AML for DNFBPs in Ras Al Khaimah

Introduction

Ras Al Khaimah (RAK) has evolved into a major hub for business and trade within the UAE, attracting companies across real estate, corporate services, jewellery, and accounting sectors. Many of these businesses fall under the category of Designated Non-Financial Businesses and Professions (DNFBPs) — entities that play a crucial role in maintaining the integrity of the UAE’s financial system.

While the emirate’s open economy, free zones, and investor-friendly policies encourage growth, they also present money laundering (ML) and terrorist financing (TF) risks. It explores the key AML risks DNFBPs face in RAK, the regulatory framework, and best practices to ensure compliance.

________________________________________

1. Understanding DNFBPs in Ras Al Khaimah

In the UAE, DNFBPs include:

• Real estate brokers and agents.

• Dealers in precious metals and stones (PMDS).

• Auditors and accountants.

• Lawyers, notaries, and other legal professionals.

• Corporate service providers (CSPs) and trust formation agents.

Under Federal Decree-Law No. (20) of 2018 and Cabinet Decision No. (10) of 2019, DNFBPs must comply with national AML and CFT (Countering the Financing of Terrorism) regulations.

In RAK, entities licensed under RAKEZ (Ras Al Khaimah Economic Zone) are directly bound by the RAKEZ DNFBP Regulations 2020, which require registration, risk assessment, and adherence to AML obligations.

________________________________________

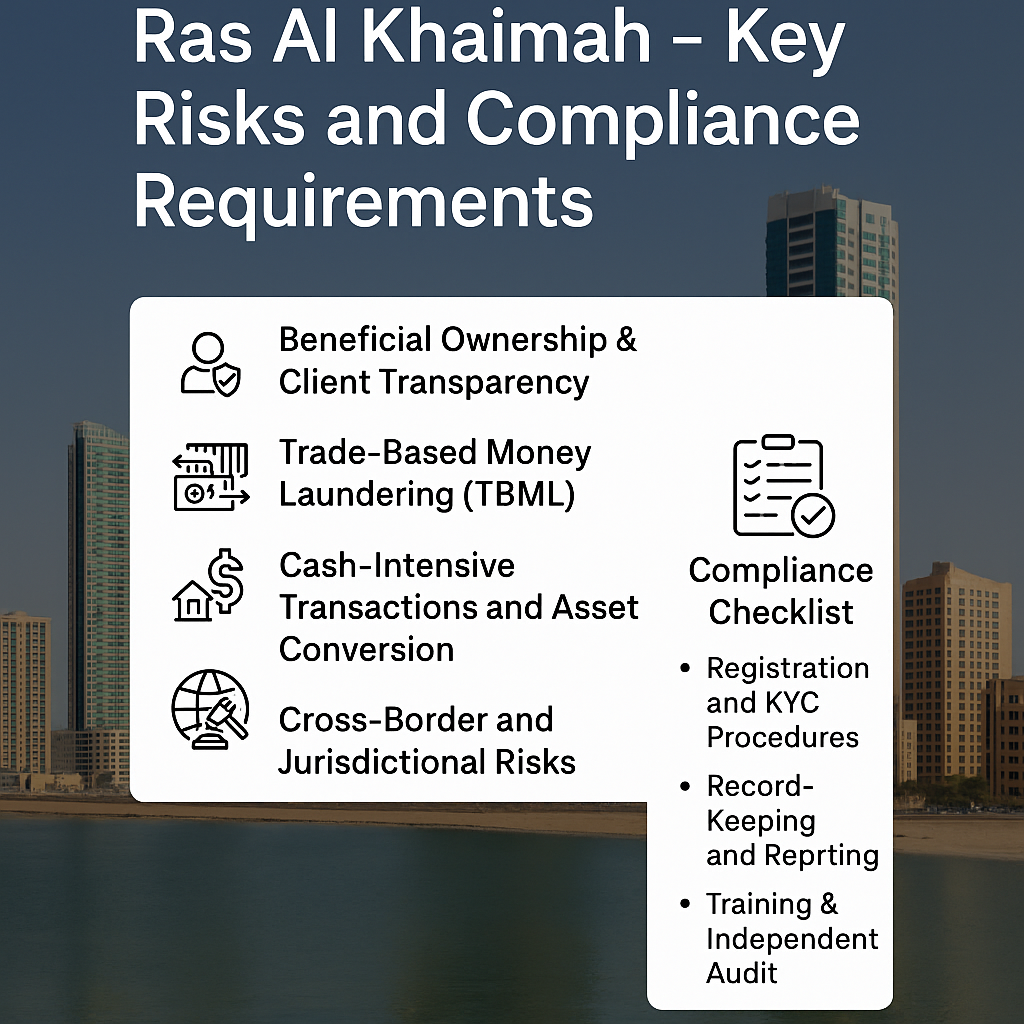

2. AML Risks Faced by DNFBPs in RAK

a. Beneficial Ownership & Client Transparency

RAK’s global appeal allows foreign investors to establish companies quickly — sometimes with opaque ownership structures. Shell or front companies may be used to obscure true ownership.

