) Registration & Reporting

• goAML Registration: All DNFBPs must register on the UAE FIU’s goAML portal.

• DNFBP Reports (DPMSR, Real Estate Reports, STRs): Transactions above thresholds and suspicious activity must be reported promptly.

b) Customer Due Diligence (CDD)

• Mandatory for any transaction of AED 55,000 or more in cash or wire transfers.

• Verification of customer identity and Ultimate Beneficial Owner (UBO).

• Enhanced Due Diligence (EDD) for politically exposed persons (PEPs) and high-risk jurisdictions.

c) Risk Assessments

• Conduct enterprise-wide ML/TF risk assessments, considering customer base, geography, and transaction type.

• Maintain risk-based policies and procedures.

d) Governance & Compliance

• Appoint a Money Laundering Reporting Officer (MLRO) or AML Compliance Officer.

• Implement AML manuals, procedures, and internal controls.

• Train employees regularly on AML/CTF obligations.

e) Record Keeping

• Maintain CDD records, transaction data, and reports for minimum five years.

________________________________________

3. Red Flags for Free Zone DNFBPs

Certain patterns should raise concern for DNFBPs in free zones:

• Clients insisting on cash transactions above the threshold.

• Companies with complex ownership structures involving offshore jurisdictions.

• Customers reluctant to disclose UBO details.

• Property or asset purchases by individuals with no clear source of income.

• Use of free zone entities for cross-border layering of funds.

________________________________________

4. Penalties for Non-Compliance

Free zone DNFBPs face penalties similar to mainland businesses, including:

• Fines: Ranging from AED 50,000 to AED 10 million.

• License Suspension or Revocation: Regulatory authorities can freeze or cancel trade licenses.

• Reputational Damage: Public fines harm credibility with banks and clients.

• Criminal Liability: Severe breaches can lead to imprisonment.

For example, in 2024, regulators in the UAE imposed hundreds of fines worth over AED 339 million on DNFBPs, including entities in free zones, for failing to meet AML requirements.

________________________________________

5. Why Free Zone DNFBPs Must Prioritize AML

Free zones attract global clients and high-value transactions, making them vulnerable to misuse. For DNFBPs, robust AML compliance is not just a legal requirement but a business necessity:

• Protects against reputational risk.

• Ensures continued access to banking facilities.

• Supports UAE’s standing in FATF compliance and international trade.

________________________________________

6. Best Practices for Free Zone DNFBPs

To strengthen compliance, DNFBPs should:

• Register on goAML and submit all required reports.

• Carry out risk-based customer onboarding.

• Screen clients and UBOs against sanctions lists.

• Keep internal AML policies and procedures updated.

• Appoint qualified compliance professionals.

• Engage in independent AML audits and training.

________________________________________

Conclusion

AML compliance in UAE free zones is more than a regulatory checkbox—it is an integral part of sustainable business operations. DNFBPs must proactively implement robust AML systems to avoid penalties and maintain their reputation in one of the world’s most dynamic business environments.

________________________________________

About Us

Sheikh Anwar Accounting and Auditing LLC is a Dubai-based auditing and compliance firm specializing in AML advisory, corporate tax, VAT, and transfer pricing. With extensive expertise in the gold, jewellery, real estate, and professional services sectors, we provide end-to-end compliance solutions for DNFBPs in both mainland and free zones.

📍 Address: Dubai Creek Tower, M 35, Dubai, UAE

📞 Contact: info@sa-auditors.com | +971-XXX-XXXX

🌐 Website: www.sa-auditors.com