AML for Fintech Startups in the Coming Years

Introduction

The rapid growth of financial technology (Fintech) has transformed the global financial landscape. Digital payments, blockchain platforms, neobanks, and peer-to-peer lending platforms are reshaping how financial services are delivered. However, this innovation also introduces new risks related to money laundering, fraud, and financial crime.

For fintech startups operating in the United Arab Emirates, complying with Anti-Money Laundering (AML) regulations will become increasingly important in the coming years. As regulators strengthen oversight, fintech companies must implement strong AML frameworks from the early stages of their operations.

________________________________________

Why AML is Critical for Fintech Startups

Fintech startups often handle high-volume digital transactions and cross-border payments. These activities can be attractive to criminals attempting to hide illicit funds. Without proper AML controls, fintech platforms may become vulnerable to misuse.

Key risks fintech companies face include:

• Anonymous digital transactions

• Rapid movement of funds across jurisdictions

• Use of cryptocurrency or digital assets

• Fraud and identity theft risks

Regulators expect fintech startups to address these risks by implementing robust AML compliance systems.

________________________________________

Regulatory Environment in the UAE

The UAE has developed a comprehensive regulatory framework to combat financial crime. Fintech companies operating in the country must comply with Federal Decree-Law No. 20 of 2018 on Anti-Money Laundering and Countering the Financing of Terrorism and its related regulations.

Authorities such as the Central Bank of the UAE, Securities and Commodities Authority, and the Financial Intelligence Unit oversee compliance and enforce reporting requirements.

Fintech firms must also report suspicious transactions through the goAML system and maintain proper customer due diligence procedures.

________________________________________

Key AML Requirements for Fintech Startups

Fintech startups must adopt several core AML controls to meet regulatory expectations.

1. Digital Know Your Customer (KYC)

Startups must verify customer identities using digital onboarding tools, biometric verification, and document authentication technologies.

2. Customer Risk Assessment

Companies should classify customers based on risk factors such as geography, transaction behavior, and business activity.

3. Transaction Monitoring

Automated monitoring systems must track transactions in real time to detect suspicious patterns or unusual activity.

4. Sanctions Screening

Fintech companies must screen customers against international sanctions lists issued by organizations such as the United Nations and other global authorities.

5. Suspicious Activity Reporting

Any suspicious transaction must be reported to the UAE Financial Intelligence Unit within the required timeframe.

________________________________________

Emerging AML Trends for Fintech

Over the next decade, AML compliance for fintech startups is expected to evolve significantly.

1. Artificial Intelligence in AML

AI-based monitoring systems will help detect suspicious transactions faster and reduce false positives.

2. Blockchain Monitoring Tools

Regulators are encouraging fintech firms dealing with crypto assets to use blockchain analytics tools to track transaction origins.

3. Real-Time Compliance Monitoring

Advanced compliance platforms will enable instant risk analysis and transaction screening.

4. Regulatory Sandboxes

The UAE continues to support fintech innovation through regulatory sandboxes that allow startups to test products while meeting compliance requirements.

5. Global Collaboration

Fintech companies operating internationally must align with global AML standards recommended by the Financial Action Task Force.