Mitigation:

• Verify the Ultimate Beneficial Owner (UBO) of every client.

• Conduct sanctions and PEP screening before engagement.

• Maintain ongoing monitoring to detect ownership changes.

________________________________________

b. Trade-Based Money Laundering (TBML)

RAK’s logistics and trading ecosystem can be exploited for trade-based laundering, involving false invoicing, mis-declaration of goods, or circular trade chains through multiple free zones.

Mitigation:

• Match invoice values to global market prices.

• Check trade routes for commercial logic.

• Train staff to identify TBML red flags, including unusual shipment patterns or third-party payments.

________________________________________

c. Cash-Intensive Transactions and Asset Conversion

DNFBPs dealing in gold, diamonds, and real estate often handle high-value transactions that can disguise illicit funds as legitimate business proceeds.

Mitigation:

• Restrict cash payments above AED 55,000 unless source of funds is verified.

• Accept only traceable payment methods (bank transfers).

• For real estate and jewellery, verify documentation on origin, ownership, and value of assets.

________________________________________

d. Cross-Border and Jurisdictional Risks

Clients from high-risk or non-cooperative jurisdictions increase AML exposure due to limited transparency or weak regulatory controls.

Mitigation:

• Maintain a jurisdictional risk matrix aligned with FATF’s grey and black lists.

• Apply Enhanced Due Diligence (EDD) for clients linked to such countries.

• Avoid engagements involving countries subject to UN or OFAC sanctions.

________________________________________

e. Record-Keeping and Reporting Gaps

One of the most common compliance failures among DNFBPs is poor record management or failure to report suspicious activities.

Mitigation:

• Retain all AML-related documentation for at least five years.

• Appoint a Money Laundering Reporting Officer (MLRO).

• Register on the goAML portal to file Suspicious Transaction Reports (STRs) and Suspicious Activity Reports (SARs) promptly.

________________________________________

3. AML Compliance Obligations for DNFBPs in RAK

Requirement Description

Registration All DNFBPs must register with the Ministry of Economy (MoE) and the goAML portal.

Risk Assessment Conduct an Enterprise-Wide Risk Assessment (EWRA) to identify ML/TF vulnerabilities.

CDD / KYC Procedures Implement robust Customer Due Diligence (CDD) to identify and verify clients, ownership, and purpose of transactions.

Reporting Report any suspicious activity through the goAML system immediately.

Record Retention Maintain KYC, transaction, and risk assessment records for five years.

Training & Awareness Conduct annual AML training for all relevant staff.

Independent Audit Periodically test and review AML controls for effectiveness.

________________________________________

4. Best Practices for DNFBPs in Ras Al Khaimah

✅ Develop a Written AML Policy:

Define internal procedures for KYC, reporting, and record retention.

✅ Implement Technology Tools:

Use AML screening software for sanctions, PEP, and adverse media checks.

✅ Regular AML Training:

Train employees to recognize suspicious behavior and emerging typologies (e.g., misuse of virtual assets).

✅ Maintain a Culture of Compliance:

Ensure leadership commitment — “Tone at the Top” is key to regulatory trust.

✅ Engage Compliance Professionals:

Work with AML consultants or auditors to align your practices with UAE and RAKEZ standards.

________________________________________

Conclusion

Ras Al Khaimah’s dynamic economic environment offers DNFBPs immense growth opportunities. However, compliance is not optional — it is essential for sustainability, reputation, and access to the banking system.

By adopting a risk-based AML approach, DNFBPs can safeguard their operations, meet regulatory expectations, and contribute to the UAE’s position as a trusted and transparent business hub.

________________________________________

For Expert AML Compliance Support

Sheikh Anwar Accounting and Auditing LLC

Licensed Auditors & AML Compliance Advisors – Ministry of Economy (Entry No. 5817)

📍 Dubai Creek Tower, Office M-35, UAE

📧 info@sa-auditors.com | 🌐 www.sa-auditors.com

📞 +971-58-562-1786