________________________________________

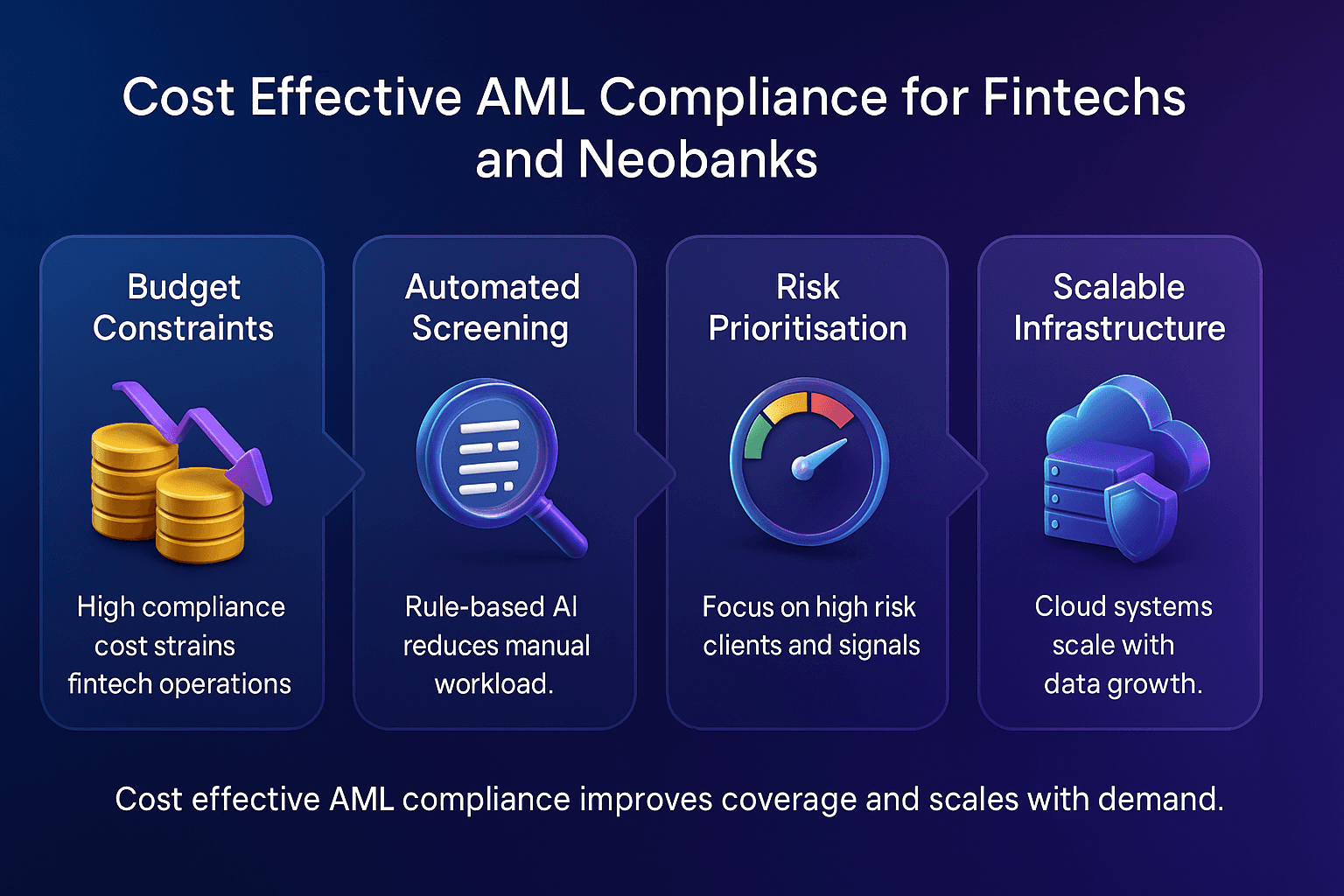

Challenges Fintech Startups May Face

While fintech innovation offers significant opportunities, startups may encounter several AML compliance challenges:

• High cost of compliance systems

• Lack of experienced compliance professionals

• Rapidly changing regulatory requirements

• Managing cross-border regulatory obligations

Startups must integrate compliance into their core operations rather than treating it as an afterthought.

________________________________________

How Fintech Startups Can Prepare

To stay compliant in the coming years, fintech startups should adopt a proactive AML strategy:

• Develop a comprehensive AML policy

• Implement automated compliance technology

• Conduct regular risk assessments

• Train staff on AML obligations

• Maintain proper reporting and record-keeping procedures

Early investment in compliance infrastructure will help fintech startups build trust with regulators and customers.

________________________________________

Conclusion

Fintech startups are reshaping the financial services industry, but this innovation must be accompanied by strong AML controls. As regulators continue to strengthen compliance expectations, fintech companies must integrate AML frameworks, advanced technology, and risk-based monitoring into their operations.

By adopting proactive compliance strategies, fintech startups in the UAE can continue to innovate while maintaining transparency and protecting the integrity of the financial system.

________________________________________

About Sheikh Anwar Accounting & Auditing LLC

Sheikh Anwar Accounting & Auditing LLC is a UAE-based professional firm providing AML compliance advisory, risk assessment services, corporate tax consultancy, VAT services, and audit & assurance solutions. The firm assists fintech companies, financial institutions, and DNFBPs in implementing effective AML frameworks aligned with UAE regulatory requirements.

Website: www.sa-auditors.com

Email: info@sa-auditors.com

Phone: +971 52 916 4130

Address: Dubai Creek Tower, M35, Dubai, UAE